The fallout of the Covid-19 pandemic has already produced the largest global wave of economic policy support ever recorded. As governments across different continents responded to the health crisis with tight social distancing measures and lockdowns, a sharp decline in economic activity was trigerred in Q2 2020. In order to prevent a sudden collapse of private income or a more persistent impairment on the balance sheet of corporates and households, economic authorities around the globe were quick to use all tools at their disposal to offer relief.

Major central banks cut policy rates aggressively or supported the financial system with massive injections of liquidity, preventing a disorderly dislocation of credit and equity markets. More importantly, fiscal expansion became paramount. Fiscal policy tools are more appropriate to provide the relief that corporates and households need, including through programs such as paid sick leave, extensions of unemployment benefits, tax holidays, direct transfers to families, and subsidized loans to small and medium enterprises.

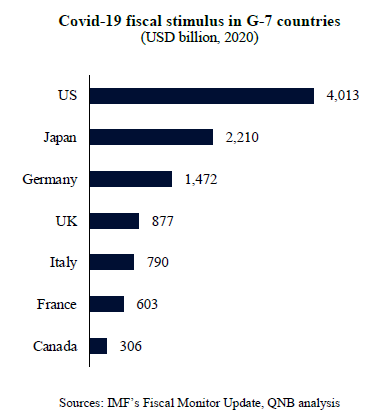

And there was no shortage of fiscal policy action to respond to the economic consequences of the pandemic. According to the IMF, extraordinary fiscal stimulus measures amounted to USD 14 trillion globally in 2020, or more than 15% of global GDP. Half of these measures consisted of additional spending or foregone revenue with the other half including “below the line measures” such as loans, guarantees and equity injections. Importantly, more than 70% of the total fiscal support was deployed by the major advanced economies of the G-7 (Canada, France, Germany, Italy, Japan, the UK, and the US).

But what comes next for fiscal policies in the G-7? Three main factors underpin our assessment of G-7 fiscal policies moving forward.

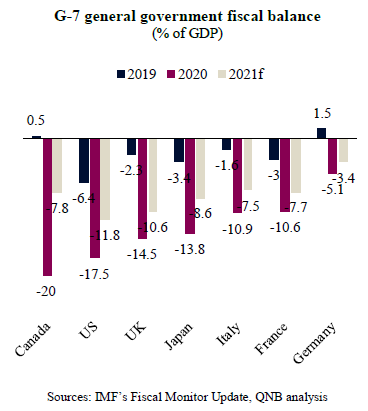

First, fiscal deficits will moderate across all G-7 countries in 2021. Recovering economic activity will naturally increase goverement revenues, for example by increasing the amount of Value Added Tax paid by the services sector as people go out for leisure and entertainment activites rather than staying at home. Likewise, government expenditure will naturally decrease, for example, as service sector emplooyees are able to return to work and stop claiming unemployment benefits. While last year almost all G-7 countries presented double digit fiscal deficits as a percentage of GDP, only the US is set to continue running such deep deficits in 2021. This in part reflects the concerns of sovereigns with elevated debt levels, exchange rate risks, and potential rating downgrades or other adverse market reactions if mega deficits persist.

Second, despite the distribution of Covid-19 vaccines, the economic recovery and lower deficits than last year, the fiscal policy of G-7 countries is still set to continue being far from “normal” this year. Fiscal deficits in 2021 are likely to still be a multiple of the pre-pandemic deficits as G-7 countries introduce new measures to cushion against a larger shock from sudden support withdrawal and to provide additional relief for vulnerable groups. Examples include the planned USD 1.9 trillion stimulus package from the new US administration and the USD 70-100 billion stimulus committed by Canada for the next three years.

Third, new fiscal initiatives are likely to be less focused on immediate emergency relief and more focused on what has been called “build back better.” The idea is that new G-7 allocations are going to be hybrid, focusing both on supporting the economy and on enabling a greener, more digital and inclusive transformation of the economy. This includes infrastructure programs as well as enhanced training and job search programs for the unemployed or for workers from industries that are going to be phased out.

All in all, a “normalization” of fiscal policies within the G-7 is already taking place. But the process will be rather slow and gradual, as governments want to take the opportunity to advance new investment programs while avoiding “withdrawal issues” of a premature exit from extraordinary measures.

Download the PDF version of this weekly commentary in English or عربي