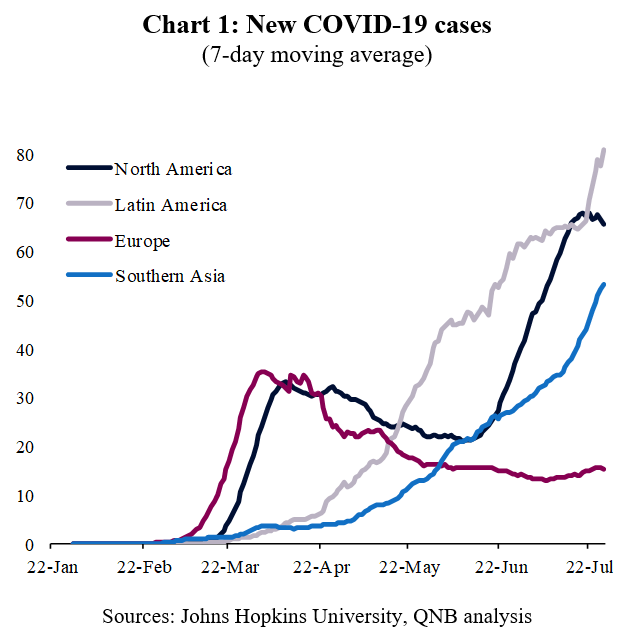

The Euro area is now on track to outperform the US during H2 2020. The virus has been well controlled by local lockdown measures, social distancing and widespread facemask wearing. Therefore, rates of new cases have remained low across Europe despite a continued reopening of the economy (Chart 1). A second wave remains a risk, but our analysis suggests that Europe is well placed to continue its steady reopening without a significant surge in new cases requiring widespread lockdowns.

With this in mind, we highlight four further factors that support the Euro area’s continued recovery.

First, timely activity indicators continue to indicate that the Euro area economy is rebounding rapidly from the sharp slowdown in Q2. Euro area Q2 real GDP is expected to see a record contraction, but this weakness was driven by measures taken to control the virus and is now safely behind us. The Euro area composite flash PMI jumped to 54.8 in July, the strongest reading since early 2018. Of course, the level of activity remains depressed relative to its pre-virus level, but we expect strong growth in Q3. With a return to containment measures in the US likely to hamper consumer spending over the summer, we expect the Euro area to outgrow the US in 2020H2.

Second, EU leaders took a huge step forward by reaching agreement on the Recovery Plan and medium-term budget last week. The final deal is less ambitious, with grants of only EUR 390 billion, lower than the EUR 500bn in the initial proposals. Even so, we consider the agreement a significant step forward for Europe. Goldman Sachs estimates that “Italy and Spain will receive grants of 5% and 6% of GDP, respectively, during 2021-23, plus cheap loans of up to 7% of GDP”. In combination with the European Central Bank’s (ECB) purchases of government debt, the Recovery Plan closes the Euro area’s fiscal funding gap for the next 2-3 years. Further, the Recovery Plan shows a deep commitment to the European project, raising hopes for further fiscal integration.

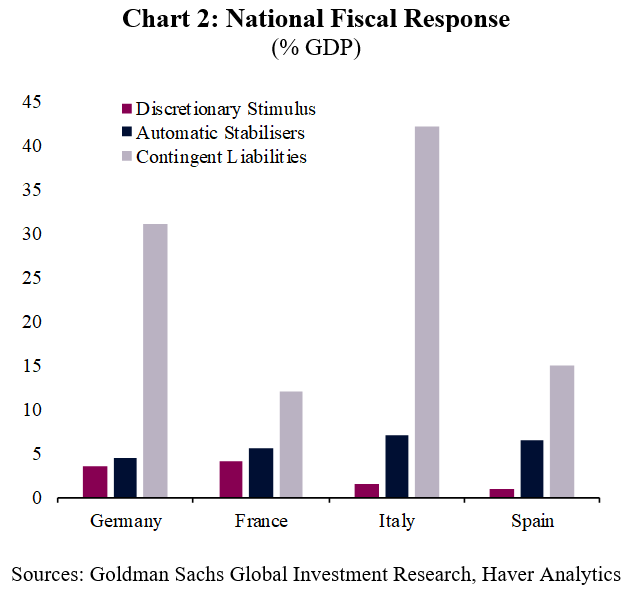

Third, the Recovery Plan will unlock and enable further fiscal measures at the national level (Chart 2). We anticipate that Euro area governments will extend programmes supporting companies and workers to avoid lay-offs, which have been effective at reducing the rise in the unemployment rate. Further discretionary stimulus has already been announced in Germany (around 3.5% of GDP) and France (around 4% of GDP), and we expect more stimulus in Italy (around 1.5% of GDP) and Spain. This will combine with sizeable automatic stabilisers and loan guarantees (contingent liabilities), resulting in significant fiscal support across the Euro area.

Fourth, following decisive action in June, the ECB is providing considerably monetary stimulus, via low interest rates, liquidity injections and Quantitative Easing (QE). Euro area inflation has already slowed, with core HICP inflation down to 0.8% year-on-year in June from 1.2% in February. ECB President Mme Lagarde stressed that, given high uncertainty and subdued price pressures, the ECB intends to make full use of the increased scope of the pandemic QE programme (PEPP). We therefore expect the ECB to extend the PEPP until mid-2021, before refocusing on its more restricted set of prior QE tools.

Effective virus control, improving data and significant support from both fiscal and monetary policy give us confidence in the view that Europe will outperform the US during the second half of 2020. We still expect to see a clear north-south divide within the Euro area, with Germany, France and the Nordic countries recovering significantly more quickly than southern countries that are more exposed to the risk of a second wave, given the dependence of their economies on tourism.

Download the PDF version of this weekly commentary in English or عربي