Inflation, which accounts for price changes, has been one of the most debated topics in recent months, dominating the agenda of economists and investors alike. The debate has been particularly important in the US, where a strong recovery from the pandemic triggered an unprecedented surge in demand. In fact, the combination of robust demand growth with pandemic-related supply constraints has so far led to a significant uptick in prices.

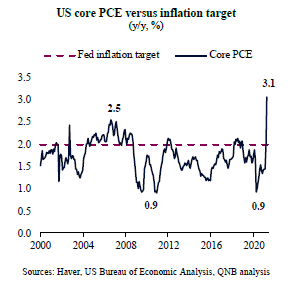

The US core personal consumption expenditures price index (PCE), the US Federal Reserve’s (Fed) favourite gauge for inflation, spiked in April 2021, printing the highest figure in almost 40 years. Moreover, according to the widely-watched survey from the University of Michigan, consumers expect prices to rise another 4.6% over the next 12 months.

According to the Fed’s new monetary policy framework, officially announced in August last year, inflation is targeted to average 2% over time. Under such framework, the 2% target should be achieved over the business cycle, which implies that past inflation deviations from target have to be partially or fully compensated in the future or “averaged.”

Given all of the above, it is therefore only fair to ask whether or not the US is on the cusp of a new inflationary cycle. Is the PCE going to run away further from the Fed’s 2% inflation target? Is the current uptick sustainable?

In our view, while the recent surge in prices has been sharp, inflation is set to moderate over the next several months. Three factors underpin our view.

First, policy stimulus, a key driver for personal income and consumption growth of big ticket items in recent months, is likely to have peaked last quarter. While monetary and fiscal policy remain accommodative, there is little scope for continued increase in stimulus, as the recovery is running fast and the threat from the pandemic was materially reduced by successful mass vaccination campaigns. This is the case particularly for the more effective type of measures such as direct cash payments to households and more generous unemployment benefits. The last batch of “stimulus checks” to US households was delivered in April 2021, and there is little political appetite for new rounds of such transfers at the moment as the US economy is in a much better shape than last year. With no additional checks from the government, personal income is bound to go down in the US over the coming months, which could filter through to contain consumer demand growth.

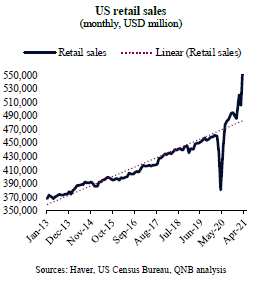

Second, after months of extraordinarily high consumption growth, demand is likely to moderate for some time. Retail sales had not only made up for the sharp contraction during the pandemic, but it is now almost 20% above the pre-pandemic trend, suggesting that it grew “too much, too fast.” Moreover, a significant amount of US spending in recent months was in big ticket, durable items, such as houses, furniture, refurbishment services, automobiles and electronics. The pandemic and work-from-home increased the utility of such items. However, these tend to be one-off purchases that are not repeated very often. Thus, the natural demand for such one-off items, which would otherwise be phased out across many years, seems to have been anticipated in time to the last few quarters. This points to some weakness within those segments moving forward.

Third, financial markets, which usually anticipate macroeconomic changes, are also pointing to an easing of US inflationary pressures over the coming months. The most clear picture of this can be seen on the market for US Treasury bonds, which comprises government securities with 10 to 30 years of maturity that are very sensitive to changes in growth and inflation expectations. Yields on US Treasury bonds tend to move in the same direction of economic projections, as a hot economy requires higher policy rates in the future and a weak economy requires lower policy rates. Despite the recent strong performance of the US economy, Treasury bond yields peaked in March 2021, suggesting that bond investors’ concerns about future inflation have diminished. Similarly, commodity prices have also started to indicate some easing in inflationary pressures. After running hot for several months, the price of growth-sensitive commodities, such as copper or lumber, declined significantly, after peaking in May.

All in all, the rise in US inflation is set to moderate over the coming months. Stimulus, consumption growth, bond yields and growth-sensitive commodities seem to all have peaked at approximately the same time around the end of last quarter and beginning of this quarter. This is likely a sign of decelerating long-term inflation for the second half of 2021.

Download the PDF version of this weekly commentary in English or عربي