Real estate plays a crucial role in the advanced economies, as it is deeply intertwined with the business cycle, and contributes significantly to the wealth accumulation of households, corporations, and governments. The complexities of the labour-intensive supply chain involved in constructing, financing, and distributing real estate affect a variety of sectors, including the job market, transportation, and financial services.

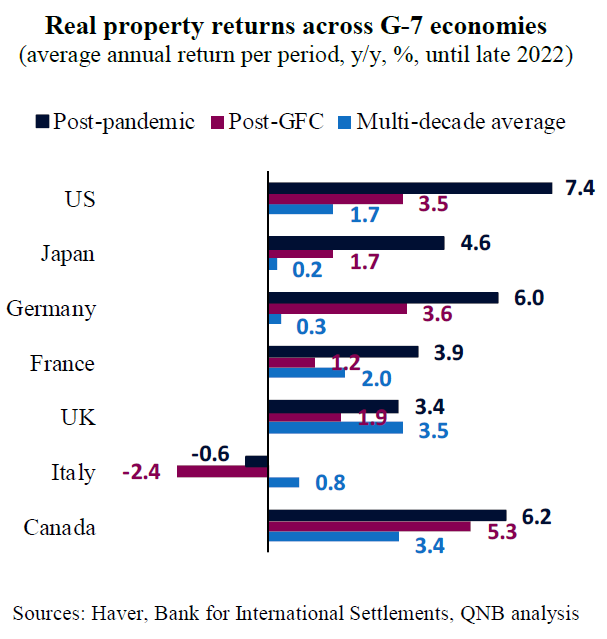

Notably, real estate or property is the largest asset class in the world and serves as the primary source of wealth for households. Real estate has historically demonstrated resilience as an asset, providing long-term wealth preservation. In fact, over the past two generations, real estate prices have generated positive inflation-adjusted returns across all G-7 economies.

However, with the exception of Italy, which was impacted by the Euro crisis, and the UK, affected by Brexit, major economies have experienced a significant surge in real property prices since the Global Financial Crisis (GFC). This trend accelerated further after the Covid-19 pandemic, driven primarily by low and falling interest rates that reduced mortgage costs and stimulated demand for housing and general property yields.

It is important to recognize that strong recent performance does not guarantee a similar trend in the future. Historically, the real estate sector has often been at the center of major economic crises, as seen during the GFC, the US Savings and Loans crisis of the 1980s and 1990s, the UK secondary banking crisis from 1973 to 1975, and the Great Depression of the 1930s.

As such, it is essential to evaluate the overall health of the property sector. We believe that property prices in advanced economies will face significant pressure in the coming quarters due to two primary factors.

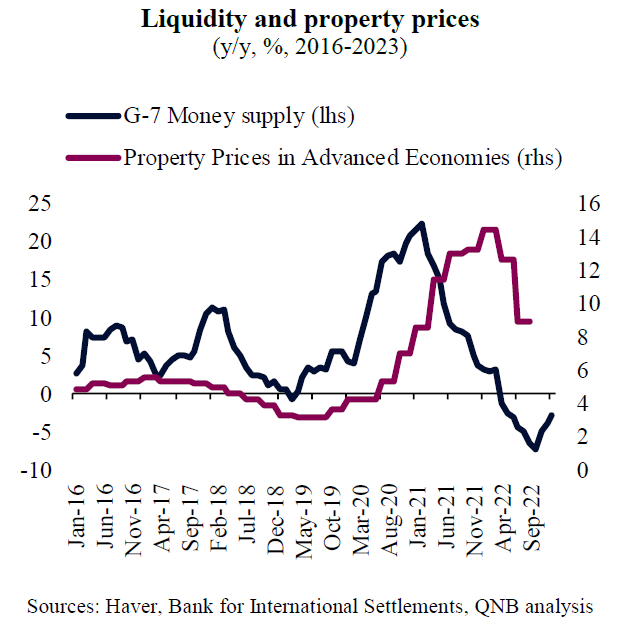

First, the aggressive monetary tightening initiated by major central banks last year presents a significant headwind for property markets. Rising policy rates and diminished liquidity can put downward pressure on real estate prices, as borrowing costs escalate and credit accessibility declines. As central banks increase interest rates, mortgage rates typically rise accordingly, making property financing more expensive for prospective buyers. This can subsequently weaken demand for real estate, leading to reduced property prices. Furthermore, tight liquidity conditions can restrict credit availability, complicating the process for buyers to secure financing. This added constraint suppresses demand, ultimately contributing to a decline in real estate values. Notably, real estate prices have historically lagged behind liquidity injections into the economy, which provided substantial support following the pandemic. However, this pattern now suggests that a price correction may be imminent.

Second, the rapid growth of real estate prices in recent years has outpaced the average increase in salaries and incomes, resulting in a widespread real estate affordability issue. In large cities with constant non-resident demand, inflation-adjusted prices have risen by an average of 60%, while real incomes and rents have only grown by around 12%. Since mid-2021, average mortgage rates have more than doubled across all analyzed cities, and when combined with higher real estate prices, the amount of living space affordable to skilled service workers has dropped by approximately one-third compared to pre-pandemic levels. Additionally, in 2022, inflation and financial market turmoil-induced asset losses are reducing household purchasing power, further curbing demand for housing from the high net worth demographics. This suggests that the real estate market in major advanced economies needs to cool down for a few years, so that housing affordability can recover.

All in all, real estate markets in advanced economies face pressures due to monetary tightening and affordability issues. These factors collectively create a challenging outlook for the sector over the next several quarters.

Download the PDF version of this weekly commentary in English or عربي