The US Federal Reserve (Fed) is at the forefront of the battle to support the economy against the coronavirus (Covid-19) shock. While fiscal policy tools are more appropriate to provide the relief that companies and households need at this juncture, monetary policy is essential to provide liquidity to the system and even accommodate fiscal policy needs.

The current interventions have already gone above and beyond everything US monetary authorities have ever done. Recently, the Fed Chairman Jerome Powell firmly stated that there are “no limits” to the amount of support officials are willing to provide. In fact, in a matter of a few weeks, the Fed had not only dropped policy rates to zero but also rolled out all the emergency tools developed as a response to the great financial crisis of 2008-09. This includes massive quantitative measures such as asset purchases and the provision of both repo liquidity to money markets and USD swap lines to other central banks.

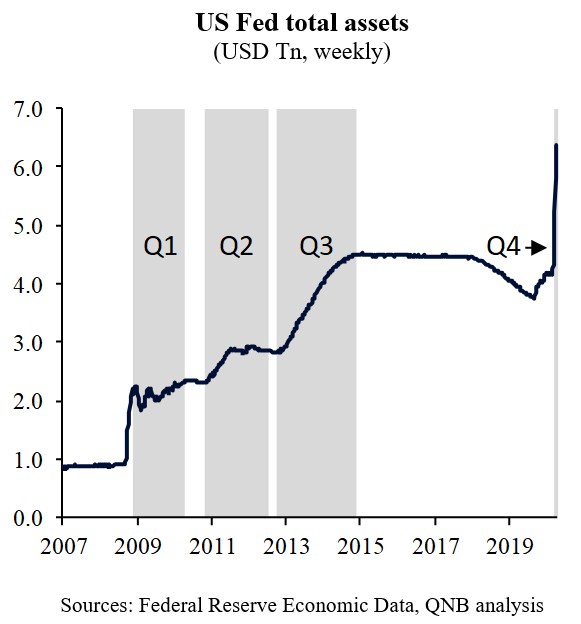

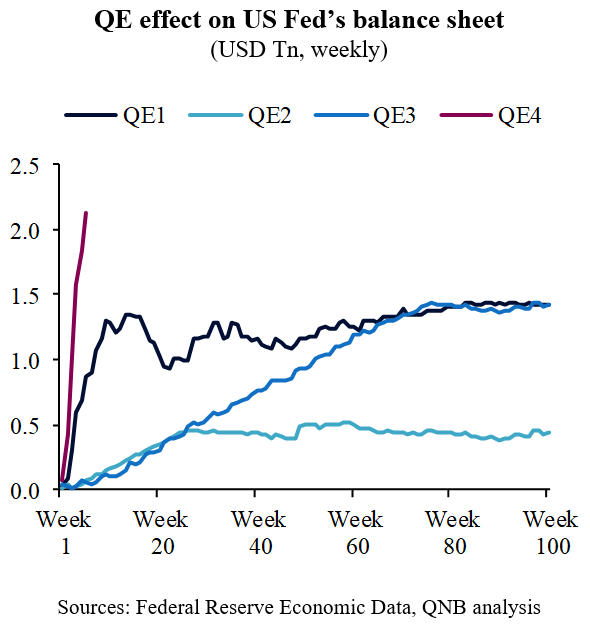

Importantly, the scale, pace and scope of the intervention should be highlighted. The amount of total assets under the Fed’s balance sheet has increased by USD 2.2 trillion (Tn) or 53% in less than two months. This far outpaces previous rounds of quantitative easing and balance sheet expansion. Moreover, the scope of the support now goes much beyond the mandate of previous programs, when asset purchases were limited to Treasuries and agency-issued mortgage backed securities. The new program includes the purchase of securitized retail loans, municipal papers, corporate bonds, commercial papers and even high-yield bond exchange-traded funds. Not surprisingly, several analysts are referring to this new round of measures as “Quantitative Easing (QE) 4” or “QE infinity and beyond.”

In contrast to other periods of economic crisis and market stress, the Fed has acted “ahead of the curve” in recent weeks, anticipating potential problems and with no fear of over-commitment. We see three reasons for the Fed’s hyper-responsiveness this time around.

First, the very nature of the current shock allows for broad political support to bolder actions from monetary authorities. As this crisis is the result of an exogenous pandemic rather than the blow up of financial imbalances, there is less room to debate whether monetary stimulus produces “moral hazard” or bad risk behaviour. Additionally, the immediate hit of social distancing measures on income and employment provides a natural sense of urgency on policymakers.

Second, there is evidence that monetary policy was too tight even before the Covid-19 shock, given the fast negative response of demand to monetary policy normalization in 2017-2018 and the “repo tantrum” of money markets in late 2019. Hence, a massive negative shock from the global spread of Covid-19 amidst non-optimal liquidity conditions requires an even more dramatic acceleration of rate cuts and balance sheet expansion.

Third, given existing structural deficits and high debt levels, sizable government-sponsored relief programs require fiscal-monetary coordination, i.e., central bank intervention to hold interest rates down during a significant fiscal expansion. With the Fed purchasing more Treasuries, a massive supply of bonds can be accommodated with limited pressure on yields. This temporarily creates additional fiscal space to fund relief-related government expenditure.

All in all, the Fed was rapid in recognizing the magnitude of the shock and in providing the appropriated backstops to the US economy. But make no mistake, there is no way back to the old monetary policy framework of a dual mandate (inflation and employment) achieved through mere changes in short-term interest rates. The current mega-intervention to rescue the US economy from a depression will accelerate recent trends, requiring a radical change in monetary policymaking. This will take shape slowly over the next couple of years.

Download the PDF version of this weekly commentary in English or عربي