We expect a modest acceleration of global GDP growth to around 3.4% in 2020 to be driven by easier monetary policy around the world, in particular the Fed’s dovish pivot to cutting interest rates. That is despite the ongoing US-China trade war, global manufacturing recession and other risks to the outlook.

However, we are concerned that the world has become too dependent on monetary policy, which is becoming less effective. There is also a growing risk that low global interest rates are inflating debt and asset price bubbles. Therefore, it is important that fiscal policy can respond to any substantial negative shocks that hit the global economy.

In this week’s article, we will first assess the current fiscal stance (i.e., whether fiscal policy is a headwind or tailwind for the economy). We will then consider three key constraints on fiscal policy. The need to ensure government debt sustainability and the difficulties arising from both political polarisation and vested interests.

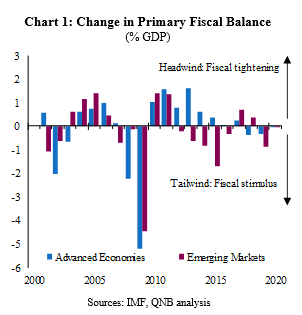

The 2008 global financial crisis was so severe that both monetary policy and fiscal policy were forced to respond with significant stimulus (see Chart 1). Monetary policy has remained very loose, but a period of fiscal austerity, particularly in the Euro area, was required to maintain debt sustainability.

The IMF’s latest estimates indicated that the fiscal stance is providing modest stimulus to the global economy in 2019. Whereas their forecast for global growth to accelerate from 3.0% in 2019 to 3.4% in 2020 is based on an assumption of neutral fiscal policy.

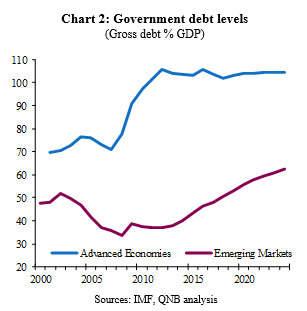

Government debt sustainability is an important prerequisite for a stable economic outlook. Government bonds are one of the least risky and liquid assets in a country. The level and sustainability of government debt depends on three main factors. The strength of nominal GDP growth, the effective interest rate and the fiscal balance.

The IMF expects nominal GDP growth of around 3% in Advanced Economies and 6% in Emerging Markets over the next 5 years. Effective interest rates are falling towards zero in Advanced Economies and falling in many Emerging Markets. Finally, most countries are running manageable fiscal deficits. Put together these factors mean that the IMF projects Government debt in Advanced Economies to be broadly stable at a little above 100% of GDP and a modest increase from a little over 50% to a little over 60% for Emerging Markets (See Chart 2).

In short, government debt is high, but in most cases sustainable as long as interest rates remain low. A number of countries, particularly Germany, China and other Asian Tigers, have considerable fiscal space and would be able to undertake significant fiscal stimulus. Whereas others, such as the US, UK and Japan, have sufficient credibility to undertake growth-enhancing fiscal stimulus whilst their effective interest rates remain close to zero. Therefore, from a technical perspective there is room for significant fiscal stimulus, which leaves us with political constraints.

Globalisation and technological progress have together lifted many people out of poverty across the world. However, there they have contributed to increased inequality in many countries, with rich owners of capital benefitting more than low-skilled workers. This in turn has fuelled increasing political polarisation with populist politicians appealing to voters with more extreme left-wing or right-wing than centralist policies. This makes it more difficult for governments to agree on sensible policies, making government spending and any stimulus less effective and more inefficient.

Another difficulty that governments face when designing good fiscal policy and stimulus comes from vested interests. Specific groups lobby politicians and governments in support of policies that increase their wealth, jobs and/or profits.

We expect global interest rates to remain low for at least the next few years, which will help to maintain government debt sustainability. That will allow fiscal policy to respond to any substantial negative shocks that hit the global economy. However, political polarisation and vested interests will undermine both the efficiency and effectiveness of fiscal stimulus. Taken together these constraints mean that fiscal policy can help mitigate some of the downside risks to global growth, but we caution against viewing fiscal stimulus as a panacea.

Download the PDF version of this weekly commentary in English or عربي