Since the beginning of the Covid-pandemic, an extraordinary sequence of global shocks propelled inflation rates in advanced economies to levels not witnessed in decades. The pandemic led to lockdowns that produced constraints in supply, while loose monetary and fiscal policies fuelled demand. These pressures on prices were further elevated with the reopening of the economies as the demand for services increased and the Russo-Ukrainian war triggered a commodity shock. By mid-2022, inflation reached 9.1% in the U.S., and a double digit record of 10.7% in the Euro-Area. These levels were far from the 2% percent targets of monetary policy, activating the alarms of central bankers.

Despite some initial hesitation, central banks reacted strongly to bring inflation rates down to their targets. The European Central Bank (ECB) embarked on a record policy rate tightening cycle, increasing its main refinancing rate by 450 basis points to 4.5%. In the U.S., the Federal Reserve Board (FRB or “Fed”) increased its policy rates by 525 bps to 5.5%.

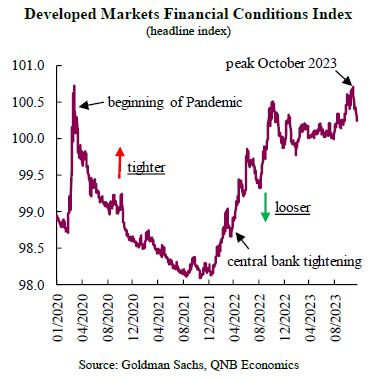

These cycles have had a significant impact on financial markets. The Financial Conditions Index provides an informative indicator of the cost of credit, by combining information of short- and long-term interest rates, as well as credit spreads. The index began a steady upward trend at the beginning of 2022, and has remained elevated since the end of last year. In addition to higher costs, the volumes of credit are contracting. In our view, tight financial conditions will persist in the U.S. and the Euro-Area through the first half of 2024. In this article, we discuss the two main factors that support our outlook.

First, despite our expectation for rate cuts by major central banks starting in Q2 2024, high policy rates should remain in place over the coming months. Inflation rates have fallen considerably from their peaks, with headline measures close to 3% in both economies. However, to a large extent, this is accounted for by the fall in energy prices, which are driven by international events. Core inflation, which excludes the more volatile prices of goods such as food and energy, and is typically more persistent, still remains above 4%, far above the comfort zone of policy makers, favouring a wait and see approach.

Central banks pay special attention to the core measure of prices given its looming persistence. Additionally, this gauge puts the spotlight on prices determined by domestic factors and better reflects underlying trends. The current levels of inflation have not been witnessed in the history of the Euro-Area, and since the early 1990s in the U.S., in a very different economic environment. Given the lack of recent experience in managing surges of prices of this magnitude, policymakers will be cautious in their timing to start cutting interest rates.

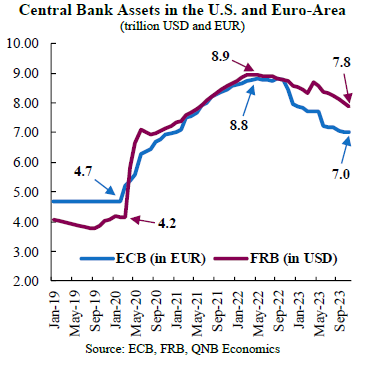

Second, the ECB and FRB will continue to drain liquidity in the banking systems by reverting the balance sheet expansions that were put in place during the Covid-pandemic. These policies were initially implemented due to exceptional circumstances to mitigate the consequences of the pandemic. In order to normalise its balance sheet, the Fed began its gradual reduction in June 2022, and has to date decreased its size by USD 1.1 trillion from a peak of USD 8.9 trillion. Similarly, the assets of the Eurosystem (the ECB plus the national central banks of the Euro-Area) have fallen by EUR 1.8 trillion from their peak of EUR 8.8 trillion. This process of quantitative tightening will continue through 2024, reducing the excess liquidity in the financial system and the availability of credit for firms and households.

The latest bank lending surveys of the ECB and the Fed show that credit standards have continued to tighten in recent quarters at a pace comparable to episodes such as the European Sovereign Debt Crisis or the Global Financial Crisis. Decreased liquidity and tighter lending standards, together with higher costs of loans, have translated into lower volumes of credit, which are now contracting in real terms. This maintains overall financial consitions tight.

Download the PDF version of this weekly commentary in English or عربي