Every summer, the US Federal Reserve (Fed) organizes a coveted economic policy symposium in Jackson Hole, Wyoming. The event is one of the longest-standing central banking conferences in the world, bringing together top economists, bankers, market participants, academics and policy makers to discuss long-term macro issues.

While the Jackson Hole Symposium always looms large in the economic agenda of investors and policy makers alike, this year the importance of the event was paramount. For the first time in decades, Jackson Hole took place during a historical policy normalization process amid well above target inflation.

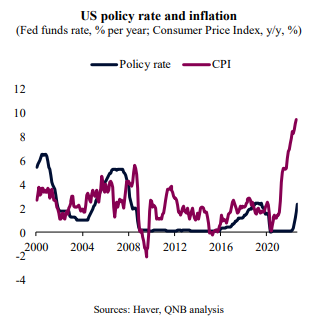

Importantly, however, the symposium followed a period of speculation about a potential near-term “policy pivot” from the Fed. After months of aggressive monetary tightening with successive rate hikes of 75 basis points (bps) each, investors were expecting that policymakers would be less aggressive after summer. The view was that US inflation likely peaked in June and “peak inflation” would beget “peak tightening.” In fact, markets even started to price significant rate cuts in late 2023.

Despite such hopes of a more moderate Fed, the tone from policymakers in Jackson Hole was decisively “hawkish,” i.e., biased towards a more aggressive tightening rather than a “dovish” policy pivot that supports more rate hikes and liquidity withdrawal. According to Fed Chairman Jerome Powell, progress on inflation “falls far short of what the Committee will need to see before we are confident that inflation is moving down” and “restoring price stability will likely require maintaining a restrictive policy stance for some time.” Moreover, Powell stressed that future decisions about rate hikes will be data dependent and another extraordinary hike of 75 bps “could be appropriate.”

In our view, the Fed will lean “hawkish,” raising rates by 75 bps in September and 50 bps both in November and December, before a final 25 bps hike in early 2023. It should then pause for a terminal rate of 4.25-4.5%. Three main reasons sustain our view on policy rates.

First, even if inflation in the US moderates significantly, it would still be well above the 2% target. In the past, every time US inflation breached the 5% mark, the price spiral problem was not contained before policy rates were aggressively hiked to a level that was at least as high as peak inflation. We do not see policy rates surpassing the likely 9.1% “peak inflation” of June this year, but the terminal rate of 3.8% that the market is currently pricing looks excessively optimistic.

Second, despite the recent slowdown, the US economy remains robust, which allows for more aggressive monetary policy tightening. The US consumer is particularly healthy, with households presenting a strong balance sheet with high levels of cash available (USD 15.8 trillion). This is supporting strong household expenditures in services, high levels of private domestic investments and a tight labour market. Such conditions are likely to make the Fed even more cautious in eventually pausing its rate hikes.

Third, the current balance of institutional incentives favours the Fed to be more aggressive, even if higher rates could cause a more significant economic slowdown or financial dislocations. The credibility of the Fed is tarnished by its inability to recognize the magnitude of the existing inflation shock earlier last year. Hence, the Fed is still playing catch up with inflation and in a journey to reinstate its price stability credentials. In other words, the bar for a policy pivot is much higher now than it was in any of the monetary policy cycles of the last 40 years. The Fed is unlikely to pause before inflation rates are substantially lower for some time.

All in all, Fed officials took the Jackson Hole stage to re-set market expectations about rate hikes. The Fed is likely to continue to lean “hawkish” over the near term, as it will fight to reinstate its credibility in a context where inflation is set to continue well above target for some time while the fundamentals of the US economy will remain relatively strong.

Download the PDF version of this weekly commentary in English or عربي