The US economy is moving fast, with volatile markets reflecting rapid changes and unexpected turnarounds. The Great Pandemic Reflation (2020-21), a stimulus-induced recovery that brought the US economy back to life from the depths of a sharp downturn, went down in history as one of the most dramatic macroeconomic events on record. After the US GDP sunk with the pandemic in Q2 2020, it rebounded strongly with growth rates that took the economy to a level above the pre-pandemic trend over the last two years. During this period, US markets enjoyed extraordinary rallies with equity indices staging strong performance and cyclical commodities paring losses to make new highs in relatively short order.

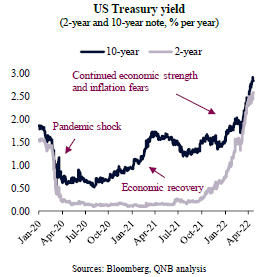

Importantly, macro-sensitive US Treasuries confirmed the positive backdrop. In fact, after recession fears and the Covid-19 shock led 10-year US Treasury yields to decline precipitously for more than a year, the economic recovery started to push yields up significantly between August 2020 and April 2021. After consolidating for a few months between May and December 2021, yields surged again on the back of moderating fears from Covid-19 variants in the West, renewed inflation fears and a more “hawkish” US Federal Reserve (Fed).

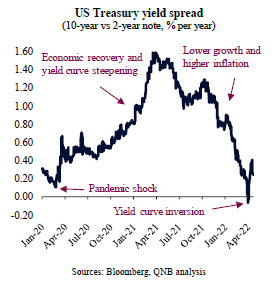

However, the US Treasury yield curve, or the spread between short- and long-term yields, tell us a more nuanced macro story. From August 2020 to April 2021, bond yields indeed pointed to continuous tailwinds for the US economy. The benchmark spread between 10-year and 2-year Treasuries widened, producing a healthy steepening of the yield curve. This was a positive sign for the economic expansion as lower yields at the short-end of the curve implied monetary stimulus and higher yields at the longer-end of the curve implied stronger growth or inflation expectations. Moreover, the price ratio between high-yield corporate bonds and US Treasury bonds increased, suggesting elevated risk appetite from bond investors or a “risk-on” environment.

But bond markets started to act differently after April 2021, with the yield curve flattening and risk appetite diminishing. This process accelerated after the Fed Open Market Committee (FOMC) meetings in June and December 2021, when a more “hawkish” Fed and the guidance for the start of a more rapid process of “policy normalization” surprised the market.

In our view, bond markets are sending three messages about the US economy.

First, bonds are suggesting that US growth has already peaked in Q2 2021, after several quarters of hyper-strong activity. In other words, bond markets are pointing to a significant slowdown of the US economic recovery, with growth rates set to return to a more normal ballpark of around 2% per year.

Second, the bond market is considering that current inflationary pressures may continue over the medium-term, but are going to ease over the long-term, however accompanied by lower growth. A flattening yield curve (short rates moving up faster than long rates) suggests that inflation is only a medium-term worry. Indeed, 10-year bond implied inflation expectations (breakeven inflation rate) have gone up only moderately by 60 basis points (bps), to stay relatively contained at around 3%, significantly below the current consumer price inflation of 8.5% for March 2022.

Third, US Treasury bonds are serving as a “safe-haven” in times of geopolitical turbulence in Europe and Asia as well as a lower-risk instrument to bet on a more robust economy. With every interest rate hike in the US, interest rate differentials globally widen, making US Treasury bonds a safer investment from a risk-reward perspective. This creates higher demand for US Treasuries, limiting more upside movements in US Treasury yields. Savers in European countries and Japan, where activity has been more sluggish and interest rates lower, are increasing their allocation to US Treasuries as US yields increase further. This creates a cap for long-term yields.

All in all, US bond yields have had a strong run in recent quarters. However, the yield curve and its respective spreads started to flatten in April 2021, signalling a weaker economic outlook, long-term inflation expectations that are lower than current inflation and US outperformance versus other advanced economies.

Download the PDF version of this weekly commentary in English or عربي