In recent decades, Southeast Asia has stood out as one of the most dynamic regions in the world, showcasing numerous countries with exceptional growth trajectories. This group of countries includes Indonesia, the fourth most populous country globally with 286 million people, only smaller than three well-estabablished engines of global economic growth: China, India, and the U.S. During 2000-2024, the Indonesian economy expanded at an average growth rate of 5%. This is a remarkable performance, sustained during a challenging period that included the highly volatile years of the Global Financial Crisis and the Covid-pandemic. Furthermore, this was achieved with notable stability, with only three years of growth below 4%.

President Prabowo Subianto, whose five-year term began in October 2024, seeks to boost economic growth to 8%, a level not seen in Indonesia in almost three decades. But the country is now facing a set of challenges that will test its ability to reach such bold ambitions. Rising geopolitical tensions and escalating tariff wars among major economies threaten to disrupt global trade and capital flows, creating uncertainty for Indonesia’s export-driven sectors. In addition, falling commodity prices and still-tight financial conditions in advanced economies pose a risk to investment in emerging economies, and could continue to add volatility to their currencies, including the Indonesiah rupiah.

In this article, we discuss key factors that will determine Indonesia’s economic growth outlook for this year.

First, consumption will remain a highly-supportive growth engine of economic activity. Consumption represents 55% of the Indonesian economy and is therefore a major factor behind its growth performance. The strength in consumption is sustained by a resilient labor market, which has shown a remarkable recovery since the Covid-pandemic. The unemployment rate has fallen from a peak of 7.1% in 2020, to 4.9% according to the latest print of 2024, the lowest since 1998.

To further boost consumption, President Prabowo’s administration is putting forward a series of policy measures, including a larger-than-expected minimum wage increase of 6.5%, and has scaled back a value-added tax hike that was planned for this year. Additional stimulus measures include electricity rebates, income tax cuts for factory workers, and the massive flagship free-meal program for children that aims to cover 83 million recipients, and could soon reach USD 28 Bn in annual spending. Resilient labor markets, together with stimulative government policies will provide ample support to consumption this year.

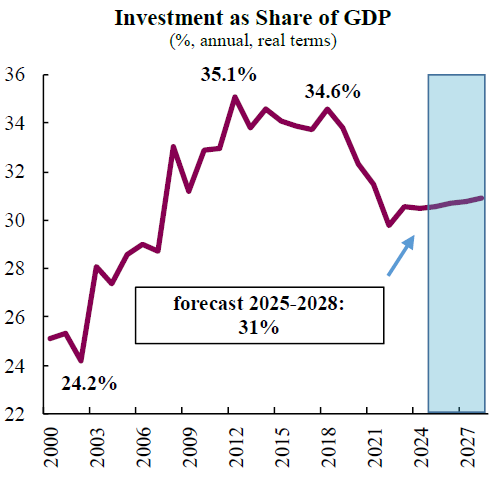

Second, Indonesia has a robust pipeline of major infrastructure and capital expenditure projects that will bolster economic growth. The collection of infrastructure initiatives, which amounts to hundreds of billions of USD, is one of the priorities of the new administration. Major projects are expected in sectors such as transportation (roads, bridges, railways, airports, ports), logistics, mining, and facilities needed for new manufacturing plants. A key driver for additional infrastructure spending is the plan to move the capital city from Jakarta to the island of Borneo, which represents investments of USD 33 Bn.

Lending measures will also be leveraged to stimulate investment, in a context where credit is already expanding at a pace close to 10% per year. Bank Indonesia will increase liquidity incentives to IDR 80 Tn (close to USD 5 Bn) for banks lending to the housing sector, as part of a program to build 3 million houses per year. Housing is a key sector to support economic growth and job creation given its supply-chain linkages. The growth prospects of the country are also attracting foreign investments, and FDI is expected to reach 1.5% of GDP in 2025. Public investments and FDI flows will add to keep a healthy level of investment, which will remain above 30% of GDP and contribute to a robust pace of economic growth.

Third, exports will continue to provide additional backing to the economic expansion, as the country remains largely insulated from the direct impact of escalating tariff wars. Exports grew 6.5% year-over-year in 2024, contributing to 1.5 percentage points of real GDP growth, and are expected to maintain a strong performance this year. Indonesia is a criticial supplier of metals, such as nickel and copper, needed to drive the world’s energy transition from fossil fuels, and stands to benefit from the rising demand of these products.

In a context of increasing geopolitical tensions and escalating tariffs, especially between the US and China, Indonesia could potentially benefit from easier market access for its goods that typically compete with Chinese products in the US, such as textiles and garments, and electronics and electrical equipment. In the medium term, trade disputes between the US and China would encourage business relocation and investment in other countries in Southeast Asia, including Indonesia, giving an additional boost to its economy.

All in all, we expect the Indonesian economy to expand at a slightly above-consensus 5.3% this year, on the back of strong consumption, a robust pipeline of infrastructure and Capex projects, and a favourable trade outlook.

Download the PDF version of this weekly commentary in

English

or

عربي