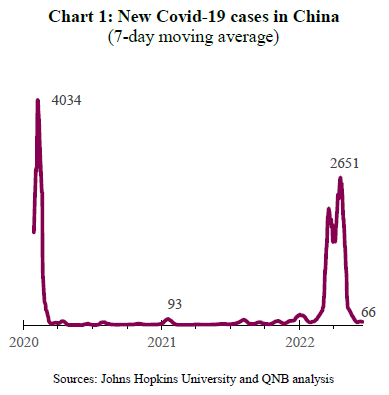

China’s Covid-Zero strategy was effective in 2020

China is where Covid-19 was first discovered in late 2019 and then experienced the first wave of the pandemic in early 2020 (Chart 1). In response, China engaged in hard lockdowns, extensive testing and contact tracing. This strategy has become known as the “Covid-Zero” because it seeks to reduce community transmission of the virus to zero. Covid-Zero was highly effective at supressing the initial wave of the pandemic, bringing down the number of infections to a low level, which was then maintained throughout 2020 and 2021. This allowed the Chinese economy to re-open and grow more strongly than any major economy over the past two years.

Omicron hit in 2022, requiring hard lockdowns

Unfortunately, Covid-19 has evolved into the much more infectious Omicron variant, which arrived in China in early 2022. Omicron can also evade some of the protection offered by China’s vaccine, which led to a surge in new cases of Covid-19 to levels not seen since 2020 (Chart 1).

A delayed response meant that hard lockdowns and extensive social distancing measures were again required to supress the virus. This included the unprecedented lockdown of millions of people in Shanghai for almost two months and tight restrictions on movement in other regions. Lockdowns covered areas that generate 40% of China’s GDP and ship 80% of its exports. This huge effort, led to a significant economic slowdown, but also meant that new cases peaked in April 2022 and have subsequently fallen back to a low level.

China has pivoted to a cat-and mouse approach

New infections continue to pop up in China despite Covid-Zero because Omicron is so infectious and can evade vaccines. As a result, officials are engaged in a constant game of “cat-and-mouse”, chasing the virus with testing and contract tracing, then stamping it out with isolation via focused local lockdowns. Implementation of this cat-and-mouse approach involves setting up tens of thousands of testing booths across China’s cities and economic heartland. This approach is particularly evident in China’s two largest cities, Shanghai and Beijing, and also in Shenzhen, China’s technology hub. The investment in testing underscores China’s commitment to Covid-Zero, an approach that has made China the only country in the world to contain the highly infectious Omicron variant.

Massive testing an expensive economic headwind

Although the cat-and-mouse approach is much less damaging for economic activity than hard lockdowns, it imposes a persistent cost and represents a significant headwind to China’s GDP growth. Goldman Sachs estimate the current cost of testing to be around USD 30 billion. That is less than 0.2% of China’s 2021 output, but Nomura analysts estimate that the cost could rise to 1.8% of GDP if smaller cities follow suit and 70% of the population is tested every 48 hours. In addition, analysts at Soochow Securities estimate that the current restrictions could knock 1.1 percentage points off China’s domestic growth for the year.

Policy support seeks to avoid a hard landing

Chinese authorities are under significant pressure to control the pandemic and drive an economic recovery ahead of the party congress in the second half of the year. Indeed, in a recent speech, Chinese Deputy Premier Liu He, reassured the public that the government would not allow for a “hard landing” of the economy. He announced measures that would support the struggling real estate sector but also help the “finalization” of the business regulation tightening cycle that caused uncertainty and losses in Chinese equity markets. However, these measures of policy stimulus in the form of tax breaks, more government spending and monetary easing have not yet been particularly effective at driving growth.

China’s outlook weaker than pre-pandemic trend

In conclusion, China’s cat-and mouse approach to its Covid-zero strategy has been effective at reducing new infections to a low level. However, it comes at a significant cost and will act as a persistent headwind to GDP growth. Counteracting this is policy stimulus that could provide some support for the economy, however this stimulus has so far been less effective than in the past.

The combination of Covid-Zero headwinds and relatively ineffective policy stimulus means that we expect only a weak economic recovery in China More specifically, we expect these two factors to lead to Chinese GDP growth of only 4.8% in 2022 and 5.3% in 2023, well below its pre-pandemic trend.

Download the PDF version of this weekly commentary in English or عربي