Despite the emergence of the new Omicron variant of concern, it is worth noting that the global economy has made a remarkable recovery from the peak impact of the Covid-19 pandemic last year. The main driver has been unprecedented fiscal and monetary stimulus, particularly in the United States (US), which unleashed a tsunami of consumer demand. Unfortunately, neither “Factory Asia” or global supply chains have been able to cope with such strong demand. The result has been severe bottlenecks in supply chains, which are pushing up the costs of goods and delaying their delivery.

The bottlenecks in global supply chains are one of the hottest topics of discussion in global economics at the moment. They are acting as a headwind to the economic recovery resulting in unmet demand that may never be satisfied. They are also driving high global inflation presenting central banks with challenges in policy decisions.

Despite bottlenecks being persistent, we have confidence that global supply chains are already recovering. Three key observations support our view: unsustainably strong demand is beginning to ease, “Factory Asia” is recovering from being hit by the Delta variant in Q3; and global shipping times and costs are already beginning to fall.

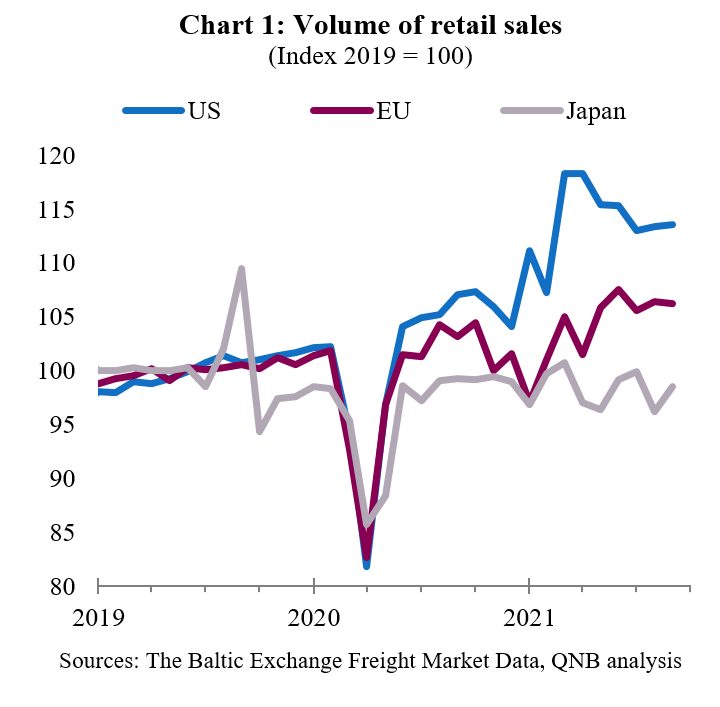

First, massive fiscal and monetary stimulus has allowed demand for consumer goods to recover in most advanced economies. In particular, stimulus in the US has been so strong that it has caused an unsustainable surge in demand felt globally. However, budget constrains apply even to the US government and fiscal policy is beginning to tighten naturally. President Biden’s Build Back Better (BBB) act sounds large with a headline figure of USD 2 trillion in new spending and tax benefits. However, the impact of BBB will spread out over 10 years and the focus on infrastructure spending will feed into consumer demand much more gently than stimulus cheques sent directly to households. In contrast, there was a recovery in consumer demand in other large economies (e.g., the EU or Japan), but demand did not reach similar levels as in the US (Chart 1). The net result is that global consumer demand will remain robust, but is already easing from an unsustainable surge driven by the US.

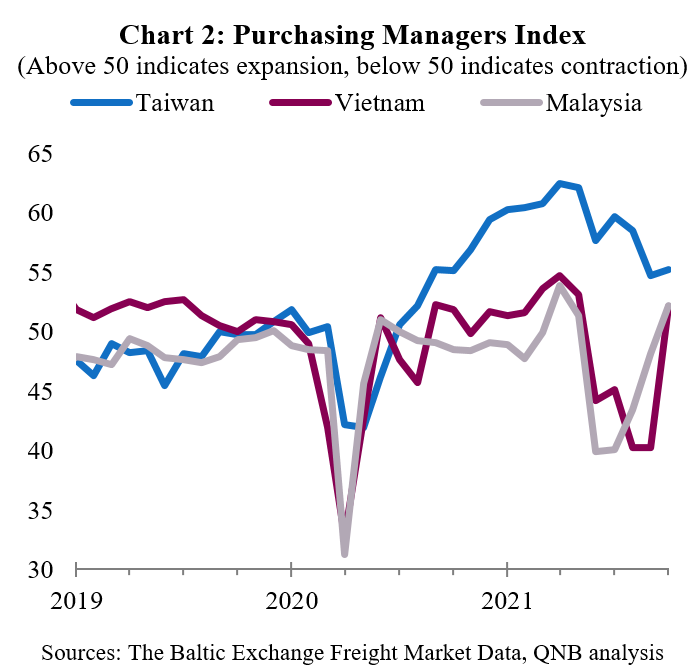

Second, the surge in consumer demand came at a time when “Factory Asia” was hit by a wave of the pandemic caused by the Delta variant. Although, Asian countries successfully managed the impact of the pandemic in 2020, they became complacent and were slow to get started with vaccination campaigns since the beginning of 2021. This meant that the Delta variant caused a surge in new infections and restrictions were required to control it, which unfortunately also lowered manufacturing output. Fortunately, rising vaccination rates over the last few months have helped Asian countries to regain control in managing the impact of the pandemic. Now, production within “Factory Asia” is recovering and they are rapidly working through the backlog of orders (Chart 2).

Third, global shipping costs are beginning to fall and are an indicator that supply chain bottlenecks are easing. A number of high frequency indicators of global shipping costs have fallen recently. The “Baltic dry index” has fallen 50% from a peak of over 5000 in October, its highest level since 2008, to less than 2,500 on the 17th November. The “Freightos Baltic index” for containers has fallen from its record high of over 11,000 in September to around 9,000 in late November. Another, “Drewry’s composite World Container index”, decreased by around 10% from its peak in October to around USD 9,000 by the 18th November. Lower global shipping costs, whilst still high, help ease pressure on global supply chains.

Although bottlenecks in global supply chains are still severe, we have confidence that the situation will continue to improve over the coming year. We expect this to reduce the pressure currently being felt by global central banks, enabling them to keep interest rates lower for longer. Further, the boost to supply, combined with more monetary policy space to maintain demand stimulus for longer, is expected to support the global economic outlook next year at a time when fiscal policy and base effects are fading.

Download the PDF version of this weekly commentary in English or عربي