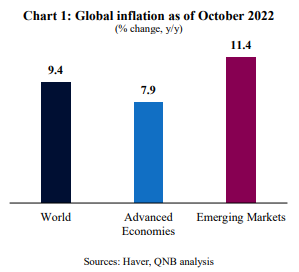

Elevated inflation has been a dominant topic throughout this year. Across countries, inflation has been driven by both demand and supply factors, often amplified by exogenous shocks or non-economic factors. On the demand side, it is mostly a product of excess consumption created by ultra-loose monetary and fiscal policies in advanced economies. On the supply side, it is negatively affected by supply-chain constraints, tight labour markets and the persistent lack of investment in extracting fossil fuels. Supply-side constraints have been recently magnified by the war in Ukraine, which caused a surge in energy and commodity prices in early 2022.

High or chronic inflation is oftentimes a phenomenon experienced by emerging markets (EM). This is also true in times where inflation is a concern across the globe. This article sheds further light on the different drivers of EM inflation.

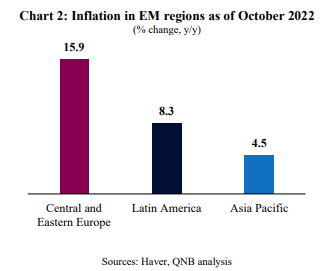

The high level of inflation in Central and Eastern Europe (CEE) this year is primarily due to their more direct exposure to higher energy prices caused by the War in Ukraine. Although energy prices have risen globally, it is more difficult for countries in CEE to substitute their energy away from gas, which has been cheaply supplied to them by Russia for most of the past decade. Going forward, we would expect high inflation in CEE to ease back, as base-effects cause energy price spikes to fall out of year-on-year comparisons.

Inflation in Latin America (LATAM) is more moderate due to several factors. First of all, the region did not experience the same monetary policy support with excessive liquidity injection throughout the pandemic. Secondly, several LATAM central banks prevented an upcoming inflationary cycle and frontloaded interest rate hikes last year, when inflation was still nascent. This was in contrast to most major central banks, which were late to recognize the significance of the post-pandemic inflationary shock. Moreover, large components of global inflation are associated with commodities, particularly food and energy prices. As LATAM is itself a net commodity exporting region, it has benefited from higher revenues and incomes. More aggressive central banks and positive commodity revenues supported some LATAM currencies, preventing the spike in imported prices that EM countries experienced elsewhere. The outlook for inflation in LATAM is for a moderate easing of inflation, again mainly due to base effects, but also in the context of reduced political uncertainty with the conclusion of the presidential election in Brazil.

Inflation in Asia Pacific is the lowest for two main reasons. First, is the disinflationary impulse from the persistent weakness of activity in China. And second, the relative strength of Asian currencies, which typically benefit from relatively strong external positions and substantial reserve buffers. An additional factor that has helped keep inflation low in Asia is the fact that commodity exports have allowed Malaysia and Indonesia to reduce inflation via subsidies. Looking forward and assuming Chinese growth accelerates, as we expect, then we would expect Asian economies to experience stronger inflationary pressures. As a result, Asian central banks may need to follow the Fed’s rate hikes more aggressively going forward.

All in all, inflation in Asia Pacific has been much lower than in Europe or Latin America. But we expect this divergence in inflation pressures across EM regions to moderate next year.

Download the PDF version of this weekly commentary in English or عربي