Every summer, the US Federal Reserve (Fed) organizes a coveted economic policy symposium in Jackson Hole, Wyoming. The event is one of the longest-standing central banking conferences in the world, bringing together top economists, bankers, market participants, academics and policy makers to discuss long-term macro issues.

During the Jackson Hole Symposium last year, which was also held virtually due to Covid-19 concerns, the Fed formally announced its new monetary policy framework, in which inflation is targeted to average 2% over time. Under such framework, the 2% target should be achieved over the business cycle, implying that past inflation deviations from this target have to be partially or fully compensated in the future or “averaged.”

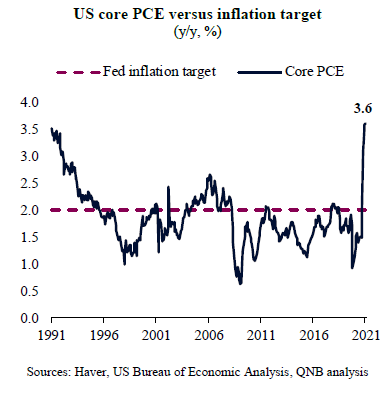

While this Fed-led symposium always looms large in the agenda of investors, this year the importance of the event was paramount. It followed a period of extraordinary policy support against the Covid-19 shock, a record-breaking economic recovery and a significant overshoot in US inflation. In fact, the US core personal consumption expenditures price index (PCE), the Fed’s favourite gauge for inflation, spiked by 3.6% year-on-year (y/y) in July 2021, the highest rate in 30 years.

Continued supply disruptions associated with the pandemic and a strong recovery of demand are keeping several prices under pressure. This, along with a fast improvement of employment numbers, is creating the macro backdrop to the introduction of “normalization” measures by the Fed. Such normalization would entail scaling down asset purchases (tapering) from the current USD 120 Bn per month and, later, interest rate hikes.

During his speech at Jackson Hole, Fed Chairman Jerome Powell delivered what the market interpreted as a relatively “bearish” view about the US economy. In his remarks, Powell emphasized downside risks such as “too high unemployment,” a “likely temporary” uptick in inflation and concerns over the Delta-variant that would justify a rather slower pace of monetary normalization. He also eliminated ongoing speculations about earlier than planned interest rate hikes in the near future, before 2023. This suggested that extraordinary monetary stimulus is set to be scaled down at a slower pace than previously expected by the market.

In our view, three factors support Chairman Powell’s cautious approach to monetary policy normalization.

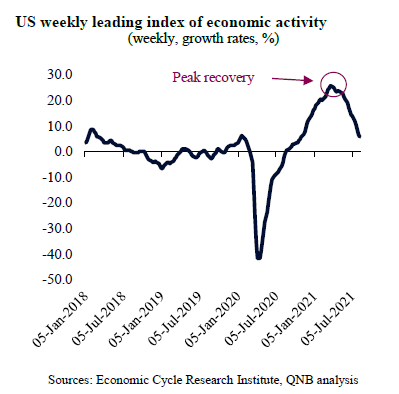

First, the US recovery is losing momentum as fiscal stimulus fades and consumption growth moderates, after months of extraordinary expansion. According to the US weekly leading index of economic activity, which is a composite of high-frequency data that tends to lead the business cycle by 3 to 10 months, the US economy is set to slow down significantly over the next several months. The main reason for this is the contraction of personal income, as direct transfers from the government ended in April 2021 and special unemployment benefits are set to end over the next few weeks. Monetary authorities will be wary to withdraw stimulus too fast just when the US economy is slowing and household income is contracting.

Second, inflation is expected to moderate over the next few quarters as Covid-19 related supply disruptions ease and the supply of labour normalizes. There are already signs that severe shortage of chips and other key inputs or finished goods are softening, and the remaining bottlenecks should gradually normalize over the next 9 months. Moreover, US labour shortages will likely wane after special unemployment benefits are withdrawn and the school schedule returns to a more normal “in-person regime,” favouring females return to work. A higher rate of labour participation is expected to prevent any price-wage spiral, lowering the odds for more sustained acceleration in inflation and reducing the need for policy intervention.

Third, the spread of Delta and other highly contagious Covid-19 variants still pose risks to the global recovery, particularly in countries with low vaccination rates or high vaccine hesitancy. A sudden spike of virus risks in the US over the winter can quickly disrupt the economy, eliminating the likelihood of too abrupt of a change in monetary policy.

All in all, the path to monetary policy normalization will be rather long, with authorities leaning on the side of caution. The ongoing economic slowdown after the recovery, a moderation of inflation and existing downside risks all substantiate the Fed’s caution on scaling down stimulus too much or too early.

Download the PDF version of this weekly commentary in English or عربي