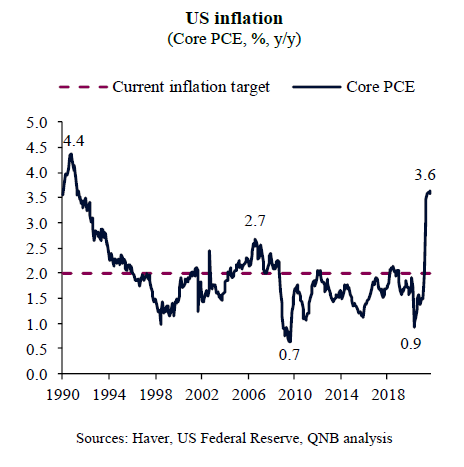

The combination of robust demand growth with pandemic-related supply constraints for goods and services has led to a significant rise in consumer prices. The US core personal consumption expenditures price index (PCE), the US Federal Reserve’s (Fed) favourite gauge for inflation, spiked 3.6% year-on-year (y/y), a level not seen in decades.

“Reflation” has been the name of the game for the US since policymakers aggressively responded to the unprecedented shock from the Covid-19 pandemic. Often referred to as policy-induced periods of surging economic activity and asset prices, reflations can be very positive to kick-start the economy after a severe downturn.

However, reflations can also produce negative side effects, particularly when too much stimulus creates economic and market distortions. An example of economic distortion is when, due to temporary shocks or artificial factors, there is a significant imbalance between supply and demand, such as in the second-hand car market in the US in recent months. Market distortions occur when central bank intervation pushes capital to riskier assets, bumping valuations, such as with listed US growth companies that have been trading at extremely high price-to-earnings ratios.

Importantly, rapid inflation is taking place while the US Fed’s new monetary policy framework remains fresh and un-tested. Officially announced in August 2020, the framework targets average inflation of 2% over time. Under such guidelines, the 2% target should be achieved over the business cycle, which implies that past inflation deviations from target have to be partially or fully compensated in the future or “averaged out.”

Against this backdrop, investors and economists are debating whether the US is on the cusp of a new long-standing inflationary cycle. Is the PCE going to run away further from the Fed’s 2% inflation target? For how long? In other words, is high inflation the new normal for the US?

At the time of writing, concerns are particularly salient as supply bottlenecks in key markets prevail, and may even worsen temporarily over the winter if the global energy market tightens further under higher seasonal demand.

In our view, while prices are expected to remain elevated over the next few months, inflation should nevertheless moderate over the medium-term. We highlight two main reasons to support our assessment.

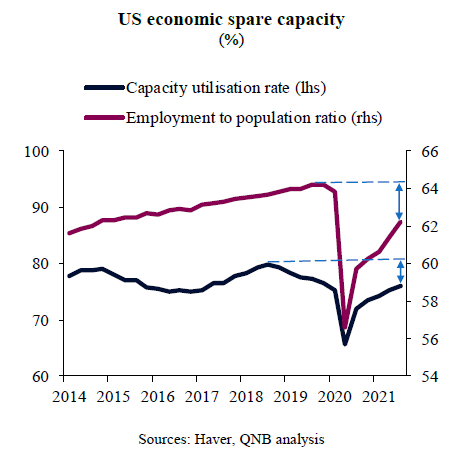

First, there is still significant “slack” or spare capacity in the US economy, which suggests that supply constraints should be temporary. The “slack,” or negative output gap, means that current levels of production and employment are below capacity or labour availability. In fact, total industrial capacity utilization and the employment-to-population ratio are both still significantly below their pre-pandemic levels. Hence, there is still some room for additional manufacturing demand and employment growth before the economy start to overheat to the point of creating permanent inflationary pressures.

Second, there are clear but tentative signs that parts of the supply chain constraints are moderating. High frequency data from Emerging Asia pointed to a strong recovery in activity last month, indicating a significant relief from Covid-19 and Delta-variant related supply woes. The improvement, particularly strong in Southeast Asia, should ease some of the disruption to regional and global supply chains, as factories re-open and output resumes. This is behind the improvement in delivery times from Asian exports in recent months. Moreover, when it comes to shipping constraints, there were also some positive developments. Prices for the transportation of dry bulk materials have already declined by more than 50% over the last several weeks while freight rates for container transportation stabilized.

All in all, despite the ongoing rise in inflation fears, we believe that moderately high inflation is a temporary phenomenon in the US, mostly associated with Covid-19 related supply constraints. Over the medium-term, inflation should moderate, as there is still significant spare capacity in the US and supply constraints are gradually easing as economic activity normalizes across countries and regions.

Download the PDF version of this weekly commentary in English or عربي