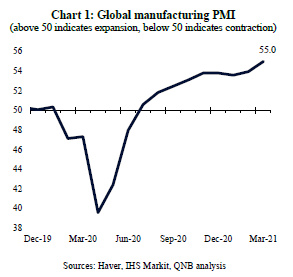

The global manufacturing Purchasing Managers Index (PMI) rose to a ten-year high of 55.0 in March 2021, which indicates that world industrial production has continued to recover (Chart 1). That is no surprise, given that both the US and China are experiencing strong economic recoveries that are helping to drive the global economy. In addition, consumers confined at home have been busy ordering goods and services online for both work and recreation, which has boosted demand for various manufactured goods.

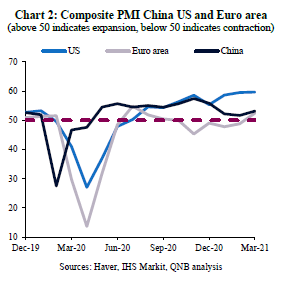

The manufacturing PMI does not tell the whole story, since it ignores the services sector, which is particularly important in both the US and Euro area. We therefore broaden our analysis to the composite PMI (including both manufacturing and services), which allows us to compare the situation in the three main growth engines of the global economy: the US, China and the Euro area.

First, the US composite PMI reached 59.7 in March 2021, which shows that the recovery continues to strengthen (Chart 2), thanks to the potent combination of massive stimulus from both monetary and fiscal policy. The Fed acted fast when the pandemic hit last year, cutting interest rates to zero and flooding financial markets with liquidity via asset purchases. The Fed also adjusted its policy to target average inflation, giving it flexibility to look through a brief period of higher inflation after a period of low inflation. Now, this flexibility will allow the Fed to avoid tightening monetary policy too early and risk derailing the economic recovery in the US. The US has also enacted multiple waves of fiscal stimulus, which has been targeted at consumers and low-income workers. Further, it now seems likely that further stimulus will come from an increase in infrastructure investment, which should help broaden and deepen the recovery. The third factor supporting the US economy is the ramp up of its drive to vaccinate, having already administered a first dose to over 42% of adults.

Second, the recovery in China is maturing, which is allowing the gradual withdrawal of policy stimulus. China’s initial recovery was driven by a return to public investment in infrastructure and facilitated by combating the pandemic with mass testing and effective social distancing measures. As stimulus is withdrawn, the recovery is shifting to a lower gear as indicated by the composite PMI for China, which eased back to an average of 52.3 in Q1 2021, down from a high of 56.3 in Q4 2020 (Chart 2). China’s continued growth is being supported by a recovery of domestic travel and continued strong external demand for exports of consumer products to the rest of the world.

Third, we turn to the Euro area where the recovery has not been sustainable, with the composite PMI falling back below 50 between October 2020 and February 2021. The main form of stimulus provided by Euro area governments has been via furlough schemes, where workers were still paid, even if unable to work due to lockdowns and unemployment benefits. The European Union (EU) also took a large step forward with the introduction of the Next Generation EU Fund (NGEU), worth around USD 880 Bn, which mutualises debt issuance across the EU for the first time. However, EU bureaucracy means that the NGEU is still months away from disbursing its first funds and even by the end of next year, only a quarter of the fund is expected to have been disbursed. Likewise, the ECB has provided monetary stimulus much less aggressively than the Fed has done for the US. The relative weakness of stimulus in the Euro area explains why the Euro area composite PMI has been running below that of the US and China since mid-2020. Indeed, the pick-up to 52.5 in March 2021 is driven by the strength of external demand for manufacturing exports (Chart 2). Unfortunately, the PMI for the Euro area may weaken in April 2021 as continental Europe grapples with a third wave of the pandemic and a number of countries are forced to re-impose lockdowns.

In conclusion, we expect the US recovery to strengthen further, while the strong recovery in China is maturing and there is a risk that the recovery in Europe may falter. Altogether, global growth is expected to gradually strengthen as the year goes on and more people are vaccinated against Covid-19.

Download the PDF version of this weekly commentary in English or عربي