Singapore’s economy is booming and there are some indicators that suggest it may be even overheating. After having lifted most of the pandemic related restrictions, the first half of the year has been strong as the reopening boosted the domestic recovery and led to a rebound in household spending. This strength has pushed inflation to a 10 year high of 5.6% in May, unemployment down to 2.2% in Q1, and property prices up by 10% year-on-year (y-o-y).

This week, we take stock of Singapore’s economic outlook, focusing on GDP and inflation, before considering the implications for monetary policy.

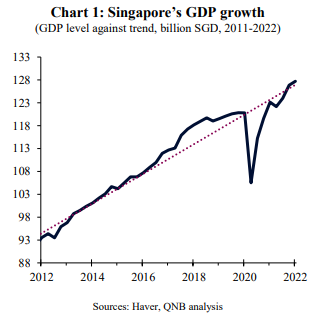

In 2021, Singapore experienced a robust recovery, with GDP growing at 7.6%, the fastest rate in more than a decade, following the deep recession triggered by the pandemic in 2020. A key driver of this was Singapore’s manufacturing sector, which benefited from the surge of demand for electronics and other goods. Indeed, Singapore’s recovery has been so strong that it has taken GDP above the trend growth rate, of 3.2 % over the past decade (Chart 1).

However, we can’t simply extrapolate this strong growth into the future. Growth drivers will continue to rotate towards services from manufacturing as the economy reopens. Indeed, the manufacturing PMI, at 50.4 in May 2022, indicates only modest growth, whereas mobility has recovered to around 10% below pre-pandemic level in early June. On the other hand, there are global headwinds. Oil prices are likely to remain well above $100 per barrel for the rest of the year, which combined with other price pressures will weigh on the outlook for domestic demand. Similarly, the deteriorating external environment has weakened the outlook for exports and the manufacturing sector.

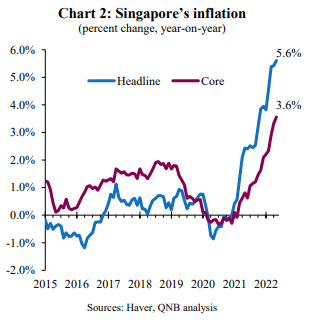

As noted earlier, headline consumer price inflation rose further to 5.6% y-o-y in May. Importantly, core consumer price inflation, a typically more stable metric, which excludes the more volatile prices for food, transportation and accommodation, rose to 3.6% during the same period (Chart 2). Indeed, core inflation is now nearly double the two percent target of the Monetary Authority of Singapore (MAS). Meanwhile, the tightness in the labour market is feeding through to wages, up by 7.8% y-o-y in Q1.

Those indicators point to a possible overheating of the economy over the medium-term. It is therefore important to understand the direction and guidance of MAS in regulating monetary policy to mitigate such risk.

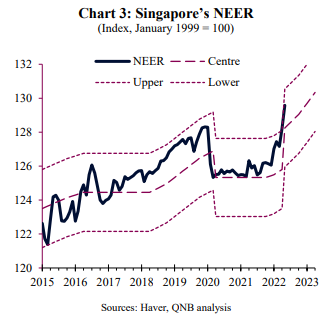

MAS sets its monetary policy by intervening in currency markets to keep the Singapore dollar nominal effective exchange rate (NEER) within a set policy band. MAS’s policy decisions define the slope, width and centre of the policy band, which are calibrated to be consistent with medium-term price stability, currently “just below 2%”.

Going forward, we expect the MAS to increase the slope by a further 0.5ppts to 2%, with a move possible even before the next policy meeting in October (Chart 3). This will signal to the public that the MAS is willing to double down on its tightening path, adjusting to a more restrictive stance quicker if necessary. Such move is important to stabilize inflation expectations, preventing prices to get out of control.

To conclude. Singapore’s economy benefited from the surge in external demand for manufactured goods before domestic demand rebounded strongly as the economy reopened. This, in turn, led to a surge in employment, wages, domestically generated inflation and property prices. MAS has responded by tightening policy twice already this year, with another round of tightening expected in, or before, October. Together, global headwinds and policy tightening are expected to cause Singapore’s GDP growth to moderate to around 3% in 2022, before easing further to 2% in 2023. This would take GDP growth back below trend and would hence refrain from overheating in the medium term.

Download the PDF version of this weekly commentary in English or عربي