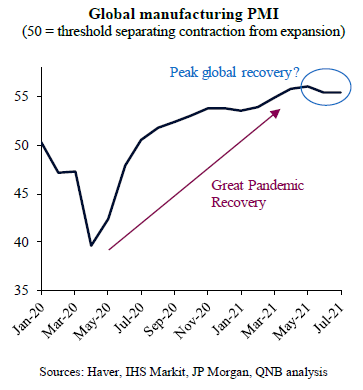

Earlier last year, when the spillovers from the pandemic produced unprecedented negative economic shocks, activity indicators plummeted. The global manufacturing Purchasing Managers’ Index (PMI), a survey-based indicator that measures whether several components of activity improved or deteriorated versus the previous month, bottomed at an all-time low of 39.6 in March 2020. Traditionally, an index reading of 50 serves as a threshold to separate contractionary (below 50) from expansionary (above 50) changes in business conditions.

But as major economies gradually re-opened and policymakers supported demand with aggressive stimulus, the global manufacturing PMI improved markedly, suggesting a big thrust from the economic recovery. In fact, the indicator has been in expansion territory for thirteen months in a row now and even reached all-time highs of 56 in May 2021.

While the latest print of 55.4 for the global manufacturing PMI is rather strong and comfortably within expansion territory, there are signs that growth has peaked and that the global economic recovery is set to moderate moving forward. Our analysis delves into the latest global PMI print and the three main reasons why it is suggesting that peak global recovery is behind us.

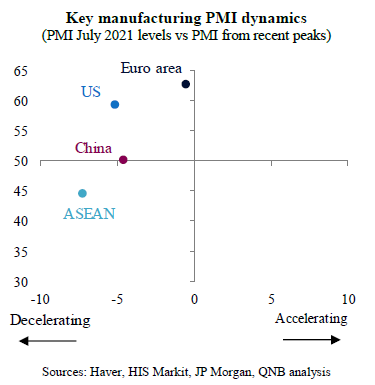

First, while still in expansionary territory, the manufacturing PMIs of all major economies (US, Euro area and China) have been losing momentum, slowing from their recent peaks over the last few months. The US and China, who led the global recovery process after the Great Pandemic Recession, are ahead in this process, with PMI prints declining significantly in the US and closing-in to the 50 neutral level in China. The Euro area, who lagged the leaders in the recovery process, is just starting to slow down.

Second, the Covid-19 Delta variant is taking its toll on manufacturing in some emerging Asia economies, particularly the Association of Southeast Asian Nations (ASEAN). A surge of new Delta cases in ASEAN is leading to more social-distancing measures and a sudden economic contraction in several countries, including Indonesia, Malaysia, Vietnam and Thailand.

Third, Covid-19 related supply constraints in several industries continue to contain manufacturing growth in several economies, including industrial powerhouses such as the US, China and parts of central Europe. In fact, despite a decline from extreme highs for global new orders, other components of PMI surveys are indicating that suppliers’ delivery times continue to lengthen. Supply constraints include low inventory levels as well as bottlenecks and other Covid-related disruptions in manufacturing output and transportation infrastructure, such as ports, containers, and logistic networks. The Asian supply chain is particularly affected, causing knock-on effects in other manufacturing exporters. There is still a large backlog of orders for manufacturers to deliver on over the next quarters, but we expect that supply constraints will only ease meagninfully by mid-2022, the time when key industries are expected to be operating at normalized capacity. This will put a cap on global manufacturing growth for the rest of the year.

All in all, the global manufacturing PMI is still pointing to a continued recovery, but the “second derivative” or rate of change of the recovery is slowing. The slowdown has been driven by both a normalization of demand in major economies and global headwinds such as the Delta variant as well as supply constraints.

Download the PDF version of this weekly commentary in English or عربي