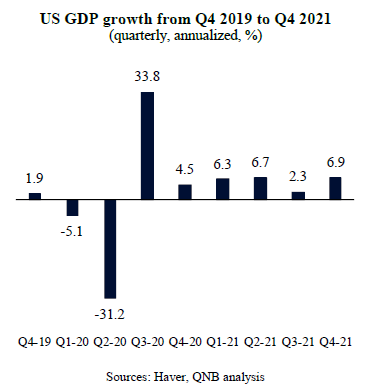

The Covid-19 shock led to a sharp but short-lived downturn, when the US economy staged an epic recovery. In fact, following a GDP collapse of more than 31% annualized in Q2 2020, the US economy rebounded strongly, printing robust annualized growth rates over the subsequent quarters to Q4 last year. Today, the US economy is in the middle of another turning point.

Until recently, consensus forecasts were pointing to another year of extraordinary US growth in 2022. However, significant headwinds emerged, darkening the outlook, including persistent and higher than expected inflation, a rapid monetary policy tightening cycle, disrupted commodity markets, continuous supply-side bottlenecks, and the Russo-Ukrainian conflict. Thus, projections for US growth has been revised downwards in recent weeks. The International Monetary Fund (IMF), for example, has stripped 120 basis points (bps) from their projections for US growth this year, from 4.9% to 3.7%.

In our view, there is scope for an even faster deceleration of the US economy. This article highlights three key leading indicators that suggest that the US economy is set to slow further over the coming quarters.

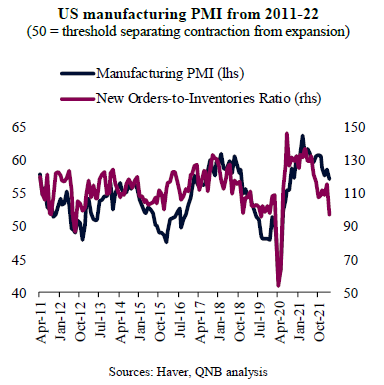

First, key components of the manufacturing Purchasing Managers’ Index (PMI) survey are pointing to a rapid slowdown of the US economy. The manufacturing PMI for March 2022 prints 57.1 index points, well above the 50 threshold that indicates expansion. Nevertheless, and perhaps more importantly, the PMI’s New Orders-to-Inventories Ratio is sinking, suggesting weaker demand going forward on the back of a lack of new orders and higher inventory levels. This ratio also indicates that activity will likely slide to stagnation levels by June.

Second, US equity markets are also pointing to slower growth. After a period of exuberant equity market performance, due to excess liquidity and strong earnings growth, major US indices, such as the S&P 500 and the NASDAQ, started to decline. Importantly, a deeper look sector-specific performance and earnings expectations also suggests a gloomier economic picture. Cyclical stocks, including small-caps, financials and transportation players (airlines, trucking, marine transportation, railroad and delivery companies), whose performance tend to lead the economic cycle, had recently started to stagnate and decline, despite the tailwinds from the post-pandemic economic re-opening. Some of the indices, such as the Russell 2000, are, at the time of writing, closing in “bear market” territory, i.e., down more than 20% from recent highs. Such movements often anticipate periods of significant slowdown or recession.

Third, macro-sensitive bond markets started to flash warning signs. The US Treasury yield curve, the spread between short- and long-term Treasuries, has been flattening for months, accelerating in recent weeks. This flattening of the yield curve normally indicates a more challenging macro environment, as short-dated rates rising faster than long-dated rates point to tighter monetary conditions amid weakening long-term growth and inflation expectations. Inverting yield curves tend to be a indicator of weaker growth and recessions.

All in all, the US economy is slowing rapidly. While a recession is unlikely over the short-term in 2022, due to the strong balance sheets of both US household and corporates, recession risks have increased. Leading indicators, derived from PMI surveys, equity markets and US Treasury markets, are all pointing to a deterioration of US macro conditions.

Download the PDF version of this weekly commentary in English or عربي