For several years Emerging Asian economies have been outperforming most other countries when it comes to GDP growth and other activity metrics. This picture has changed recently in the post-pandemic recovery. In recent months, the Delta wave of Covid-19 infections spread quickly in the region, requiring lockdowns and other social distancing measures. The situation was more severe in parts of Southeast Asia, where low vaccination rates and a lack of effective tracing systems produced a challenging environment, in particular for selected countries of the Association of Southeast Asian Nations (ASEAN).

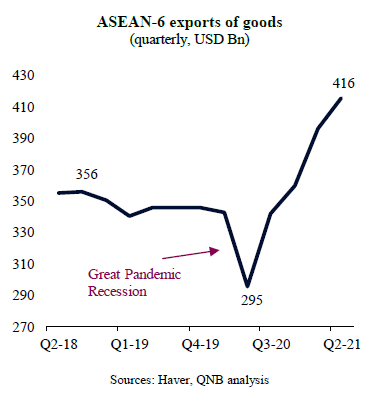

Amid such difficult circumstances, there is still a bright spot for ASEAN economies: the export sector. Boosted by unprecedented manufacturing demand from major advanced economies, exports boomed, partially offsetting the weaknesses in other segments. In fact, exports of goods from ASEAN-6 countries (Indonesia, Thailand, Malaysia, Singapore, the Phillipines and Vietnam) grew 41% since the depths of the global Great Pandemic Recession, far surpassing pre-pandemic levels and reaching all-time highs.

Surprisingly, this has been taking place even as severe bottlenecks and supply constraints from the pandemic persist in certain key segments, such as chip production and shipping logistics.

In our view, however, this support from a buoyant external environment for ASEAN exports is likely to moderate. Three main points underpin our analysis.

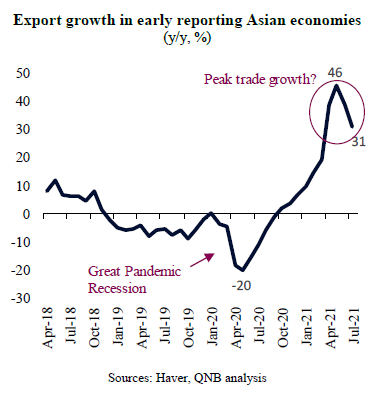

First, high frequency data from key major economies (US, European Union and Japan) is already pointing to a weakening in global trade growth. The flash Purchasing Managers’ Index (PMI) surveys recorded three consecutive months of slowdown in new export orders from advanced economies. This is in line with a significant deceleration of trade growth in early reporting Asian exporters (South Korea, Taiwan, Singapore, and Japan), which tend to lead trade patterns in the ASEAN, given their centrality in regional supply chains. Such movements indicate a slowdown in overall global trade, which should filter through into ASEAN exports.

Second, investor expectations about economic activity in the transportation sector, a key leading indicator for future growth in global trade, had also started to indicate a moderation in demand for physical goods. The Dow Jones Transportation Average, an equity index comprised of airlines, trucking, marine transportation, railroad and delivery companies, whose performance leads global exports by 2-3 months, peaked in May, declining substantially ever since. The index is not only signalling for a pause in global trade acceleration but for a significant deceleration in growth over the coming months. Given that Asia contributes with 35% of total global trade of physical goods, this is expected to dampen the prospects for exports from ASEAN countries.

Third, structural factors also point to a more persistent weakening of demand for consumption goods. Trade growth during the global recovery was driven by exceptional demand for physical goods during the pandemic. This was caused by policy stimulus and a temporary change in spending patterns away from services, as social distancing measures constrained face-to-face activities and the service economy. But both factors are already reversing, in a movement that will likely accelerate in 2022. Strong economic recovery and successful mass vaccination campaigns are leading to a gradual withdrawal of policy stimulus and the re-balancing of spending patterns back to services. Moreover, the demand for physical goods, such as electronics and home building equipment, was “pulled forward” during the pandemic, which means that there is likely to be an extensive period of weaker demand for these goods in the near future. With less spending in consumer goods, the ongoing global trade deceleration is set to gain further momentum, darkening the outlook for ASEAN exports.

All in all, strong ASEAN exports, one of the few positive highlights of the regional economic performance in recent quarters, is likely to moderate over the short- and medium-term. This will add to a challenging macro environment within ASEAN.

Download the PDF version of this weekly commentary in English or عربي