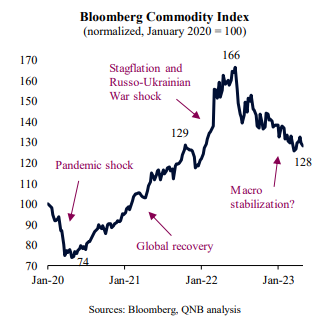

Commodity markets have been particularly volatile since early 2020. The negative demand shock from the Covid-19 pandemic initially triggered deflationary pressures that rapidly pushed commodity prices to multi-decade lows. The Bloomberg Commodity Index, a leading benchmark for general commodity price movements, plummeted from January to late April 2020. However, it did not take long for unprecedented policy stimulus to spur a significant global economic recovery, which supported commodity prices. After a healthy period of economic recovery, excess global demand, combined with supply constraints and the Russo-Ukrainian War shock, led to a spiral of high prices in late 2021 and early 2022. High commodity prices seemed to have reached a zenith mid- last year, before a significant correction that is still under way.

A closer look at commodity price movements can shed light into important aspects of the global economic outlook. The price development of selected commodities conveys relevant macroeconomic information, including trends on sentiment and inflation, often leading or confirming cyclical turning points. Our analysis focuses on three main messages embedded into the recent correction of commodity prices.

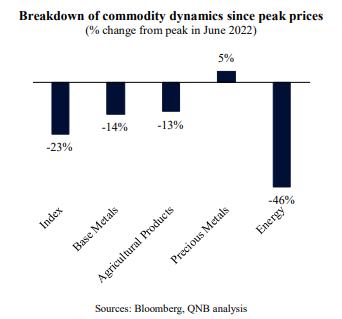

First, commodity prices seem to indicate a further deceleration of the global economy. Higher policy rates, liquidity withdrawals, contained fiscal spending and inflation-driven lower disposable incomes are already moderating aggregate demand, producing a slow down in activity. This is expressed in the more pronounced correction of highly cyclical commodities, such as energy and base metals. Brent crude oil prices, while still slightly above pre-pandemic marks, are down 38% from their recent peak. Copper and lumber prices, important proxies for activity in China and the US, have also collapsed from their recent peaks. Such price performance suggests that the global growth outlook is still dominated by headwinds and the ongoing deceleration in the US and Europe.

Second, the price development of precious metals is pointing to further USD weakness. Gold prices have been recently outperforming long-dated US treasury bonds, suggesting that both foreigners and private domestic investors are favouring non-US issued safe-havens. Higher safe-haven demand for non-US assets, such as gold implies lower potential demand for the USD. In fact, the US Treasury bond-to-gold ratio is an important proxy for USD sentiment, with a declining ratio often signalling a turning point of the USD cycle, from a USD bull market to a USD bear market that favours other currencies. A weaker USD is also a healthy sign of a stronger non-US economic performance, and could be particularly positive for emerging markets, given the incentive for larger positive inflows of foreign capital.

Third, precious metals are also pointing to continued inflation pressures. Gold is close to all-time highs. Moreover, silver, which is a key input for the new economy (technology and clean energy industries), has advanced more than gold in recent months, suggesting that some pressure remains on the real economy, despite the global slowdown. A falling gold-to-silver ratio amid a strong gold performance is a sign that inflationary pressures are still not set to fully abate.

All in all, recent developments in commodity markets do not bode well for the global outlook. The sharp correction in cyclical commodities point to more growth headwinds whereas precious metals suggest high demand for non-US safe-havens and continued inflationary pressures.

Download the PDF version of this weekly commentary in English or عربي