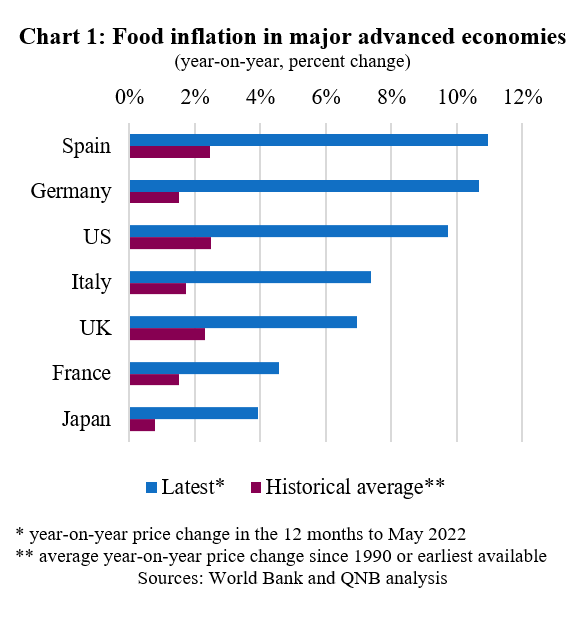

The world is dealing with severe stagflation, with decade-high inflation and slowing economic growth in most major advanced economies. Surging food prices are a significant contributor to high headline inflation in many countries, including most major advanced economies (Chart 1).

Spain and Germany are currently seeing food price inflation of over 10% compared to just under 4% in Japan. Most of the difference between countries is caused by consumption of different types of food, e.g., rice has a large weight in the Japanese food basket, but the price has actually fallen in the past year. Despite the differences between countries, it is clear that food price inflation across countries is much higher in the past year than the historical average since 1990. Therefore, in this article we focus on the four main drivers of the current high food prices across countries: high oil and gas prices, weather effects, labour shortages and wage growth, and more recently the war in Ukraine.

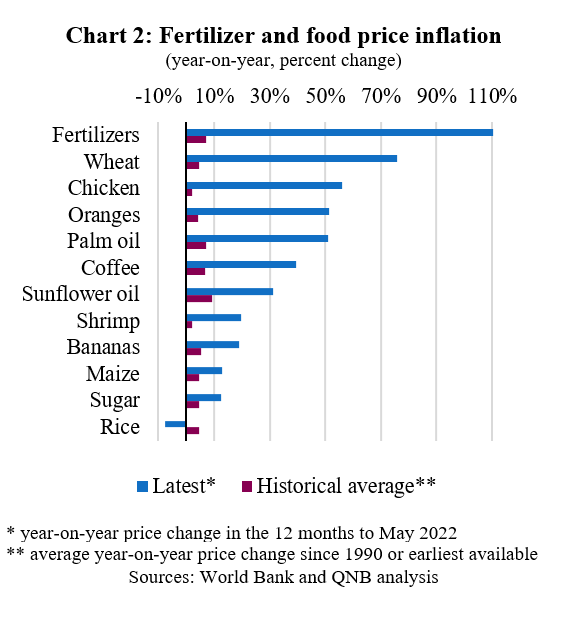

First, oil and gas prices feed into high food prices in a number of ways. Fertilizer production is energy intensive, so fertilizer prices have risen substantially (Chart 2). Growing foods requires fertilizers to replace nutrients used from the soil, so fertilizer prices feed directly into food prices. Fuel and energy also contribute to food price inflation via the cost of processing and transporting food. If oil and gas prices remain high, as we expect, they will continue to put upward pressure on food prices.

Second, adverse weather, including droughts in US and Brazil, have reduced yields and pushed up prices for wheat and soybeans. Similarly, heavy rain in China and unusually hot weather in India also hit wheat yields and prices. Weather is hard to predict, but climate change is widely acknowledged to be causing more frequent and more extreme adverse weather. This will continue to put upward pressure on food prices on average.

Third, migrant labour flows have not yet returned to pre-virus levels. The agricultural sector in particular is heavily dependent on migrant labour which contributes to labour shortages in many advanced economies.. This in turn is pushing up on costs via both higher wages and lower productivity. Nevertheless, we expect migrant flows to recover as the pandemic continues to abate and consequently expect the upward pressure from labour shortages to ease.

Finally, the war in Ukraine has worsened the outlook for some of the above factors, particularly for higher oil and gas prices. Furthermore, Russia and Ukraine account for 28% of the world’s wheat exports and 55% of the world’s sunflower oil exports. The war has caused extensive crop destruction in Ukraine, but is also disrupting or completely preventing exports via Black sea ports. Even with an immediate cease-fire, the existing disruption will heavily impact this year’s harvest and still have a negative impact for next year. Therefore, the war is leading to substantial and persistent upward pressure on food prices.

Taken together, we expect the war in Ukraine and high oil and gas prices to keep food prices high, despite an easing of pressure from labour shortages, whilst the impact from adverse weather remains uncertain.

Persistently high food inflation will continue to erode households’ spending power, reducing discretionary spending, and contributing to the stagnation of global GDP. At the same time, persistently high food inflation will reduce and delay the fall in headline inflation.

Central banks normally “look through” changes in food and energy prices as they are notoriously volatile and tend to be driven by supply side factors. Consequently, central banks have no control over them. However, central banks no longer have the luxury to do so given how large the impact of food prices is currently on inflation. Therefore, central banks are tightening policy in response to “headline” inflation (including both food and energy), rather than their usual focus on “core” inflation.

Download the PDF version of this weekly commentary in English or عربي