Since the end of World War II, advanced economies have pursued trade liberalization, seeing open markets and lower tariffs as essential pillars of peace, prosperity, and global economic integration. The General Agreement on Tariffs and Trade (GATT), and later the World Trade Organization (WTO), institutionalized this agenda, helping to reduce global average tariffs from double digits to low single digits. This movement gained further momentum in the 1980s and 1990s, with the rise of “free market” supply-side economics thinking, the fall of the Iron Curtain, and a new wave of globalization.

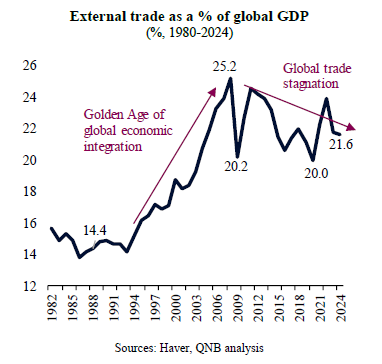

The world saw the rapid expansion of global supply chains, the integration of emerging markets, and the steady erosion of trade barriers as positive forces for growth, efficiency, and price stability. During this time, external trade increase its significance from 14.4% of global GDP to 25.2%.

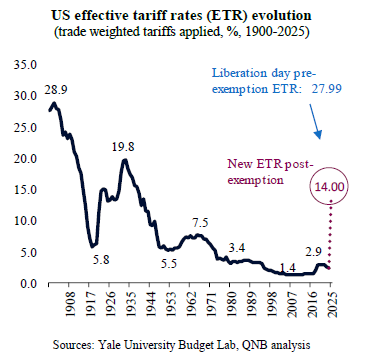

This evolution began to fracture with the Global Financial Crisis in 2008 and the election of Donald Trump in 2016, whose “America First” doctrine brought protectionism back into the mainstream of US economic policy. Yet, while his first term featured targeted tariffs and trade skirmishes – particularly with China – the latest iteration of Trump’s trade policy marks a far more radical departure. On what has come to be called “Liberation Day” on April 2nd, Trump unveiled a sweeping package of tariffs that shocked global markets: headline US effective tariff rates (ETR) surged from 2.9% to 27.99%, before several rounds of exemptions moderated it to 14%. This still represents a manifold increase, placing US tariffs close to 1930s levels.

For some analysts and investors, the magnitude and abrasiveness of the US tariff hike meant not only a pause on trade liberalization, but also potentially the first systematic tentative to reverse it. In our view, however, despite the extraordinary challenges posed by much higher US tariff rates, there are reasons to be optimistic and believe that global economic integration will be resilient towards existing deglobalization threats. Three main factors support our position.

First, the objectives and mandate of the new US tariff packages remain unclear, raising the likelihood of resistance from key market and institutional stakeholders. While the headline rhetoric has emphasized reindustrialization and economic nationalism, the underlying targets of the new tariffs remain ambiguous. Is the goal to reduce the trade deficit, revive domestic manufacturing, isolate strategic rivals, or simply boost federal revenues? These aims are not always mutually reinforcing. For instance, broad-based tariffs that raise input costs can harm US manufacturers and consumers, undercutting the reshoring narrative used to justify them. Meanwhile, targeting allies risks diplomatic backlash and complicates coordination on issues such as isolating strategic competitors or access to critical raw materials.

Markets reacted sharply to the “Liberation Day” tariff announcement, with US Treasury yields rising on fears of de-anchored inflation expectations and lower policy credibility. This not only signals investor scepticism but also creates real economic constraints, as higher borrowing costs threaten growth and complicate fiscal policy. Symmetrically, markets rallied sharply when the new US administration demonstrated more flexibility and pragmatism in conceding exemptions. In addition, the legal foundation for such sweeping tariffs may face scrutiny, as trade policy traditionally falls under congressional authority, and broad applications of national security provisions could invite judicial review. Combined with likely resistance from courts, Congress, and corporate America, these pressures increase the odds of more policy pivots toward an even more pragmatic approach, including further exemptions, rollbacks, and rapid bilateral “deals” to limit the fallout.

Second, tariffs are relatively blunt instruments in a world defined by complex supply chains, digital trade, and fluid capital mobility. Unlike in the mid-20th century, when trade flows were largely bilateral and goods were produced end-to-end in one country, today’s production networks are deeply fragmented and global. A single product might cross multiple borders during assembly, diluting the intended economic effect of country-specific tariffs. Multinational firms are adept at adapting quickly, reconfiguring sourcing, rerouting shipments, or absorbing costs through internal pricing strategies. The result is that tariffs often fail to meaningfully shift production back to the imposing country, while still potentially raising costs for domestic consumers and firms.

Moreover, management tools such as transfer pricing, tax structuring, and jurisdictional arbitrage make it easier for global companies to minimize the financial impact of tariffs. In practice, firms find workarounds faster than policymakers can enforce rules. The more interconnected the global economy becomes, the harder it is to enforce protectionism without inflicting broader collateral damage.

Third, the US may be raising barriers, but the rest of the world is largely moving in the opposite direction. From the European Union (EU) to Asia and Latin America, most major economies continue to view open trade as essential to their growth models – and are actively pursuing deeper integration. Recent examples include the Regional Comprehensive Economic Partnership (RCEP) in Asia, the EU’s expanding trade agreements with key South American (Mercosur) and Indo-Pacific partners, and the African Continental Free Trade Area. Non-US activity spans 73% of global GDP and 87% of trade flows, reinforcing a multipolar trading system that can remain dynamic even without US leadership.

The US retreat may even accelerate cooperation among others, as countries seek to hedge against protectionist shocks and preserve market access. As a result, global firms may increasingly orient towards alternative hubs with more stable trade frameworks, limiting the gravitational pull of US tariffs.

All in all, while the scale of the recent US tariff measures is unprecedented, even after several rounds of exemptions, the forces underpinning global economic integration remain robust. Market pressures, legal constraints, corporate adaptability, and the continued commitment of other major economies to openness all suggest that globalization is not being reversed, but rather geographically reshaped and re-oriented.

Download the PDF version of this weekly commentary in English or عربي