The combination of robust demand growth with pandemic-related supply constraints led to a significant spike in global consumer and producer prices. As a result, major central banks have enacted “hawkish” moves, either directly tightening policy or providing forward guidance on imminent changes in policy stance. The Bank of Japan (BoJ), however, is a notable exception to this trend.

Historically at the forefront of radical monetary policy experimentation, the BoJ is continuing its journey on tackling entrenched deflation. While the US Federal Reserve and the European Central Bank are working on a sudden policy shift to tame inflation, the BoJ is set to maintain its mix of ultra-easy policies for longer. This includes negative interest rates, broad-based asset purchases and yield curve control measures that cap long-term rates at low levels.

Three points justify a “dovish” BoJ amid more hawkish major central banks.

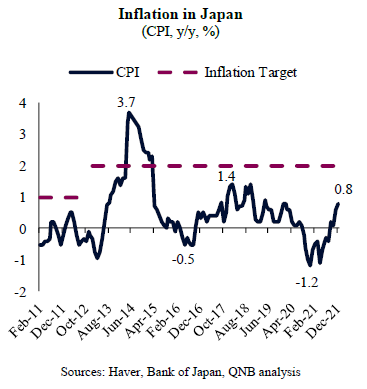

First, despite a recent recovery from negative territory, inflation in Japan remains modest, with a December 2021 print of 0.8%. Importantly, CPI inflation is still running well below the 2% target established by the BoJ in 2013. The latest CPI figure completed the seventh consecutive year of below-target inflation. This point to the fact that deflationary forces continue to prevail in Japan. In other words, the deflationary trap of low growth, low inflation and high levels of indebtedness is offsetting the effects from the post-pandemic recovery and global supply-chain constraints in Japanese prices. Thus, with inflation consistently under-shooting the stated target, the BoJ has no reason to follow its peers in tightening or normalizing policy.

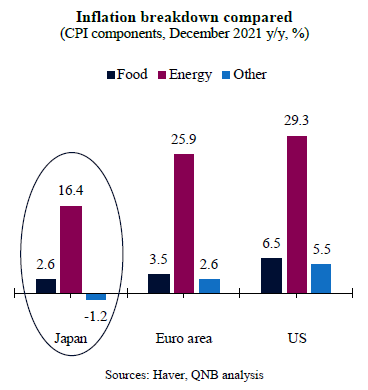

Second, below the surface of headline figures, the recent pick up in prices looks even less persistent in Japan than in other advanced economies. A significant share of the rising prices comes from more volatile and often imported components of the CPI, such as commodity-related food and energy products. Other components of the Japanese CPI still indicate muted or even negative price pressures. The figures are so far supporting the idea that the so-called “pass-through” or contagion from imported inflation is limited in Japan. Therefore, the BoJ would likely sit still even if shocks such as additional supply-chain disruptions or geopolitical events added more pressure to global price inflation.

Third, long-lasting deflation in Japan created a “memory” of flat prices that became entrenched in the behaviour of households and corporates. This “anchoring of expectations” creates a deflationary feedback loop of low spending, low mark ups, low wage growth and overall cost-consciousness. Only large, persistent shocks could break this dynamic. In the absence of such persistent shocks and new behaviours, the BoJ needs to keep the stimulus going.

All in all, the BoJ is expected to maintain once again its accommodative policy, even as other major central banks move toward a tightening cycle. This is due to a low headline inflation, even lower “core” inflation and an entrenched deflationary memory of Japanese residents. It may take some time before we see a hawkish BoJ.

Download the PDF version of this weekly commentary in English or عربي