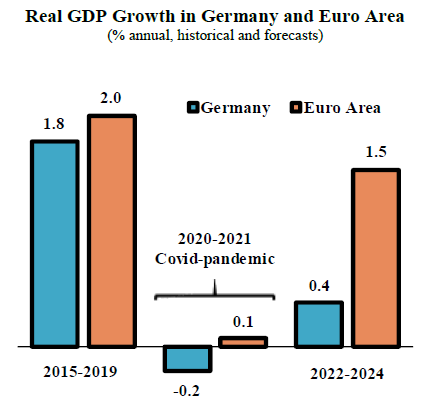

Post-World War II, Germany stood as the economic powerhouse of Europe during extended periods of time. However, over the last two decades, fundamental headwinds began to accumulate. These included negative demographic trends, excessive regulatory and tax burdens, and the omission to upgrade leading sectors to adapt to the digital age and a rapidly changing global landscape. As a result, Germany’s economy has underperformed, with real GDP remaining unchanged in the last 5 years. This compares poorly with the 12.2% expansion for the US, or even the 5% growth for the rest of the Euro Area during the same period.

The incoming administration led by Chancellor Friedrich Merz could mark a turning point in economic policy and performance. For decades, Germany has been committed to fiscal discipline and austerity. In contrast, the new government enters the scene with a massive fiscal expansion package that could reach EUR 1 trillion, including infrastructure and defense, together with plans for tax and labor market reforms.

The economic package marks a paradign shift from Germany’s traditional fiscal conservatism, and will stimulate growth in the medium term. However, the new administration inherits considerable challenges that call for aggressive reforms to sustainably boost the stagnant German economy. In this article, we discuss three key factors that describe the challenges faced by the government and support our outlook.

First, significant structural challenges continue to erode competitiveness and productivity. The World Competitiveness Report provides a useful assessment on this dimension across countries. Just a decade ago, Germany was ranked 6th in the world. However, the country has dropped markedly to the 24th position, reflecting regulatory burdens, onerous tax policies, rigid employment laws, and administrative complexity.

Excessive bureaucracy costs Germany up to EUR 146 Bn a year. The loss of competitiveness is starkly reflected in productivity statistics: since 2017, output per worker has dropped 2.5%. Business leaders point to the amount of red tape and a glacial pace in moving towards the digitalization age. This is particularly damaging in the case of startups, where bureaucratic delays can make the difference between survival and failure of a project. Because of this, companies are increasingly relocating their business to other European countries, such as Holland, Sweden, Portugal or Poland. Therefore, structural problems will continue to weigh on economic growth and need to be addressed by the new administration with measures that go beyond fiscal stimulus.

Second, upgrading outdated infrastructure is critical if Germany aims to achieve a new economic growth phase. Germany’s highly conservative fiscal policy has led to an underfunding in key infrastructure areas. Public investment averaged 2.8% of GDP during 2023-2024, compared to 4.3% in France, for example. As a result of low public investment, aging infrastructure for transportation and energy, and lagging digital technology are hindering long-term economic growth, underscoring the importance of substantial upgrades.

In previous experiences, procurement and planning have taken more time than actual construction, and there are abundant examples where spending funds have gone unutilised. In 2023, EUR 76 Bn in fiscal resources went unused due to bureaucratic and regulatory hurdles. Thus, an infrastructure upgrade should be one of the priorities for the new government. Furthermore, a plan to reduce corporate taxes would only be gradually implemented starting from 2028.

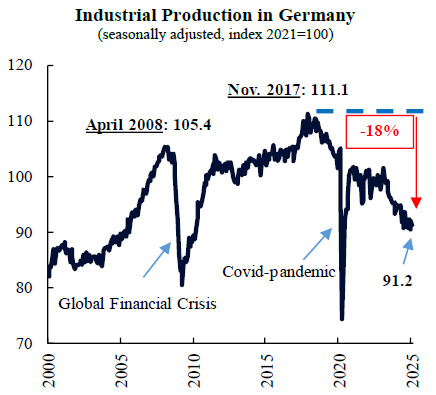

Third, the manufacturing sector, a key sector of the German economy, continues to extend a sustained period of decline that drags on overall growth. Between 2000 and the peak in 2017, the industrial component of real GDP grew at an annual rate of 1.9%. This robust pace reversed dramatically afterwards, as the sector faced a successive series of negative shocks, including global trade tensions, a slowing world economy, the Covid-pandemic, the energy crisis due to the Russo-Ukrainian war, and the decline of the automotive industry. Since its peak in 2017, industrial production accumulates a contraction of 18% in Germany.

This year, the new trade wars initiated by President Trump’s administration, together with the high levels of geopolitical uncertainty, will put further pressure on Germany’s export oriented industries. Although manufacturing should benefit from larger infrastructure investment and defense spending, the new administration will need to secure a more stable environment to offset major headwinds and support growth.

All in all, the government inherits a heavy legacy posing significant challenges to growth. The paradigm shift in fiscal policy will contribute to a much-needed upgrade in infrastructure and likely jumpstart a recovery, providing a boost to medium-term growth, but deeper reforms are also needed.

Download the PDF version of this weekly commentary in

English

or

عربي