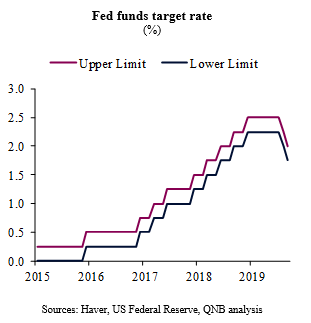

The US Federal Reserve (Fed) has decided to cut rates for the second time in eleven years at its latest monetary policy meeting in September 17-18th. The target range for the benchmark fed funds rate was adjusted down by another 25 basis points (bps) to 1.75-2%. Official reasons for the cut included the “implication of global developments for the economic outlook as well as muted inflation pressures.” This rate cut was widely anticipated.

Fed funds target rate

Out of nine voting members of the Federal Open Market Committee (FOMC), there were three dissents, including two “hawkish” votes against the cut (Esther George and Eric Rosengren) and one “dovish” vote for a deeper cut of 50bps (James Bullard). Dissent in opposite directions are relatively rare in the history of the Fed.

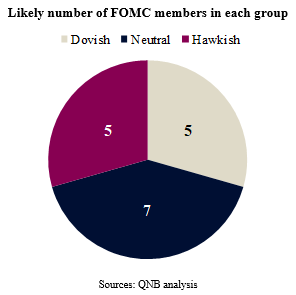

In addition to that, the forward guidance (communication about official expectations of future policy actions) is suggesting a continuation of the current divergence. This is manifested in the “dot plot” or year-end forecasts of interest rates from all FOMC members. Out of 17 FOMC members, including both voting and non-voting members, a significant minority of seven members has projected a third rate cut in 2019. Most importantly, however, five members have decided to effectively show dissent against the most recent rate cut by submitting end-2019 dots of 2-2.25%, 25 bps above the actual rates.

A closer look at recent comments from FOMC members helps us understand the underlying reasons behind the divisions. We have identified at least three main topics of disagreement between “hawks” (supporters of less monetary stimulus) and “doves” (supporters of more monetary stimulus).

First, hawks tend to play down global uncertainty and emphasize the need for the materialization of risks before more supportive monetary policy actions are taken. Doves, on the other hand, believe risks and uncertainty are already amplifying challenging global conditions, suggesting monetary policymakers should try and get “ahead of the curve” or act more preventively.

Second, hawks tend to be more skeptical about the argument that the relationship between unemployment and inflation (Philips curve) is broken, i.e., that low levels of unemployment do not necessarily translates into higher future inflation. Hawks have been often pointing to multi-decade low levels of unemployment and episodic upticks in inflation to defend less supportive monetary policy. Doves argue that secular or long-term structural reasons have weakened the Philips curve considerably and therefore low levels of unemployment are less likely to produce a “inflation scare” or sudden rise in inflation expectations. Moreover, as inflation has undershot the target for several years, doves are more worried about a potential anchoring of long-term inflation expectations significantly below the 2% target.

Third, hawks tend to be more concerned about the potential impacts of excessively accommodative monetary policy on financial stability. Hawks are particularly worried about the bad incentives that low rates for longer can create, including capital misallocation and high indebtedness.

At of the time of writing, we view the FOMC as equally split between hawks and doves, with a higher number of more neutral members who are neither hawks nor doves. Given the lack of consensus about the path of policy rates, we expect the Fed to remain

Download the PDF version of this weekly commentary in English or عربي