Being the earliest economy hit with the novel coronavirus (COVID-19), the Chinese economy is now in the vanguard of the economic recovery. Indeed, China is one of the few countries expected to see economic growth during 2020 as a whole. Activity data continued to improve in May, likely taking the level of output above that of 2019, for the first time since the pandemic erupted. However, growth rates are still below of that in 2019. We expect a positive growth rate of 1.5% in 2020.

Our analysis focuses on two key aspects of the Chinese economy to better understand the depth of this nascent recovery. For simplicity, we will refer to year-on-year growth rates throughout the article.

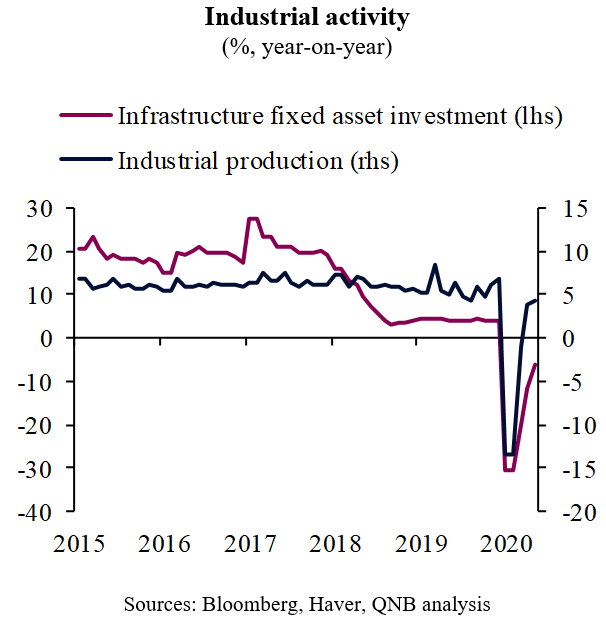

First, the Chinese authorities have returned to their tried and tested methods of economic stimulus via government spending on infrastructure investment. The People’s bank of China has lowered the official rate twice from 4.15% to 3.85% this year. Record high issuance of nearly RMB 1 trillion of special local government debt has boosted infrastructure fixed asset investment, which jumped to 11.6% in May, up from 4.6% in April. This has in-turn pushed up growth in fixed asset investment, up 3.9% in May from 0.6% in April. Similarly, industrial production growth improved to 4.4% in May from 3.9% in April. Indeed, particularly strong contributions from increases in steel and cement highlight how such infrastructure spending can directly boost industrial output. Broadly, the Caixin manufacturing PMI rose 1% in May, the first positive growth rate since the outbreak shock of COVID-19, up from -1.6% in April.

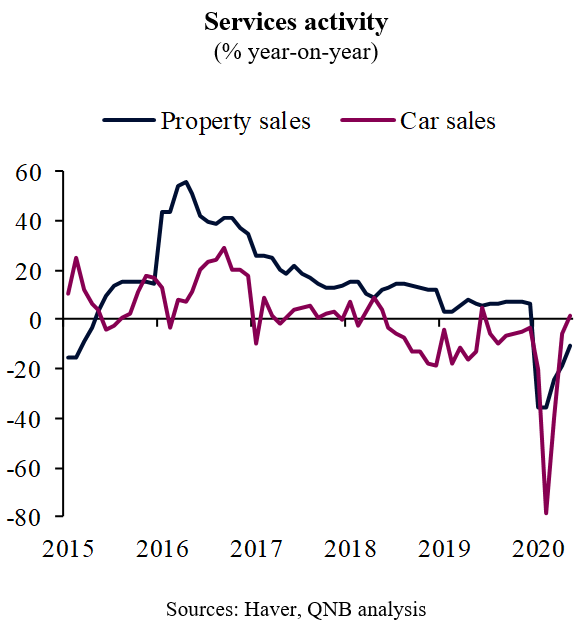

Second, the services sector is showing some of the most encouraging signs. Property sales rebounded strongly, although growth in new property remains more subdued and suggest that developers remain cautious. Car sales have also rebounded strongly. Pent up demand is likely to have contributed to the rebound in sales. However, the strength of the rebound suggests that consumers are becoming more willing and able to make large purchases once again. More generally, services activity expanded 1% in May, a considerable improvement from the 4.5% contraction in April. Moreover, the Caixin services business activity PMI rose 4.4% in May, a significant rebound from -18.6% in April.

There are some reasons to remain cautious. Export growth turned negative in May, which suggest that external demand remains a drag. In addition, a surge in cases due to an outbreak of COVID-19 in Beijing has sparked fears of a second wave in China. However, neither issue is unexpected. Countries all over the world are easing lockdown measures as they continue to learn how to better control and manage the virus without resorting to extensive lockdowns again.

We had not been expecting to see such widespread positive year-on-year growth until Q3, but an increasing number of indicators suggests that China’s economy has already regained its pre-virus level, if not growth rate.

From the Great Financial Crisis of 2008-09 to last year, China has contributed to 42% of the total global economic expansion in nominal terms. Moreover, China’s investment focused growth model has driven strong demand for commodities. Therefore, China’s early return to growth is a boon for the entire global economy and both emerging markets and commodity exporters in particular.

Download the PDF version of this weekly commentary in English or عربي