The fallout from the global spread of Covid-19 produced tremendous stress in energy markets. Early during the pandemic, in the first half of 2020, a negative demand shock from large-scale global lockdowns amplified the effects of a supply glut associated with a “market share war” amongst oil exporters to send the energy industry into a tailspin. This led to a historic rout that rapidly pushed crude oil prices to multi-decade lows.

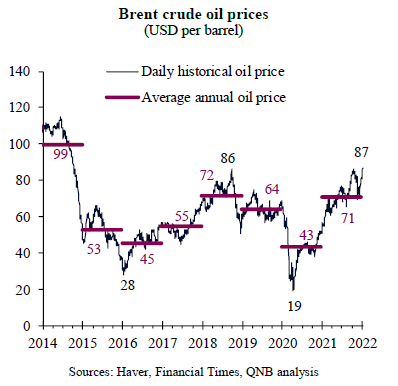

In fact, the crisis was so severe that it caused a temporary collapse in market structure, with inland-linked crude price benchmarks such as West Texas Intermediate (WTI) plunging to deep negative prices, as storage hubs got overwhelmed and transportation costs surged. Brent crude, the most relevant benchmark for global trade, bottomed at around USD 19 per barrel in late April 2020.

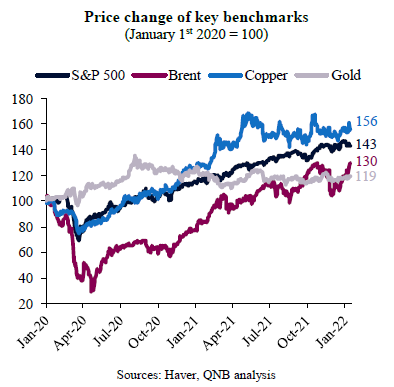

However, the doom and gloom did not last for too long. After bottoming in April 2020, crude oil prices staged a remarkable turnaround. Brent crude prices rallied ever since, up 358% within 20 months from the bottom. Importantly, Brent is already 30% above pre-pandemic price levels, even if still lagging and underperforming other key benchmarks, such as cooper or the S&P 500. But the catch up of Brent prices to these other benchmarks has gained momentum in recent months.

The rally was driven by a much faster than expected demand recovery, ignited by policy stimulus and strong demand for goods, and strict supply management measures by OPEC+ member countries, led by Saudi Arabia and Russia.

Moving forward, while Bloomberg consensus forecasts suggest a moderation of Brent prices to average USD 74 per barrel in 2022, we hold a different position. In our view, Brent prices are expected to remain well supported, ranging around USD 85 per barrel. This is supported by two main factors.

First, global growth remains strong and the cyclical upswing is expected to continue for longer, on the back of inventories for manufactured goods at critically low levels and a new wave of capital expenditure in infrastructure projects. In addition, as the world adapts to Covid-19, more people return to work from the office and vaccines as well as antivirals become more available, transportation demand will pick-up further, particularly for air travel and tourism. We expect strong pent-up global demand associated with further open-ups and tourism in H2 2022.

Second, despite the ongoing, planned release of production quotas from OPEC+, global supply growth has been slow, even as crude oil trades at more attractive prices. In Russia, the lack of drilling investments last summer made it difficult for the country to ramp up output at a faster rate. Moreover, outside OPEC+, shale producers in the US are responding slowly to the new scenario due to the imposition of more capital discipline by investors and the deterioration of midstream and service infrastructure capacity after the historic slump in 2020. Analysts estimate that the reaction function of shale production to higher prices halved since the pandemic shock, making the shale patch less relevant in quickly adjusting to market imbalances. Hence, supply growth is limited over the medium-term.

It is important to note, however, that the outlook for oil prices is particularly vulnerable to shocks at this stage. Downside risks could materialize with negative demand shocks, including a potential worsening of the pandemic, a further slowdown of China or a policy mistake from the US Federal Reserve tightening “too much, too fast.” This would push oil prices significantly below current levels. On the other hand, upside risks could materialize if global growth accelerates further with the opening-up of Asia or if geopolitical events disrupt supply, such as a conflict in Ukraine. As physical oil markets are under-supplied and inventories of advanced economies are at the lowest levels in more than 20 years, this would cause Brent prices to spike in quick order.

All in all, conditions are ripe for crude oil prices to remain strong over the medium-term, even if the bulk of the recovery in terms of price gains are likely already behind us.

Download the PDF version of this weekly commentary in English or عربي