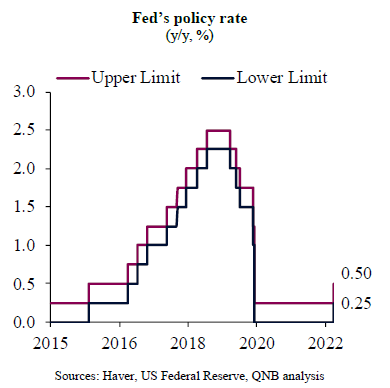

The US Federal Reserve (Fed) is on the move. After several months managing the expectations of market participants about its future actions, the Fed enacted its first policy rate hike since 2016. In fact, during its Federal Open Market Committee (FOMC) meeting in March 16th 2022, the Fed increased its fund target rate by 25 basis points to 0.25-0.5%. This action was widely expected by the market and came on the back of a strong economic recovery and multi-decade high inflation rates. The Fed also provided an outlook for further six rate hikes in 2022.

This piece highlights three main takeaways from the most recent FOMC meeting.

First, the Fed recognized the “stagflationary” nature of the shock created by continuous supply constraints from the pandemic and the Russo-Ukrainian conflict. Quoting the Fed’s Chairman Jerome Powell, “supply disruptions have been larger and longer lasting than anticipated, exacerbated by waves of the virus here and abroad, and price pressures have spread to a broader range of goods and services. Additionally, higher energy prices are driving up overall inflation. The surge in prices of crude oil and other commodities that resulted from Russia’s invasion of Ukraine will put additional upward pressure on near-term inflation here and abroad.” Moreover, the FOMC Summary of Economic Projections displayed significant revisions to its outlook: forecasts for US GDP growth in 2022 were reduced by a median of 122bps, from 4% to 2.8%. Likewise, forecasts for core inflation, which excludes volatile food and energy prices, increased by 140bps, from 2.7% to 4.1%. In other words, the Fed acknowledged that the US macro environment became more “stagflationary,” with lower growth and higher inflation.

Second, the Fed reinforced its hawkish tone about clamping down on high inflation, prioritizing it over other macro concerns, such as the possible economic slowdown of the global economy and more uncertainty associated with geopolitical volatility. In this sense, the Fed surprised the market by presenting a higher projection of 2.8% for policy rates in both 2023 and 2024, implying a more aggressive tightening cycle than before. Importantly, this projection exceeded the so-called “neutral” interest rate projection of 2.4%. The “neutral” interest rate is the theoretical threshold that separates “accommodative” from “tight” monetary conditions. Hence, by setting an expected policy rate above “neutral,” the Fed communicated for the first time in this cycle that it is ready to sacrifice GDP growth in the name of inflation control.

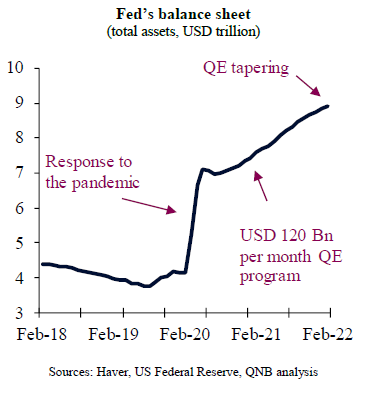

Third, the Fed communicated “excellent progress” on its plans to accelerate the normalization of its balance sheet, i.e., reduce the overall amount of assets it holds. Following the pandemic shock, the Fed balance sheet more than doubled to almost USD 9 trillion, including emergency liquidity injections and the USD 120 billion per month quantitative easing (QE) programme. In December last year, the Fed started a process of “tapering” or reducing its QE programme. In the latest FOMC meeting and speaking engagements, Chairman Powell strongly suggested that quantitative tightening (QT) or balance sheet reduction is formally starting in two months.

All in all, the Fed is doubling down on its “hawkish” pivot towards inflation control. It started raising rates and is ready to hike more aggressively beyond the “neutral” stance, making monetary policy “restrictive” or “tight” already in 2023. Moreover, the Fed also indicated an earlier than expected start to QT. We expect six more rate hikes this year and two more in 2023, for a terminal rate of 2.75-3%. We also see a QT engineered as a passive runoff of assets in the Fed balance sheet, with a cap of USD 100 Bn in asset reduction per month. Powell said he is prepared to raise interest rates by 50bps at the next FOMC meeting in May if needed. That would be the first increase of such magnitude since 2000.

Download the PDF version of this weekly commentary in English or عربي