More than two years since Covid-19 was first discovered, China again appears to be the epicentre of the pandemic. At least that’s the take-away from recent headlines. However, focusing too much on China distracts us from the bigger global picture, which is that the Covid-19 pandemic is fading. Indeed, thanks mainly to effective vaccines, Covid-19 is gradually becoming an endemic disease that we simply have to learn to live with.

This week we review key pandemic indicators to demonstrate that the pandemic is indeed fading, before moving on to consider the substantial risks that remain. We see three major risks: the battle between Omicron and China’s “dynamic zero” policy; and the possibility that a more deadly variant emerges; and the lingering legacy of the pandemic itself and the policy response from governments.

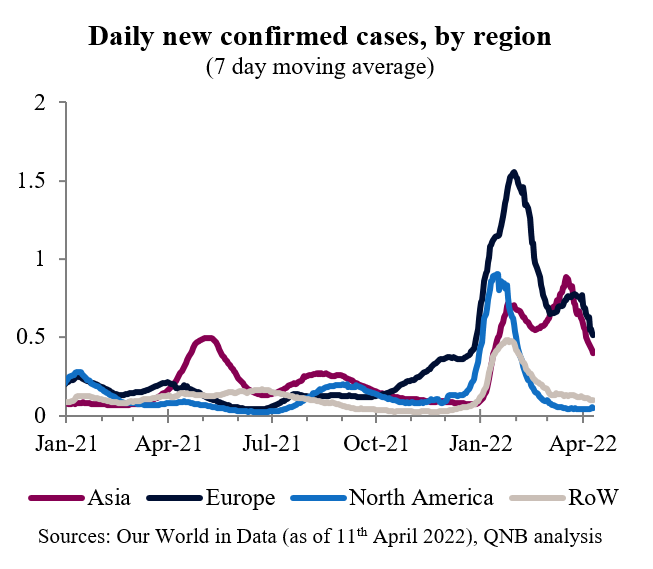

We are well past the peak of the wave of the pandemic caused by Omicron and its sub-variants. One million (Mn) Covid-19 cases per day were recorded globally in the 7 days ending on the 10th April, down from a peak of 3.4 Mn in late January 2022. However, case numbers remain much higher in Europe and Asia, relative to North America and the Rest of the World (RoW), see chart. Deaths attributed to Covid-19 have fallen even more rapidly to an average of only 3,400 per day, down from a peak of 11,000 in February 2022, and less than a third of the peaks caused by other variants last year. Dividing the number of deaths by cases gives a crude estimate of the mortality rate, which has fallen to 0.3%, down from a peak of 7.4% in April 2020. The broad distribution of effective vaccines is the main reason that the mortality rate has fallen so much. Indeed, over 11 billion (Bn) vaccine doses have been administered, including 1.7 Bn boosters. As a result, over 5 Bn people have received at least one dose and 4.6 Bn have been fully vaccinated. The high and rising level of vaccinations globally is reducing the need for strict lockdowns and other mitigation measures in most countries, with the obvious exception of China. In turn, this means that the headwind from the pandemic on the global economy is fading. However, risks remain.

First, the Omicron variant is causing serious problems in China, which has recorded 19,000 new Covid cases per day on average over the past week, surpassing the previous peak in early 2020. The surge in cases is because Omicron is so much more infectious than previous variants. Indeed, China is struggling to bring cases back under control, even with stringent lockdowns in major cities like Shanghai and Shenzhen. Goldman Sachs estimate that 18% of the economy is currently facing lockdowns and expect containment policies to remain in place until late this year. As a result, China faces the costs of both attempting to contain Omicron as well as the possibility that containment fails and the virus runs through a relatively unprotected population. Therefore, expect weaker Chinese growth in 2022, with knock-on effects on the outlook for growth in Asia and the whole global economy.

Second, the still-high number of Covid-19 infections in the global population provides the virus with ample opportunities to mutate and produce new variants. The process of evolution and natural selection favours the creation of new variants which are more infections, but less deadly. Hopefully, scientists can develop booster shots tailored to new variants, or pan-coronavirus vaccines able to tackle all variants. However, there is still a risk that we are faced with a new variant, which is more deadly and still highly infectious. Indeed, U.K. Prime Minister Boris Johnson has refused to rule out further Covid-19 lockdowns, saying “there could be a new variant more deadly” that emerges in future.

To conclude, we draw our key pandemic indicators and risks together. The pandemic is fading, but case numbers remain high, as does the likelihood that we face future waves as new variants emerge. This means that the global economy should continue to benefit from rebounding economic activity in many countries. In contrast, China’s struggles with Omicron will act as a drag on the global economy through both lower domestic consumption and weaker exports, increasing stress on global shipping and supply chains.

Download the PDF version of this weekly commentary in English or عربي