As a global recession becomes increasingly likely, we turn our attention to two key challenges facing the Euro area (EA).

First, energy security is challenged because of Europe’s dependence on Russian gas, with gas flows cut drastically due to the impact the Russo-Ukraine war and its resulting sanctions on Russia. Consequently, EA governments need to handle skyrocketing energy prices with direct fiscal transfers to vulnerable households and failing industries to assist them through the winter.

Second, government debt levels were already high in a number of countries before the war and following the pandemic with some of them having never recovered from the Euro area sovereign debt crisis.

Sources: European Electricity Review, QNB analysis

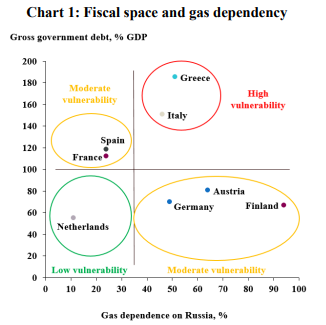

This week, we analyse the implications for selected EA countries with regards to their level of gross government debt as well as the dependence on Russian gas (See Chart 1). This allows us to separate countries into three groups, based on their vulnerability: high, moderate and low. The most vulnerable countries have a high dependence on Russian gas as well as a high government debt to GDP ratio.

High vulnerability: Greece and Italy are particularly vulnerable as they are highly exposed to the energy crisis and their governments have limited resources to fund alternatives, provide support for citizens and bailout strategic corporates.

Moderate vulnerability: Spain and France are relatively insulated from the gas crisis but high debt levels limit their margin for manoeuvre. On the opposite side, Austria, Germany, and Finland are heavily exposed to the gas crisis, but have more resources to absorb the negative economic effects.

Low vulnerability: The Netherlands is the safer side, with a low exposure to the energy crisis and relatively high fiscal space.

These indicators of fiscal space and gas dependency highlight the relative vulnerability of different countries within the EA, but also represent headwinds for the EA as a whole. In addition, this divergence will make it hard for EA institutions to coordinate the policy response across countries. Therefore, as these challenges represent headwinds, the economic outlook for the whole of the EA has deteriorated.

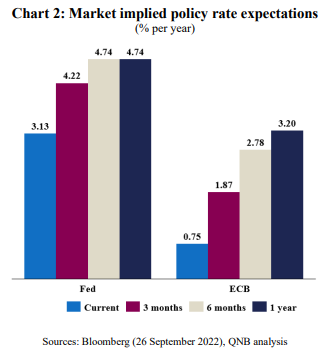

A third headwind comes from the ECB being forced to follow the Fed and hike interest rates aggressively (Chart 2). This impacts Euro area countries directly by increasing the cost while at the same time reducing the availability of credit. But it also spills-over to the rest of the EA as independent central banks are faced with the same challenges: controlling inflation and preventing too much currency depreciation/weakness.

Download the PDF version of this weekly commentary in English or عربي