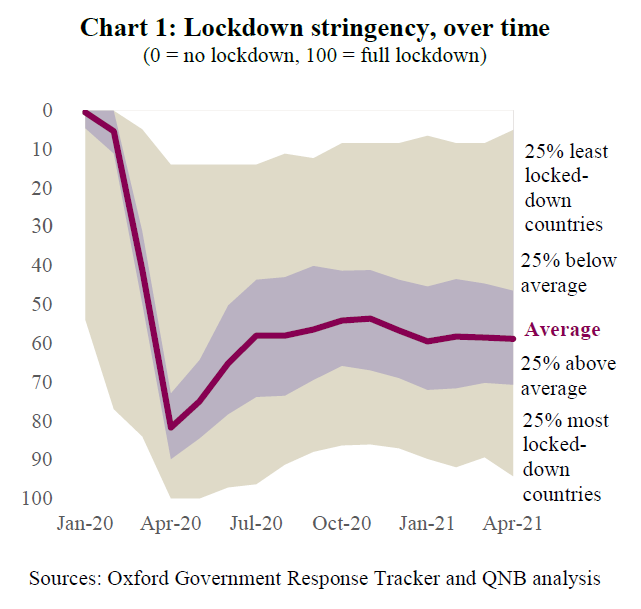

In response to the global Covid-19 pandemic, countries across the world implemented a range of restrictive policies to impose social distancing and help reduce the severity of the pandemic. Most countries introduced tight lockdowns in April last year before relaxing them gradually during the rest of the year (Chart 1). A number of countries then needed to tighten their lockdowns again to respond to a surge in cases of Covid-19 during winter in the Northern Hemisphere. However, every country is different and that has led to a wide range of approaches to managing the pandemic.

A lot has already been written on the topic of government responses to the pandemic. The main metric used for lockdowns in most analyses is the Oxford Coronavirus Government Response Tracker’s Stringency Index. This is a composite measure of government responses across: school closures; workplace closures; cancellation of public events; restrictions on public gatherings; closures of public transport; stay-at-home requirements; public information campaigns; restrictions on internal movements; and international travel controls.

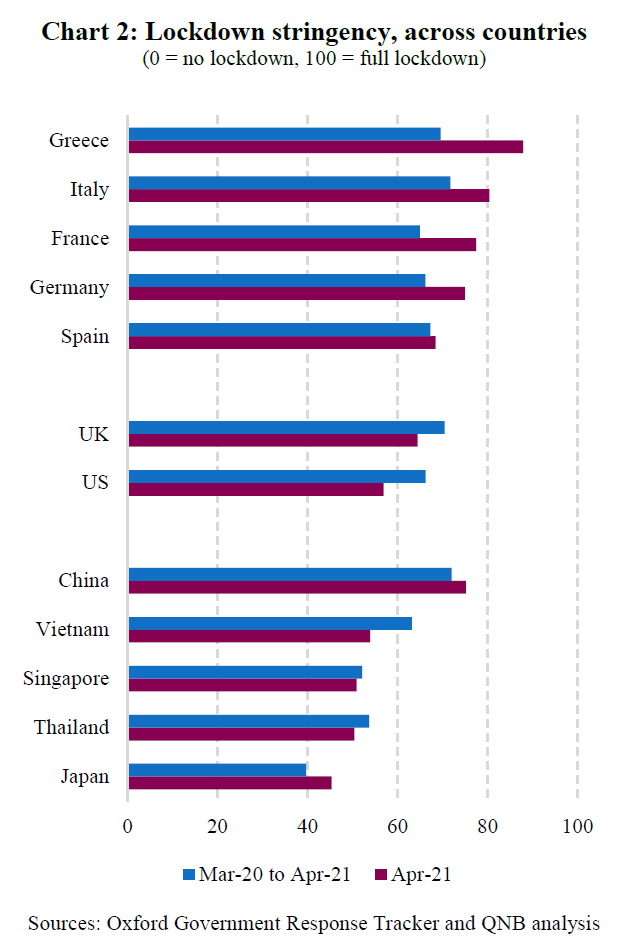

In this article we use this stringency metric to do a stock-take of the policy measures taken by many governments around the world. This will help to validate our assessment of how quickly their economies will be able to recover during the rest of the year. We consider a number of major economies in three groups: 5 Euro area (EA) economies; the United Kingdom (UK) and the United States (US); and 5 Asian economies (Chart 2).

