The global economy is recovering strongly from the Covid-19 pandemic. Such rapid economic normalisation would not have been possible without the development of effective treatments and vaccines. The main driver of the recovery has been unprecedented fiscal and monetary stimulus, particularly in the US and China. This boosted consumer demand for manufactured goods, which has benefited “Factory Asia”.

“Factory Asia” is a term that refers to the fact that the majority of consumer goods produced in the world are made in Asia. This is more than just a China story, because some of the most high-tech components are made in countries like Japan, Korea and Taiwan. These components are then assembled in countries with lower labour costs. Historically, China has done the Lion’s share of the assembly, but more recently supply chains have been spreading to other countries less developed countries.

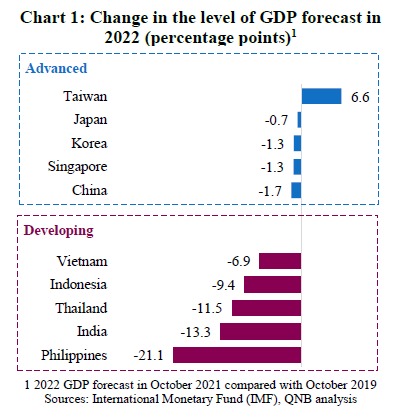

There is clear divergence between the speed and strength of the economic recovery in different countries within “Factory Asia”. We measure this by comparing the level of GDP in 2022 forecast by the IMF in its latest World Economic Outlook, with the level forecast before the pandemic in October 2019 (Chart 1). What we see is that advanced countries are recovering more strongly from the pandemic than developing countries. This article seeks to explain this divergence by focusing on three key factors; the importance of manufacturing, levels of vaccination and the amount of policy space.

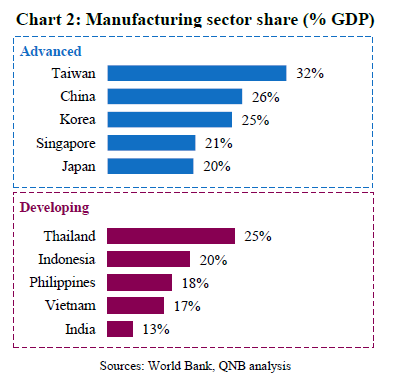

First, we can see that advanced countries tend to have a higher share of manufacturing than developing countries, averaging 25% of GDP relative to only 15% (Chart 2). Large manufacturing sectors mean that countries within “Factory Asia” are all benefiting from robust global demand for consumer goods. However, the larger share of manufacturing in advanced countries means that they benefit the most. This helps to explain why their economies are expected to be only slightly below their pre-crisis trend in 2022, and even above in the case of Taiwan.

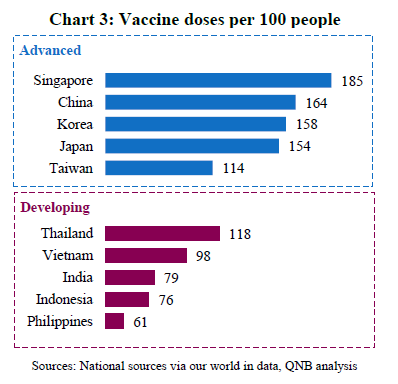

Second, the Delta variant hit “Factory Asia” particularly hard during Q2 and Q3 of this year. The main reason was that the Delta variant is so much more infectious than the original virus. Fortunately, after a slow start, Asian countries have now made significant progress with vaccination campaigns. However, despite this progress there remains a clear divergence between countries, with advanced countries administering many more vaccine doses per hundred people than developing countries (Chart 3). The main reason for this is that advanced countries had earlier access to vaccines and more established infrastructure for transporting, storing and administering them.

The slow start to vaccination campaigns and still-low level of vaccination in developing countries helps explain why they were hit harder by the Delta variant and therefore less able to benefit from the exceptionally strong demand for consumer goods. We expect some catch-up in vaccinations next year, but this is too late for developing countries to benefit from the full force of the consumer boom, which we expect to moderate slightly next year.

Third, another important factor to consider is the amount of fiscal and monetary policy space. Fiscal and monetary stimulus allow countries to support consumption and investment through periods of economic disruption like the pandemic. Advanced countries typically have greater policy space than developing countries, which is another reason why their recovery from the pandemic is stronger. High global inflation and tightening global financial conditions mean that the benefit of having greater policy space is more likely to increase than decrease next year. This will make it more difficult for developing countries to catch up with the advanced countries.

In conclusion, the relative size of manufacturing sectors, effectiveness of vaccination campaigns and amount of policy space all help to explain the divergence in the speed and strength of recovery from the pandemic within “Factory Asia”. The core factors are relatively persistent, so we expect advanced countries to remain around their pre-pandemic growth trend, whereas we do not expect developing countries to catch up to their pre-pandemic trend within the next two years.

Download the PDF version of this weekly commentary in English or عربي