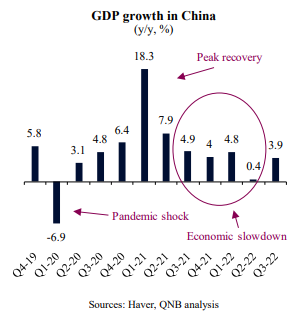

China remains a major source of uncertainty for the global growth outlook. After a collapse in demand and activity in Q1 2020, following the initial outbreak of Covid-19, China performed an impressive GDP growth of 18.3% at peak recovery. The positive momentum lasted from mid-2020 to mid-2021. China at that time was the first and only large economy to present positive GDP growth in 2020, being ahead of other countries in the economic cycle by several quarters.

Nevertheless, over the last several quarters, domestic factors have contributed to a steep economic slowdown in China. This was driven by their Zero Covid policy with lockdowns across Chinese tier-1 cities, restrictive bank lending to the overleveraged real estate sector and aggressive regulatory clampdowns across industries. As a result, China’s Q2 real GDP growth in 2022 was stagnant with the worst economic performance in decades.

Despite the above-mentioned challenges, there were early signs that China was about to turn the corner from its recent economic slump. Chinese policymakers were becoming more concerned about the economic slowdown and started to ease policy more aggressively. In recent months, the People’s Bank of China (PBoC) trimmed interest rates more than once for several segments of the market, indicating a deepening of its “dovish stance.” In addition, it started to ramp up liquidity injections via open market operations. This was amplified by other policy measures, such as credit support to key sectors, subsidized loans, infrastructure investments and other targeted measures.

The impulse from more accommodative policies supported a modest recovery last quarter, when the country’s GDP expanded by a more normal 4% rate, beating analysts’ expectations. The outlook was brightening as the economy was expected to accelerate further on the back of a post-National Congress period of renewed priorities in domestic investments and income redistribution.

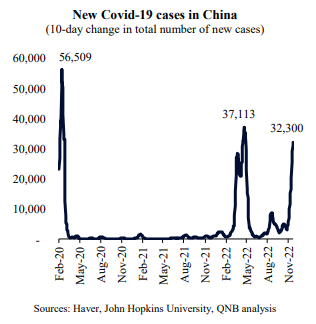

But the expected recovery is now once again challenged by a new wave of Covid-19 cases. The virus has been spreading rapidly in the country across provinces, reaching levels that are comparable with the two previous more acute waves of the pandemic. This shows how China is still vulnerable to the pandemic, as local Covid-19 outbreaks become more frequent as more contagious variants emerge amid a population that is less immunized.

Importantly, despite recent official discussions to ease the Zero Covid approach to the pandemic, certain provinces continue to deploy robust social distancing measures against local outbreaks. This will weight on growth this quarter and potentially next quarter as well as activity will be halted around the locations where new Covid-19 cases concentrate.

However, we do not expect to see the slowdown persist for too long. In our view, “pandemic risks” should moderate in China after Q1 2023. This is due to the development of new, more effective, Chinese mRNA vaccines against new variants of the Covid-19 virus as well as the availability of efficient antiviral pills. Over time, these developments should favour the abandonment of Zero Covid policies, allowing activity to gain momentum in a more sustainable fashion. This scenario was further reinforced by the recent decision of the State Council to urge elderly citizens to get vaccinated and even boosted more often, in order to protect the most vulnerable and secure a more rapid “re-opening” of the country.

All in all, in our base case, the much-awaited cyclical recovery from China should only be delayed by a quarter or two, depending on how severe the current wave of the pandemic will be. We have therefore revised our forecast for growth in China to 3% in 2022 and 5.5% in 2023.

Download the PDF version of this weekly commentary in English or عربي