Euro area countries were hit hard by the first wave of the pandemic in early 2020, but also by the winter surge at the end of the year. They therefore had tight lockdowns on average over the past 14 months and still have some of the tightest lockdowns in the world in April 2021 (Chart 2). This understandably had a negative impact on their economies.

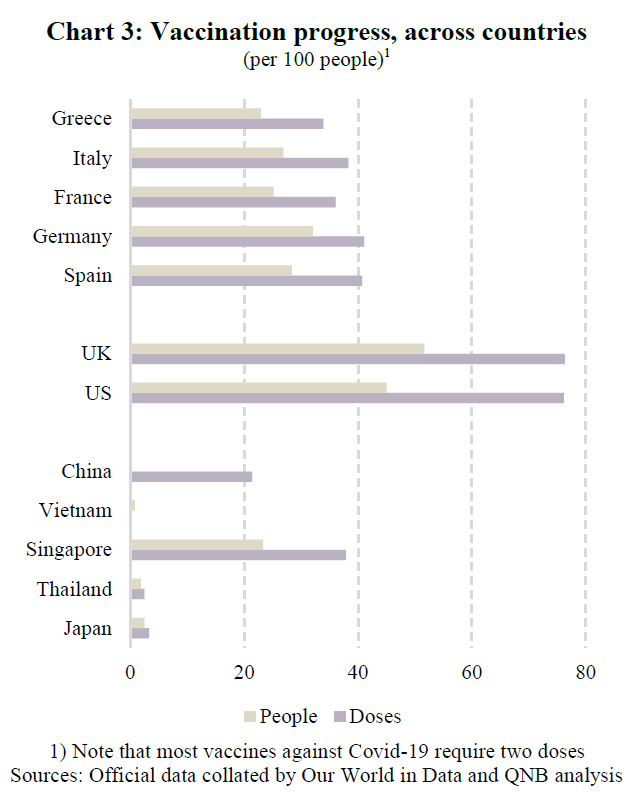

Like Europe, the UK and the US were hit hard by the first wave of the pandemic and also needed to impose tight lockdowns (Chart 2). However, both countries have made rapid progress with vaccination campaigns (Chart 3), which is allowing them to ease lockdowns gradually over the next few months and unlock their economic recoveries.

In contrast, many Asian economies are much more experienced at managing virus pandemics after a number of bird flu and swine flu outbreaks over the past few decades. Countries like China and Vietnam focused on contact tracing to help reduce the spread of the pandemic and tend to be much faster imposing localised lockdowns when new outbreaks are found. This allowed many Asian economies to avoid imposing as stringent national lockdowns for as long as was necessary in Europe and the US. However, success at managing the pandemic in 2020 may be one reason why many Asian economies have made slow progress with vaccinating their populations against Covid-19 (Chart 3). This is likely to constrain their otherwise strong economic recoveries during the rest of the year. Tourism dependent economies like Thailand are particularly exposed to this headwind to their recoveries and are therefore dependent on continued strong global demand for consumer goods produced by their export-orientated manufacturing sectors.

We conclude that the divergence in how countries are responding to the ongoing pandemic, in terms of both lockdowns and vaccination campaigns, is leading to different timing and strength of economic recovery. Indeed, countries that have taken proactive approaches to both lockdowns and vaccinations are best placed to benefit from stronger recoveries sooner. Whereas countries that have delayed either lockdowns or vaccination campaigns, face the challenge of higher numbers of new Covid-19 cases. This will cause an unavoidable delay to their economic recoveries due to lower confidence and restrictions on international travel imposed by others.

Download the PDF version of this weekly commentary in English or عربي