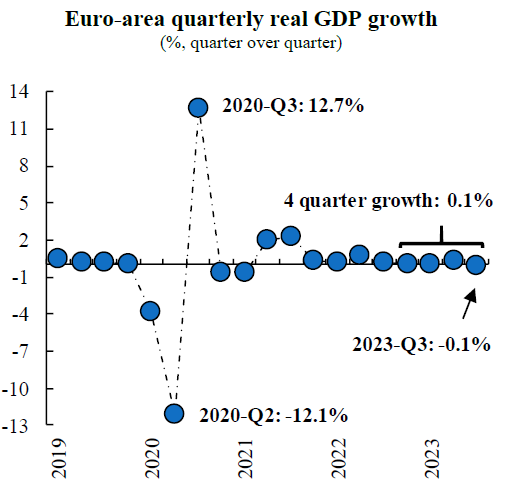

Since 2022, the resilience of the Euro-area economy has been pushed to its limits due to significant headwinds from high energy prices, record monetary policy tightening, global uncertainty, and weak external demand. As a result, growth has stagnated over the last four quarters, with real GDP expanding only 0.1%.

Going forward, the outlook remains grim. Business sentiment across sectors is at its lowest since the Covid-pandemic, and at a level that has only been worse in deeply contractionary episodes, such as the global financial crisis or the sovereign debt crisis. With sentiment and business surveys pointing to further declines in activity in the final quarter of the year, the region currently stands on the brink of a recession, defined as two consecutive quarters of negative growth.

In this article, we discuss the main factors that signal a significant likelihood that the Euro-area economy will end this year in a recession.

First, we expect financial conditions to become tighter on the back of policy rate hikes and the normalisation of the central bank balance sheet. The interest rate tightening cycle of the European Central Bank (ECB) is likely to be over, after accumulating an increase of 450 basis points leaving the main refinancing rate at 4.5%, the highest in more than 20 years. However, in spite of the expected end in tightening, it is widely understood that the transmission of changes in policy rates to households and firms is gradual, and therefore the impact of previous tightening is yet to be fully felt in consumption and investment.

In addition to the higher costs of credit, the ECB continues its process of balance sheet normalisation. This implies the reversal of the extraordinary measures put in place through different asset purchase programs during the Covid-pandemic, which results in reduced liquidity in financial markets. As a result, banks have reported stricter credit standards for households and firms throughout the year, and are expected to tighten further. Consequently, credit volumes continue to contract, weighing on economic activity.

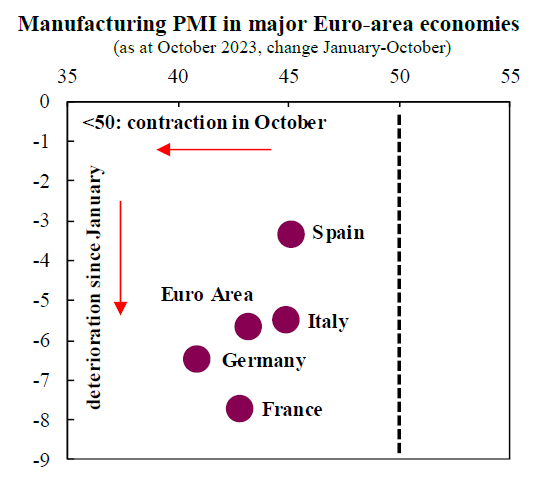

Second, the manufacturing recession continues to deteriorate, and is now broad-based across the major economies in the region. The Manufacturing Purchasing Managers Indices (PMI) reflects these conditions well. The PMI is a survey-based indicator that provides a measurement of improvement or deterioration in economic activity. An index level of 50 serves as a threshold to separate contractionary (below 50) from expansionary (above 50) business conditions. The PMI shows that manufacturing has deteriorated continuously this year and further worsened in October.

Pessimism affected Germany’s industrial sector first, given its greater exposure to the decelerating Chinese economy and energy constraints. But negative conditions have become extensive in the four major economies (Germany, France, Italy, and Spain), which account for 73% of the region’s GDP. Furthermore, headwinds from energy constraints and weak external demand will continue to suppress manufacturing activity, signalling a negative contribution to total output in the last quarter of the year.

All in all, following a year of economic stagnation, in our view the Euro-area is likely to end 2023 in recession, given tight financial conditions, and a manufacturing sector undergoing a deep contraction. Looking ahead, we expect a recovery in the manufacturing cycle to partially mitigate a slowdown in consumer spending. This would help the Euro-area economy to move out of recession around the first quarter of 2024. Nevertheless, the overall economic remains stagnant and weak.

Download the PDF version of this weekly commentary in English or عربي