There are few precedents to the magnitude, breadth and depth of the negative shocks currently facing the Euro area. On the supply side, the legacy of Covid-19 related disruptions was amplified by the most significant energy crisis in decades, as the geopolitical spill overs from the Russo-Ukrainian conflict materialized and negatively affected European utilities. On the demand side, the otherwise strong momentum from the post-pandemic economic re-opening last year is starting to falter, as high and rising inflation is depleting disposable incomes which dampens consumer as well as business sentiment.

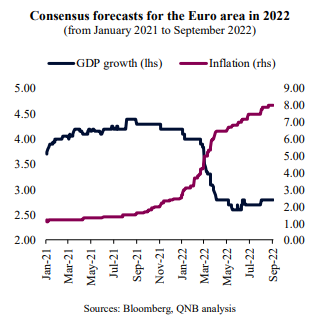

As a result, the Euro area is being severely hit by a combination of low and slowing growth with high and rising inflation.

This creates a macroeconomic backdrop that is particularly challenging for monetary policymaking. High and rising inflation puts pressure on the European Central Bank (ECB) to lean “hawkish” and hike policy rates aggressively. Low and slowing growth magnifies the negative implications of tighter financial conditions, as it increases the cost of capital and widens Euro area inter-country risk premiums. This created a policy dilemma that so far kept the ECB on a “slow moving” stance, trailing the US Federal Reserve (Fed) and some other key central banks.

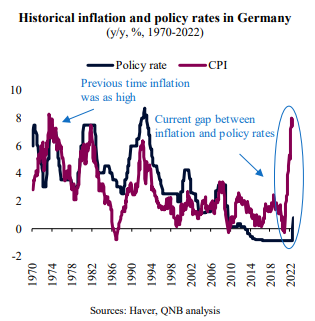

However, the latest ECB policy decision to hike rates by another 75 basis points (bps) was designed to start a process of aggressive tightenting. This is long time overdue as the gap between inflation and policy rates has widened to a level not seen in other historal periods. The ECB had ignored early warning signals and did not initiate the required “catch-up.” Consequently, the measures to be taken now to reduce a gap between 9.1% inflation in August and a policy rate of 0.75% have to be all the more drastic. In our view, similar to the Fed, but a few months later, the ECB is finally starting a journey to restore policy credibility despite the negative effects of the needed actions on growth. Three main facts support our argument.

First, inflation is not only well above the 2% target for the Euro area, but longer-term inflation expectations are de-anchoring rapidly. According to a flagship poll from the Zentrum für Europäische Wirtschaftsforschung, Leibniz Center for European Economic Research (ZEW) Institute in Mannheim, Germany, Euro area inflation expectations are around 4.5% in 2023 and 3% in 2024. This is already by far the most severe inflationary shock the Euro area has ever experienced in its more than 23 years of history. Taking Germany as a proxy for inflation during the pre-Euro era, last time inflation reached rates that were similar to August 2022 highs was in mid-1973. However, at this time the Bundesbank policy rate was at a similar level than inflation. This time, the spread between inflation and policy rates is so wide that the ECB has still a lot more “catch up” to do in terms of rate hikes.

Second, Mediterranean countries of the South or the “periphery” of the Euro area, such as Greece, Italy and Spain, run wider fiscal deficits and accumulate higher levels of indebtedness than more fiscally conservative economies of the North (Germany, Austria, Belgium and the Netherlands). Therefore, Southern European economies are more vulnerable to a more aggressive tightening pivot from the ECB, as higher interest rates increase the debt burden, potentially creating unsustainable sovereign credit dynamics. Aggressive ECB driven interest rate hikes bear the risk of “fragmentation”, an economic dispersion between the North and the South within the Euro area. To prepare the ground for further interest rate hikes, the ECB has created so-called “anti-fragmentation” measures. These are measures that provide the re-allocation of additional ECB funds from the North to the South in case of further stress due to a hawkish monetary policy stance. We conclude from this that the ECB is well prepared to continue a journey of further rate increases in the mid to long-term.

Third, as the gap between US and Euro area policy rates widens, a capital flight towards the US dollar further weakens the EUR. To date, the US Fed rates range from 3-3.25%, versus 0.75% for the Euro area deposit rate. This adds to selling pressure on the EUR. In the absence of a meaningful cycle of ECB rate hikes, the EUR could depreciate further against the USD, adding to inflation pressures as the cost of imported goods increase. This is also in our view an indication that the ECB is well positioned to continue its rate hikes to narrow the interest rate differential to the US.

All in all, the ECB is under pressure to hike rates to be able to get inflation under control; a measure which is for the Fed as well as the ECB at this moment more important than economic growth. Conditions are in place for further aggressive actions from here, as inflation accelerates. In our view, the ECB will hike rates again by 75 bps in October and 50 bps in December, taking rates to 2% before the end of the year. We also expect further interest rate hikes throughout 2023 until the delta between actual inflation and interest rates narrows to an extent that prevents economic value destruction via negative real rates.

Download the PDF version of this weekly commentary in English or عربي