The United Kingdom (UK) formally left the European Union (EU) on the 1st of January 2020 under the so-called “Withdrawal Agreement”, but entered an extendable “transition period” until the end of this year. Despite the global Covid-19 pandemic, UK Prime Minister Boris Johnson has so far stuck to his commitment not to extend the transition period. Negotiations between the two sides have identified a range of key issues but both sides have drawn red battle lines. Johnson says a deal must have been concluded by the European Council Summit on the 15th of October or the UK would walk away. However, that is likely to be a soft deadline and we expect negotiations to continue.

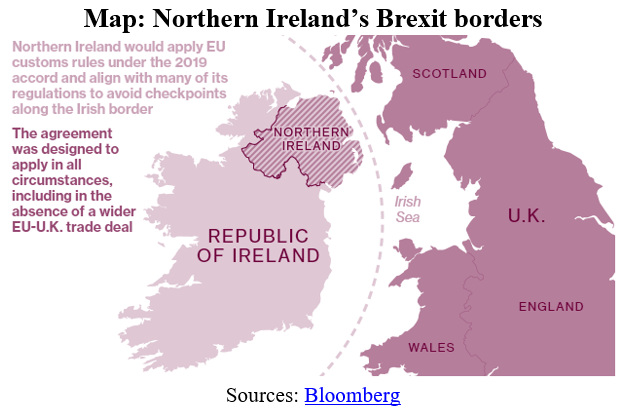

The Withdrawal Agreement agreed on a new type of boundary in the Irish Sea (see map). So, in the absence of a new agreement, Northern Ireland would be forced to obey the rules of the EU’s single market, including those covering areas, such as food safety and state aid. That is unacceptable to the UK, which has responded by introducing legislation which gives it unilateral powers to align policy in these areas with that of the UK rather than the EU. Unfortunately, even the UK government admits that would breach the terms of the Withdrawal Agreement and hence also effectively breaks international law. In response, the EU has started legal proceedings to force the UK to negotiate a mutually acceptable deal.

We review four remaining differences over level playing field provisions, fisheries, the actual structure of the deal, and Northern Ireland

First, the EU insists on a level playing field. The EU expects the UK to guarantee that it will not undercut certain EU regulations in order to gain a competitive advantage (e.g., on state aid, labour standards, environmental standards, taxation) in exchange for continued access to EU markets. However, the UK argues that this is unprecedented for a trade deal and is instead insisting on the freedom to diverge from EU rules e.g., to be able to provide financial support to firms, limited only by international (rather than EU) rules, or to cut taxes below EU thresholds.

Second, the two sides disagree over EU access to fishing in the UK’s territorial waters. The UK wants annual negotiations on access to waters and fishing quotas, while the EU is seeking to maintain existing reciprocal access and stable quota shares.

Third, they even differ on the structure of the deal. The EU is seeking a single integrated agreement that covers all aspects of the future economic relationship. However, the UK wants to separate the trade deal, with its own legal agreements, from other aspects, such as aviation, security, energy, fisheries etc.

Finally, and perhaps the most fraught issue is the details of Northern Irish trade after the transition period ends. In particular, the extent of customs requirements and regulatory controls for goods moving between Northern Ireland and the rest of the UK. The EU wants to prevent goods that do not meet EU rules from leaking into the European Single Market, whilst the UK wants to ensure unfettered movement within its own internal market.

Each side claims to have the upper hand, but with negotiators running out of time, the difference between “deal” and “no deal” is narrowing and the risk of a “no-deal” trading relationship have risen.

Despite, both sides talking tough and seeming unwilling to compromise on their red lines, we still think a partial trade deal is the most probable outcome. Indeed, both sides are still engaged in talks and, in our view, a deal is in the interests of both sides. Therefore, we expect a deal on goods trade to be agreed and at least partially implemented by the end of the year. We see the UK as most likely to compromise on fisheries and the “state aid” component of a level playing field

Such a deal is unlikely to include regulatory alignment, which will result in border disruption and trade in services will remain mostly out of scope of the deal. For example, there could be new customs requirements, border checks, testing requirements, and frictions in cross-border services trade. Barriers to bilateral trade will be most pronounced in areas of regulatory divergence, and are likely to lead to higher administrative costs for both UK and EU businesses.

Brexit remains an unfortunate headwind to the economic outlook for the UK. The UK government and Bank of England will therefore need to maintain significant fiscal and monetary stimulus to deliver a still-weak recovery from the deep recession caused by Covid-19. There is also the uncomfortable possibility that continental Europe may enjoy a stronger and more robust recovery than the UK.

Download the PDF version of this weekly commentary in English or عربي