European bond markets have been particularly volatile in recent weeks as the general sell-off that started later last year deepened. The stagflationary shock triggered by the Russo-Ukrainian conflict was a major driver of the deterioration, adding to supply chain constraints associated with the pandemic. According to Bloomberg’s consensus forecasts, growth expectations for the Euro area in 2022 plummeted to 2.7%, from 4.4% as of September 2021. At the same time, Euro area inflation accelerated from 3.5% to 8.6%. This represents an unprecedented worsening of the macro outlook.

As a result, and despite the slowdown in growth expectations, the European Central Bank (ECB) has been under pressure to tighten policy and deliver on its 2% inflation mandate. In fact, in its latest policy meeting, the ECB decided to lean “hawkish,” tightening rates by 50 basis points (bps) instead of the expected 25 bps. It is the first policy rate hike of the ECB in more than a decade. Importantly, the action placed the ECB’s deposit rate out of negative territory for the first time in 7 years.

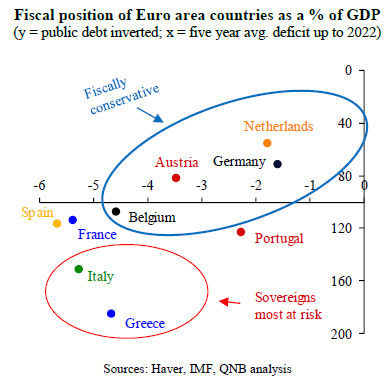

However, monetary tightening in the Euro area could be challenging. The macro situation differs across countries within the monetary union, particularly when it comes to fiscal needs and debt levels.

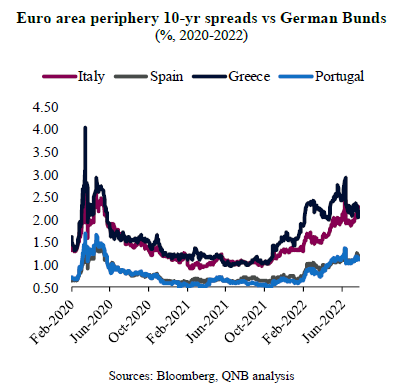

Mediterranean countries of the South or the “periphery” of the Euro area, such as Greece, Italy and Spain, run wider fiscal deficits and accumulate higher levels of indebtedness than the more fiscally conservative economies of the North (Germany, Austria, Belgium and the Netherlands). Hence, Southern European economies are more vulnerable to a more aggressive tightening pivot from the ECB, as higher interest rates increase the debt burden, potentially creating unsustainable sovereign credit dynamics. In fact, as further rate hikes were priced into the markets, yields started to soar across the board.

German 10-year Bunds jumped by more than 130 basis points (bps) since late last year. More importantly, during the same period, spreads between German Bunds and bonds from Southern European countries widened significantly, running close to the stressed levels last seen during the depths of the pandemic crisis. Italy and Greece present the most difficult position, with their spreads widening by 130 and 100 bps, respectively. According to different debt sustainability metrics, the current yields for Italy and Greece may well be enough to start another round of Euro debt crisis discussions.

More stressed sovereign debt markets in the Euro “periphery” have already required action from the ECB. In mid-June, the ECB’s Governing Council called for an emergency meeting to discuss so-called “anti-fragmentation” measures, i.e., policy actions designed to support countries under stress and protect the integrity of the monetary union. Then, ECB officials announced both, more flexibility in the allocation of funds when re-investing redemptions from its asset purchase programme and the creation of a new anti-fragmentation instrument for the region. In practice, these measures meant that maturing assets from the ECB can be re-invested disproportionally in bonds from stressed sovereigns and that more funds should be made available to provide a backstop for the “periphery.” The result of these discussions materialized in the recent policy meeting, when the ECB announced the so-called “Transmission Protection Instrument” (TPI) to counter “unwarranted, disorderly market dynamics.”

For some analysts, such new measures are just expressions of how difficult the monetary policy normalization will be in the Euro area. In our view, the emergency meeting mandated the groundwork for the creation of the necessary tools for a “de-coupling” of the ECB’s actions. This means that the overall policy normalization to combat inflation and create price stability is most likely to be rolled out across the Euro area via more aggressive interest rate hikes. On the other hand, to prevent an aggravation of the stress to the countries of the “periphery,” the ECB reserves itself the discretion to use and re-allocate quantitative tools to support more fragile Euro area economies. In this sense, it was no surprise that the ECB decided to enact on a more aggressive pace of tightening.

All in all, we expect to see a more active ECB in the second half of the year. A potential solution for the Euro area’s “macro divergence problem” opens the door for more aggressive policy rate hikes while at the same time preventing more severe shocks and a potential sovereign Euro area crisis. We expect to see the ECB’s Governing Council hiking rates by 50 bps in the following meetings in September and October, before slowing to a more normal pace of 25 bps rate hikes in December. This may be just the beginning of a historical normalization process.

Download the PDF version of this weekly commentary in English or عربي