China remains a major source of uncertainty for the global growth outlook this year. In fact, the country is behind a significant part of the global slowdown story over the last several quarters. Late last year, the Chinese economy was expected to grow by 5.6% in 2022. At the time of writing, however, Bloomberg consensus forecasts pointed to an expected expansion of only 3.5% for the same period.

Importantly, Chinese growth stood even still last quarter. This was the worst economic performance of China in more than 30-years, excluding Q1 2020, when the country rapidly reacted to the initial wave of the Covid-19 pandemic. The weak print came on the back of a gradual but protracted slowdown that started about a year ago, after the strong initial recovery from the pandemic.

In our view, the slowdown of China was caused by four main factors. First, the early withdrawal of both fiscal and monetary stimulus, which did not help to support aggregate demand when households were still cautious about the medium-term economic consequences of the global pandemic. Second, the combination of new waves of Covid-19 variants with China’s Zero-Covid policies led to “stop-and-go” patterns in activity that punished any momentum in either consumption or investment growth. Third, the energy crisis in the second half of last year affected negatively industrial production in certain provinces of China, due to power rationing and production shutdowns. Fourth, the comprehensive campaign to tighten regulation on the real estate and corporate sectors, which dampened business sentiment and contained a more significant rebound in private investments.

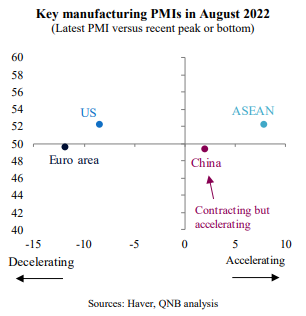

However, despite the negative momentum, there are early signs that the Chinese economy may be about to turn a corner into a recovery mode. The manufacturing Purchasing Managers’ Index (PMI) of China, a survey-based indicator that measures whether several components of activity improved or deteriorated versus the previous month, seemingly bottomed in April this year. Traditionally, an index reading of 50 serves as a threshold to separate contractionary (below 50) from expansionary (above 50) changes in business conditions. While higher frequency data are still indicating that China’s economy is contracting or running below normal levels, it started to accelerate again in recent months, due to a moderation of Covid woes and the re-opening of some important cities. This places China on a similar path of Southeast Asian (ASEAN) economies, which struggled last year due to the pandemic but are now on a recovery phase. In contrast to the economies in Asia, activity is slowing down and even contracting in other major advanced economies.

Chinese policymakers are becoming more concerned about the economic slowdown and are starting to ease more aggressively. In recent weeks, the People’s Bank of China (PBoC) trimmed interest rates again for several segments, indicating a deepening of its “dovish stance.” In addition, it is ramping up liquidity injections via open market operations.

We expect the “pandemic risk” to also moderate significantly in China, particularly after Q4. This is due to the development of new, more effective, Chinese mRNA vaccines against new variants of the Covid-19 virus as well as the availability of efficient antiviral pills. Over time, these developments should favour the abandonment of Zero Covid policies, allowing activity to gain momentum in a more sustainable fashion.

After several quarters of a comprehensive regulatory tightening in the key real estate and technology sectors, authorities are now moderating their positions and providing more clear guidance to China’s large corporates. Businesses are quickly adjusting to the new business environment and uncertainty should diminish over time. This will create the conditions for higher investments over the coming quarters.

Finally, energy constraints have also eased significantly. While China is currently experiencing energy problems in its hydro power plants, due to droughts and insufficient inflows into the mega Three Georges Dam, the “coal crisis” from last year has been controlled. Coal availability surged while prices collapsed from very high H2 2021 levels. On balance, the energy situation is much better now for China, as coal accounts for about 60% of energy consumption in the country, versus 17% for hydro power.

All in all, we believe that activity in China is currently bottoming and the the country is on the verge of a cyclical recovery with the economy accelerating beyond 2022. This will likely help to mitigate the negative effects of the slowdown in major advanced economies and positively contribute and support global growth.

Download the PDF version of this weekly commentary in English or عربي