The novel coronavirus (Covid-19) outbreak spread rapidly around the world. Governments have responded with containment and mitigation policies, including testing, isolation of infected patients and comprehensive social distancing measures. However, the spread of the outbreak affected the behaviour of both households and corporates, causing a deep downturn. This analysis delves into the recent experiences of selected economies of East and Southeast Asia (EM Asia), including China, South Korea, Indonesia, Thailand, Malaysia, Singapore, Philippines and Vietnam.

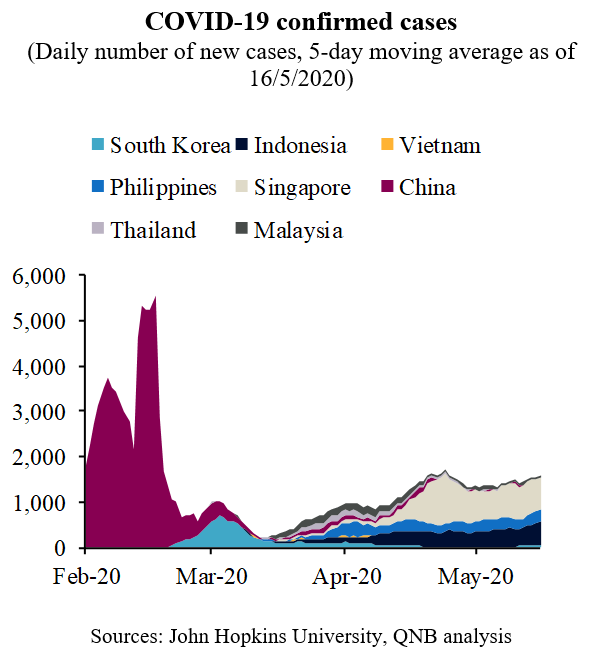

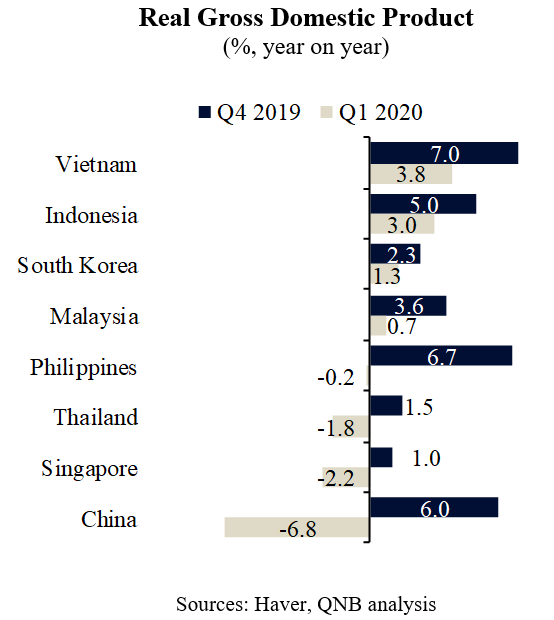

Gross domestic product (GDP) data for Q1 2020 in EM Asia came out weak, ranging from 3.8% to -6.8% year-on-year (y/y) from 1% to 7% y/y in the previous quarter. The difference in performance is explained by both the magnitude of the epidemic spread and the timing of the virus expansion. Infections in China, South Korea, Thailand, Malaysia, Singapore (initial wave) and Vietnam happened relatively early, whereas significant outbreaks took only place weeks later in Indonesia and the Philippines. Moreover, South Korea and Vietnam were able to identify root causes of virus spread early on and therefore experienced less drastic containment policies (massive testing, isolation of infected patients and only regionally targeted comprehensive social distancing). The magnitude of the initial spread required China and Thailand to launch more comprehensive and broad mitigation policies, including large-scale, strict social distancing measures.

There is still uncertainty about the impact of Covid-19 on GDP in Q2, but the “opening up” of the EM Asian economies will provide insights of the speed of recovery. This is particularly obvious in countries that are comfortably on the other side of the peak with regards to new infections (China, South Korea, Vietnam, Thailand and Malaysia), potentially setting up for a quick rebound. But optimism should be measured. Moving away from more strict forms of social distancing bears the risk of a “second wave” of infections which would require the return of strong mitigation policies. The case of Singapore provides an important cautionary tale. After a success in initially controlling the epidemic and in providing the required health infrastructure, the country faced a significant second wave of cases after a period of normalization.

All in all, we believe that four reasons explain why the economic recovery of EM Asia will be rather gradual and slow over the second half of the year.

First, several restrictions towards public gatherings, work, social distancing, traffic and other activities are expected to remain partially in place. Therefore, a full return to pre-Covid-19 normality seems unlikely. This will naturally limit output capacity, placing a cap on the recovery over the next few months.

Second, irrespectively of government mandated measures, individuals and private institutions are likely to become more risk averse when it comes to both financial and health issues. As a result, their marginal propensity to save rather than to spend or invest should increase, dampening consumption and investment.

Third, policy support to boost growth will take time to permeate through the economy. This is valid for the monetary policy accommodation as well as for the more expansive fiscal stance. While local central banks have lowered rates by a minimum of 50 to up to 125 basis points and fiscal authorities launched spending packages ranging from 2% to 17% of their respective GDP, it will most likely take several months for the stimulus to generate a significant pick up in consumption and investment.

Fourth, not all countries have a robust healthcare infrastructure in place to ramp up capacity and put together the necessary capabilities for containing potential new waves of virus spread. Crucial parts of the progress made by countries such as China, Korea, Vietnam and initially Singapore were related to testing and tracing capabilities. Without a robust containment strategy, countries would not be able to maintain a flat curve of new cases for long.

In brief, existing challenges will likely place a cap on the ongoing economic recovery of EM Asia. Expected rebounds are set to be rather gradual and will, vary markedly from country to country. The recovery should accelerate only after Covid-19 is fully contained and official support is in full swing.

Download the PDF version of this weekly commentary in English or عربي