The International Monetary Fund (IMF) has recently published its October 2021 World Economic Outlook (WEO), “Recovery during a pandemic”, highlighting key elements of the ongoing global economic rebound. According to the IMF, growth is expected to remain strong globally, increasing by 5.9% in 2021 and decelerating modestly to expand by 4.9% in 2022.

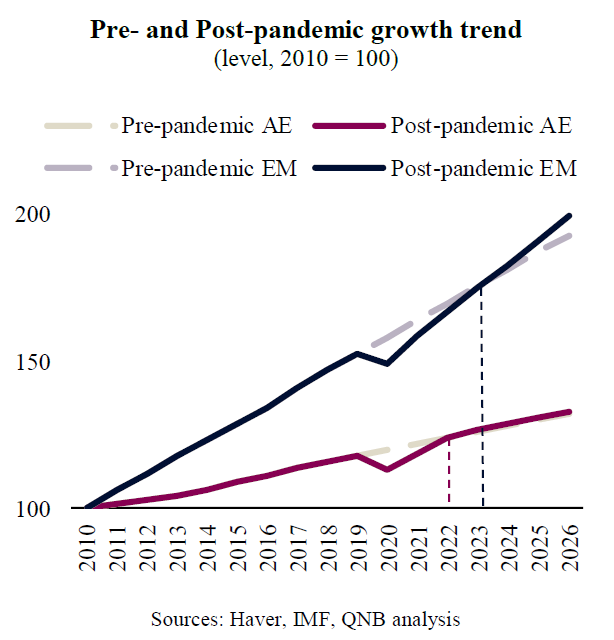

While the IMF’s overall outlook remained broadly similar to their previous forecasts, there were significant changes below the surface, across different countries and regions. In fact, the main takeaway from the IMF is that recoveries are expected to diverge significantly going forward. Emerging markets (EM) are expected to gain less traction than advanced economies (AE) on the recovery process. AE’s are going to reach their pre-pandemic growth trend in 2022, while EM countries are expected to lag behind their previous trends for years.

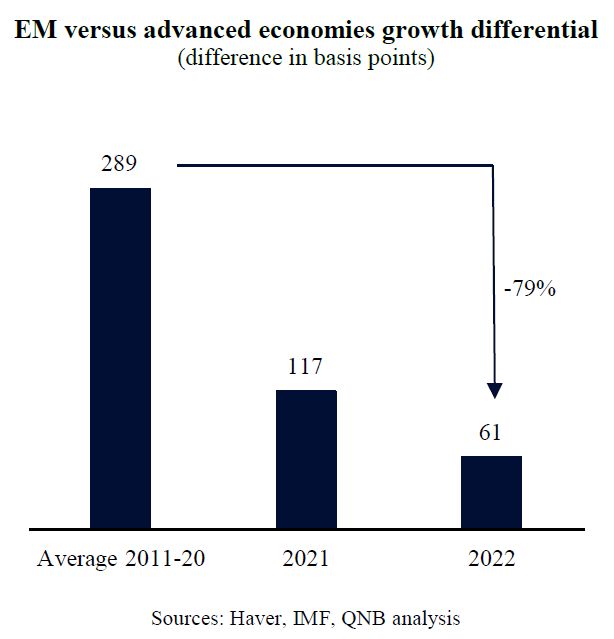

This divergence is also expressed in the weakening of EM relative economic outperformance. EM growth tended to be 289 basis points (bps) stronger than AE growth over the past decade, reinforcing the idea that EM countries were “catching up” to the higher levels of income and economic sophistication of the AE. However, this pattern changed significantly since the post-pandemic recovery and today is more than 3% below its pre-pandemice performance. In our view, three factors explain this change in relative performance.

First, the current change in EM-AE relative economic performance from historical norms is associated with different monetary and fiscal policy space. EM countries, and particularly middle- and lower-income EM, have less policy space to stimulate their economies during a downturn. With weaker central banks and fiscal institutions, and with a smaller capital base to tap into, most EM do not have the conditions to support their households and corporates the same way that more advanced countries do. As a result, while economic authorities protected the balance sheet of the private sector from the pandemic crisis in AE, the same did not apply for most middle- and lower-income EM. Exceptions to this lack of policy space include higher income EM or other EM economies that benefit from a strong net foreign asset positions and low levels of indebtedness. Thus, in EM with limited policy space, both consumption and investment will be relatively slower to recover.

Second, different vaccination rates between EM and AE are also playing a part on the pace of the recovery. Vaccinations programmes have progressed remarkably in AE since the beginning of the year, while vaccinate rollout is much slower in EM. Nearly 60% of the population have been fully vaccinated in AE, compared with only 36% in EM and 4% in low-income EM. As long as this vaccination rate differences persist, EM will be more vulnerable to potential Covid-19 resurgences, which could further delay their recoveries.

Third, the slowdown in China is a particularly strong headwind to EM. China’s economy comprises 43.3% of total EM GDP. Moreover, Chinese growth has a high multiplying effect, often spilling over globally, particularly to commodity exporters and Asian EM. Thus, the current slowdown of growth in China, from over 18% year-on-year (y/y) at its peak to around 4.9% in the last quarter, is materially negative for the growth outlook of EM.

All in all, while the global economy is expected to continue its recovery from the pandemic, divergences are significant and should continue over the next couple of years. Middle- and lower-income EM are expected to lag behind their pre-pandemic growth trends and “catch up” to AE at a slower pace than previously anticipated.

Download the PDF version of this weekly commentary in English or عربي