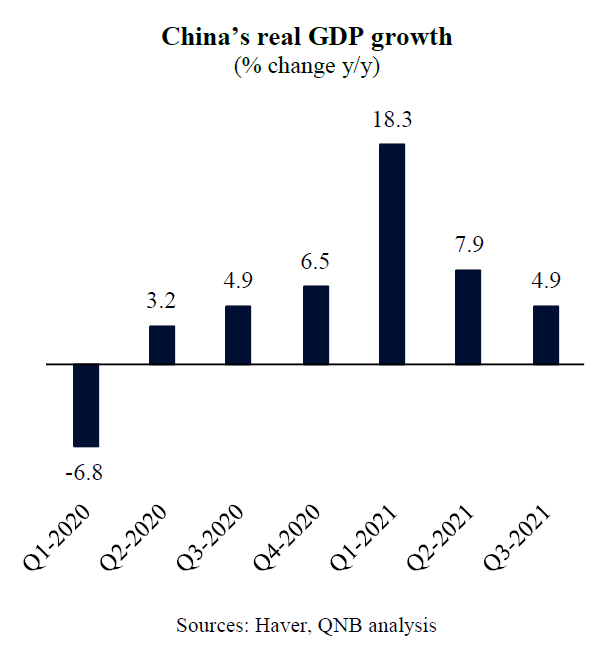

Since the outbreak of the global pandemic and its consequent downturn last year, China has been on a recovery path for more than six quarters. In Q1 2021, China’s growth peaked with overall record growth of 18.3% in real terms, predominately driven by infrastructure investments and the export sector. Over the last two quarters, however, growth of the Chinese economy could not keep up with the record speed previously seen and since then started to flatten and even decelerate. Given the sheer size of the economy, a moderation of growth of the Chinese economy is likely to spill over into the global economy and impact other adjacent countries that are economically connected or integrated to China.

This analysis delves into the three reasons why growth in China is moderating and may further slowdown over the remainder of the year.

First, the withdrawal of policy stimulus by Chinese authorities in late 2020 and early 2021 is starting to affect domestic demand, which in turn accelerates the cooling of the economy. Policy tightening was paramount, including fiscal and regulatory measures. On the fiscal front, extraordinary benefits expired and public investments moderated. On the regulatory front, authorities imposed restrictions for credit growth to the real estate sector and created new rules for different technological industries, which slowed down investments. This has contributed to moderate the growth of the economy, given that household consumption remained relatively weak and could not offset the decline in government spending and investments.

Second, the de-leveraging of major property developers in China is spilling over to the broader domestic real estate market, dampening sentiment in one of the leading economic sectors of the country. The real estate sector, when measured in broader terms, including supply chain effects and fiscal revenues, accounts for around 25% of total GDP. The potential default of major property developers is expected to further weaken economic activity in the sector. Moreover, debt distress of property developers could affect the domestic credit market, which would create additional challenges for investment growth. Both factors are significantly impacting growth.

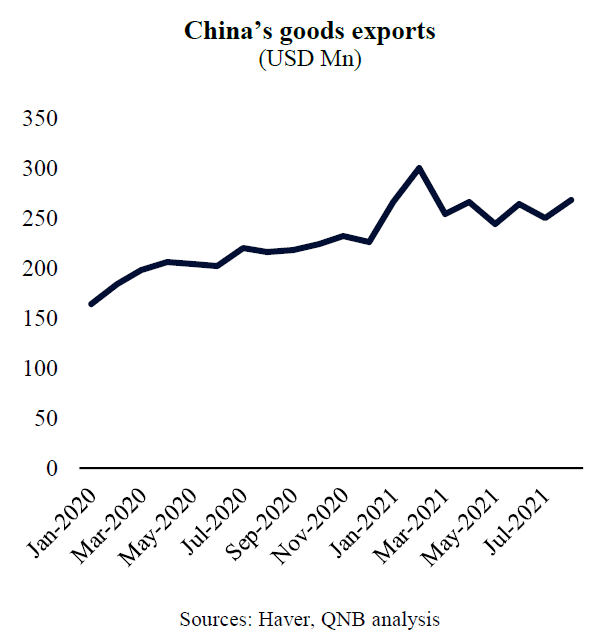

Third, export growth, a key driver for the Chinese economic recovery so far, is now threatened by the deterioration of supply side constraints in the energy sector. Higher coal prices and shortages of other key commodities are leading to power outages in several provinces. In order to ensure energy supply to households, authorities are imposing power rationing to energy-intensive manufacturers. This situation could further aggravate during the winter, when energy demand typically surges. While the government is trying to address the situation with several measures, including loosening regulation on energy producers and coal miners, it is still unclear whether manufacturers will benefit from stable power supply in Q4 2021. Should the energy situation worsen, export growth will be further affected.

All in all, the real estate and export sectors were the main driving forces of the Chinese economy since the Covid-19 shock. However, policy tightening and real estate headwinds are already contributing to a significant slowdown. Moreover, energy supply constraints are starting to also negatively affect the export sector. Hence, we expect to see growth in China to decelerate further in Q4 2021, before re-gaining momentum next year, as the impact of policy tightening fades and supply constraints ease.

Download the PDF version of this weekly commentary in English or عربي