The US is in the middle of one of the most dramatic economic recoveries ever seen. After the US GDP collapsed by more than 31% annualized in Q2 2020, it rebounded strongly, printing annualized growth rates of 33%, 4% and 6% in the three following quarters to Q1 2021.

Such recovery was only possible due to massive policy stimulus. In fact, the US Federal Reserve (Fed) cut rates aggressively and injected liquidity at an unprecedented scale, while the Treasury championed a fiscal program with measures not seen since World War II and the post-Depression New Deal of the 1930s. According to the International Monetary Fund, US discretionary support measures in response to the Covid-19 shock amounted to almost USD 6 trillion or 30% of the country’s GDP.

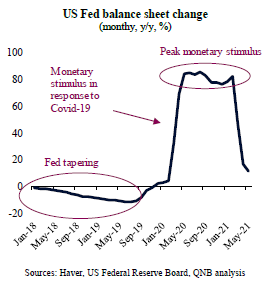

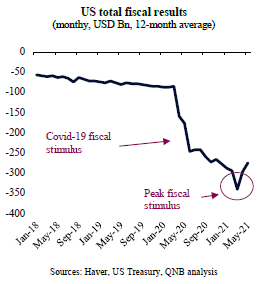

In our view, however, both monetary and fiscal stimulus peaked in the US over the past few months, which suggests that policy will be less supportive for the recovery in H2 this year.

This piece dives into recent changes in monetary and fiscal policies and their consequences for the US macroeconomic picture.

On the monetary front, while policy rates are still close to zero and the large-scale asset purchase program (quantitative easing or QE) remains in place, there are already early signs of policy normalization. At the margin, the Fed balance sheet started to stabilize, pointing to less demand for extraordinary liquidity injections and a much more favourable macroeconomic environment. Moreover, Fed authorities have updated their “forward guidance” or communication about how they are thinking about the Fed’s policy stance. In the Fed’s June Federal Open Market Committee (FOMC) press conference, Chairman Jerome Powell suggested that policymakers started to “think about thinking about tapering [reducing QE].” In addition, FOMC members started to project two policy rate hikes in 2023, coming from zero hikes projected in March 2021. This produced a “hawkish” surprise to markets and tightened financial conditions in the following days.

On the fiscal front, stimulus is likely to have peaked last quarter. This is the case particularly for the more effective type of measures, such as direct cash payments to households and more generous unemployment benefits. The last batch of “stimulus checks” to US households was delivered in April 2021 and the supplements to unemployment programs will expire in September. The monthly US total fiscal deficit is stabilizing and the planned fiscal package for infrastructure spending is more long-term in nature as well as less stimulative, since part of the additional spending will be financed by higher taxes.

All in all, monetary and fiscal policy are still accommodative and will remain so for some time, but the “direction of the tide” is turning. Support is being gradually withdrawn as there is little justification for continued extraordinary stimulus. The recovery is well underway and the threat from the pandemic has been materially reduced by successful mass vaccination campaigns. The fear of inflation with consumption in the US growing “too much, too fast” is expected to subside as more moderate growth eases price pressures. This, in turn, will allow more flexibility for policymakers in the future.

Download the PDF version of this weekly commentary in English or عربي