The global economy is in the middle of what could be one of the most dramatic economic recoveries since World War II. After the Covid-19 shock produced the sharpest and deepest slowdown on record in Q2 2020, aggressive policy stimulus and the temporary containment of the pandemic led to a significant rebound last quarter. While the global economy is not out of the woods yet, a full-blown “second wave” of severe epidemics could create a “double dip recession”. The recovery has so far been promising, with several countries and sectors showcasing remarkable economic strength.

But which sectors are leading the recovery and what does that tell us about broader macro trends? The answer for this question is now more important than ever. Covid-19 impacted several sectors, such as the aviation, healthcare, transport, tourism and brick and mortar retail industries. The pandemic also led to modifications in consumer behaviour. Both will drive market changes with long lasting effects on economic activity, resulting in leaders and laggards.

This analysis delves into equity markets to unpack the new leaders in their future economic expansion. So far, four big themes come to the forefront.

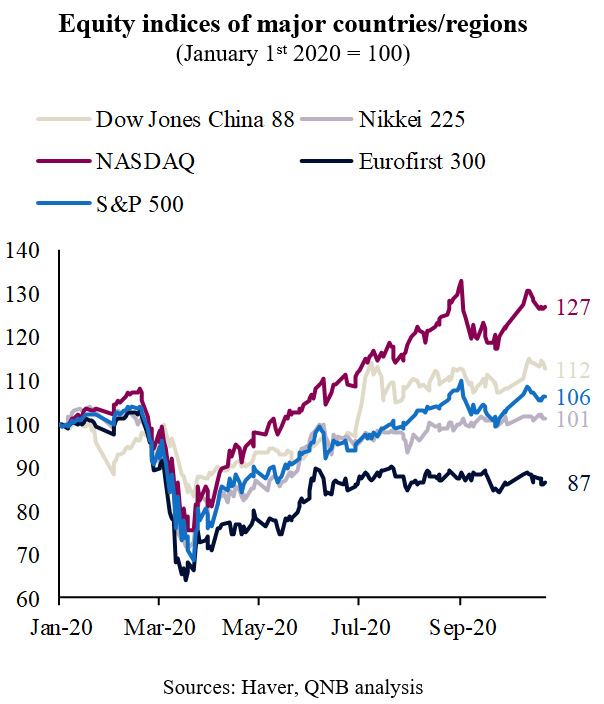

First, “growth” is outperforming “value” when it comes to investors’ preferences. In other words, companies in sectors that are growing fast continue to be favoured against companies in more stable sectors. Weak long-term growth in advanced economies and low policy rates put a special focus on companies with high potential for future earnings and sales growth. This tends to favor the “new economy” of technology versus the “old economy” of traditional capital intensive industries. In terms of geographies, this favors the dynamic, tech-heavyUS and Chinese indices over other markets when companies are listed

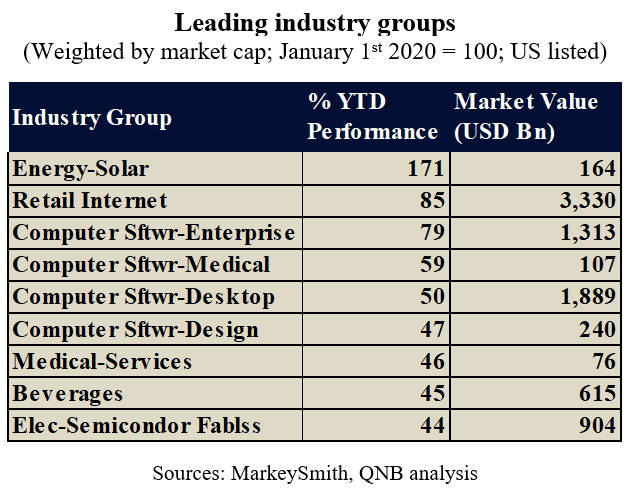

Second, initiatives that support a low-carbon economy are becoming a major market trend. This includes enterprises that promote technologies to “de-carbonize” power, mobility, agriculture and industry. A sharper than expected recovery in demand for solar energy products and investor optimism about positive regulatory changes for the sector triggered a clean energy wave in equity markets.

Third, Covid-19 strengthened the demand for digitalization of services and businesses. With lockdowns and social distancing measures implemented globally, shifts from in-person sales to e-commerce and from cash to digital payments were expedited everywhere. The digital transformation of business and workflow automation also gained ground, especially as work-from-home and cost reduction became paramount. Such trends also led to a rise in the demand for electronic products, boosting the semiconductor industry.

Fourth, the pandemic accelerated the demand for and investments into the healthcare industry and life sciences in general, propping up the pharma industry, bio-tech and a plethora of other medical related companies. This goes beyond the global race for a successful vaccine and the sudden increase in demand for personal protective equipment, including the application of robotics in surgery, the digitalization of health care and the use of artificial intelligence in medicine.

All in all, Covid-19 seems to have acted as an accelerant to trends that were already taking place globally. But the magnitude of the shock, and its effects on the behaviour of individuals and firms, is likely to have contributed to the break down of deeply seated resistances to technological change.

Download the PDF version of this weekly commentary in English or عربي