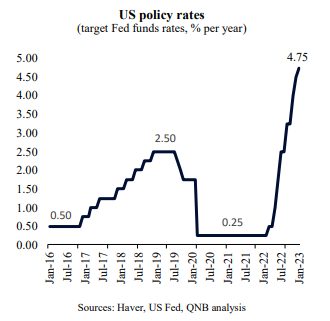

The US Federal Reserve (Fed) has been on the move to revert a decade-long approach of ultra-easy monetary policy since March last year, when untamed inflation forced it to increase policy rates for the first time in more than three years. This marked the beginning of one of the most dramatic and unexpected monetary tightening cycles in US history.

Such policy changes have so far led to eight interest rate hikes, including the aggressive “jumbo” 75 basis point (bps) hikes of June, July, September and November 2022. While the Fed already started to moderate the pace of its tightening cycle in December last year and again in January this year, with milder hikes, there is still an unfinished debate about whether the Fed is ready to wind down, “pause” or even pivot the policy rate changes sooner rather than later during the course of 2023.

The debate has gained further momentum in recent weeks as inflation figures for December were lower than expected and key Fed officials communicated on a more “dovish” tone, i.e., a tone that suggests that the Fed is about to soften more its tightening stance or even pause the hiking cycle sooner than previously expected.

According to Susan Collins, president of the Federal Reserve Bank of Boston, “now that rates are in restrictive territory and we may – based on current indicators – be nearing the peak, I believe it is appropriate to have shifted from the initial expeditious pace of tightening to a slower pace. More measured rate adjustments in the current phase will better enable us to address the competing risks monetary policy now faces.”

But market participants are even more aggressive than Fed officials when it comes to the future path of policy interest rates. Lower inflation expectations and weaker growth prospects are now driving investors to believe that the Fed will cut rates later this year. In fact, Fed fund futures are signalling 50 bps of policy rate cuts by December 2023.

In our view, however, rates are set to remain higher for longer. We expect two more 25 bps hikes for a terminal Fed funds rate of 5.25% in early May. Importantly, we do not expect any rate cuts until at least 2024, barring major geopolitical events or other unexpected exogenous shocks. Two factors underpin our view, as we keep in mind that the Fed’s formal monetary policy framework targets an average 2% inflation rate.

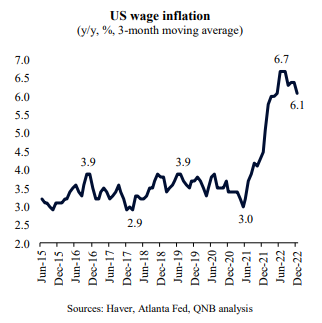

First, even if inflation in the US moderates significantly, it would still be well above the 2% target. As things stand, despite a significant pullback of inflation in recent months, conditions are still not in place for the Fed to meet its target. In order for this to happen, wage inflation, which tends to be an important anchor of overall inflation, needs to stabilize at much lower rates than what we currently see in the US. High wage inflation is associated with one of the tightest US labour markets on record, as there is an undersupply of labour and the number of new job openings continues to far outpace the number of unemployed persons. Hence, more stable prices for longer require a softer labour market, i.e., higher levels of US unemployment. This can be more easily achieved by maintaining interest rates at restrictive levels for as long as it takes for consumption and investment to go down, capping wage growth at lower rates than the current 6%.

Second, despite the aggressive cycle of rate hikes so far, nominal interest rates in the US are still significantly lower than inflation, i.e., “real rates” are negative. After the rate hike early this month by the Fed, real rates are running at -1.75%, against a pre-Covid long-term real rate average of 0.5%. In other words, there is ample room for more hikes, even if inflation moderates further. In fact, inflation is unlikely to come down further towards the Fed target if real rates do not turn positive soon. Therefore, we expect the Fed to lean “hawkish” rather than “dovish,” favouring higher rates for longer instead of risking an early “pause” or pivot.

All in all, the bar for a “dovish” turn is much higher now than it was in any of the monetary policy cycles of the past few decades. Wages are still growing at unsustainably high rates and real interest rates are still in negative territory, suggesting the need for both more rate hikes and higher rates for longer.

Download the PDF version of this weekly commentary in

English

or

عربي