Uncertainty has been high in recent months on the back of the new US administration, which has been rapidly enacting an aggressive “policy change agenda” with deep potential implications for both consumers and investors.

Even in more ordinary periods, when governments adopt a more “business as usual” approach, it is notoriously difficult to read too much into the tea leaves of US policymaking. Currently, under a more “revisionist” Trump government, it is particularly challenging to conduct a more comprehensive analysis of economic policies and their impact on growth and inflation. Hence, we turn to markets to analyse what the evolution and direction of key asset classes is telling us about the US economy.

Financial markets provide critical insights into the overall health of the US economy over the short- and medium-term, given that they are a reflection of real world investment decisions by well-informed agents that are constantly trying to access or discount the future.

In our view, price action across asset classes seems to sustain a deteriorating macro view of slowing growth, despite any potential optimism with tax cuts or de-regulation. Three factors support this position.

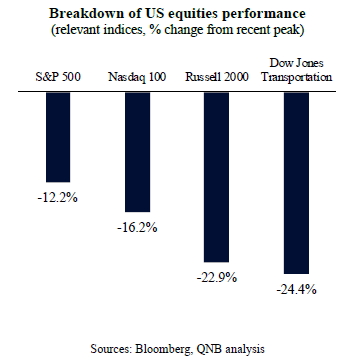

First, equity prices are clearly pointing to a sharp reversal of sentiment from bullishness to bearishness amid significant risks for earnings growth prospects. The two main US equity indices, the S&P 500 and the Nasdaq 100, are down materially from their recent peaks. Importantly, a deeper look "inside of the equity market," comparing performance across sectors and factors, suggests that capital is moving towards a more defensive position, preferring value to growth and utilities over cyclicals. In fact, cyclical equities or stocks that are more sensitive to changes in the real economy are pointing to a much more challenging environment. These cyclical stocks, including small-caps (Russell 2000) and transportation players (airlines, trucking, marine transportation, railroad and delivery companies), whose performance tend to lead economic activity, are not only underperforming vis-à-vis the major indices but are well within "bear market" territory, i.e., more than 20% decline from recent highs. Cyclical bear markets tend to be associated with periods of protracted economic weakness or recessions.

Second, the more macro-sensitive bond market is also flashing warning signs. In recent weeks, the spread between high yield corporate bonds and long-dated government papers started to widen, implying increased risk aversion of bond investors. Moreover, different metrics from the US government yield curve, which is the interest rate differential between similar instruments with different maturities, have inverted. For example, the benchmark spread between 10-year Treasury notes and Fed fund rates turned negative again in February 2025. This benchmark spread is a leading indicator of recessions as lower long yields imply lower growth expectations and higher short yields imply less benign financial conditions. This sign has flashed in advance of the last seven US recessions since the early 1960s, usually giving a year or two of warning before a recession starts. Shortly after that, in a perhaps even more relevant move, long-dated US Treasury yields spiked, signalling more severe market stress and doubts about the future of US Treasuries as a “safe haven,” due to more extreme US policy uncertainty.

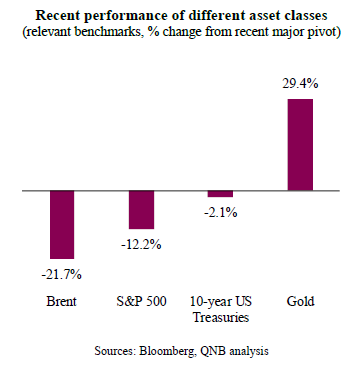

Third, key commodity markets are also sending strong signs of caution and weakness ahead. Strong price action for precious metals, and particularly gold, is likely reflecting higher geopolitical risk premium and institutional demand for non-jurisdictional assets. Gold prices are close to all-time highs, up almost 30% since September 2024 to close to 3,230/troy oz. However, crude oil prices, key as an input for real economic activity like transportation and power generation, are more significantly below its recent highs and overall underperforming gold. This demonstrates a fading impulse for growth amid strong demand for non-jurisdictional safe-haven protection.

All in all, market sentiment has turned and different asset classes are pointing to a more challenging macro environment for the US, including equities, bond markets and commodities. While we believe that calls for a recession could be premature, given the high point of departure for growth and the potential for more pragmatism in policymaking, we do expect a significant slowdown of the US economy to a headline GDP growth of 1.4% in 2025, from 2.8% in 2024.

Download the PDF version of this weekly commentary in

English

or

عربي