In recent weeks we have covered the pull back of capital flows from emerging markets (EM) and the IMF’s capacity to support countries facing external financing difficulties. This we week we will take a look at the impact of COVID-19 on fiscal sustainability and government debt levels comparing EM with Advanced Economies.

Only last December we highlighted how important fiscal policy would be in the response to negative shocks to the global economy. Now, the global COVID-19 pandemic has hit every country in the world. Governments are taking a variety of measures to limit the human and economic impact. These measures are necessary to save lives, protect the most-affected people and firms from income losses, unemployment, and bankruptcies, and reduce the likelihood that the pandemic results in a deep, long-lasting slump. However, they come at a cost in terms of their impact on government debt.

The level and sustainability of government debt depends on three main factors. The strength of GDP growth, fiscal balance (government revenue minus expenditure) and interest rates.

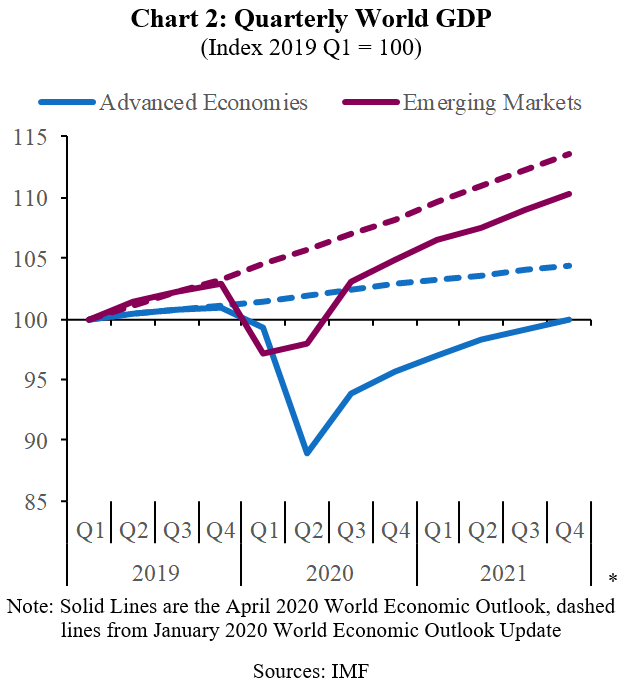

First, the IMF’s latest projections show how sharply expectations of GDP growth have fallen in the past three months (Chart 1). The IMF’s projections imply that it will take until the end of 2021 for advanced economies to recover to the same level of GDP they enjoyed at the beginning of 2019. The hit to GDP in Emerging Markets is less severe, which helps to limit the increase in government debt as a share of GDP. Therefore, this factor is putting more pressure on debt sustainability in advanced economies than emerging markets.

Second, we will look at the shock to fiscal balances. COVID-19 has hit fiscal balances hard across both advanced economies and EM. The main impact will be temporary via reduced tax revenues and support measures, so fiscal balances should naturally improve in 2021 and beyond. There is considerable divergence in fiscal space across countries. Governments have little choice but to support their economies in response to COVI-19. However, we expect considerable divergence between countries in the medium-term and fiscal austerity will be required in many countries, both advanced economies and EM to ensure debt sustainability.

Finally, we will consider central bank policy rates as a driver of the effective interest rates on government debt. Fortunately, global central banks, led by the Fed, have responded to economic shock caused by COVID-19 by lowering interest rates and injecting liquidity. They have done so even more promptly and aggressively than they did in response to the 2008 global financial crisis (GFC). Indeed, interest rate cuts by the Fed and other major central banks have allowed many EM central banks to lower interest rates sharply, helping support both economic growth and debt sustainability. Ultra-low global interest rates are the main factor supporting debt sustainability in Advanced Economies, with positive spill-overs to EM despite an increase in credit spreads of weaker economies.

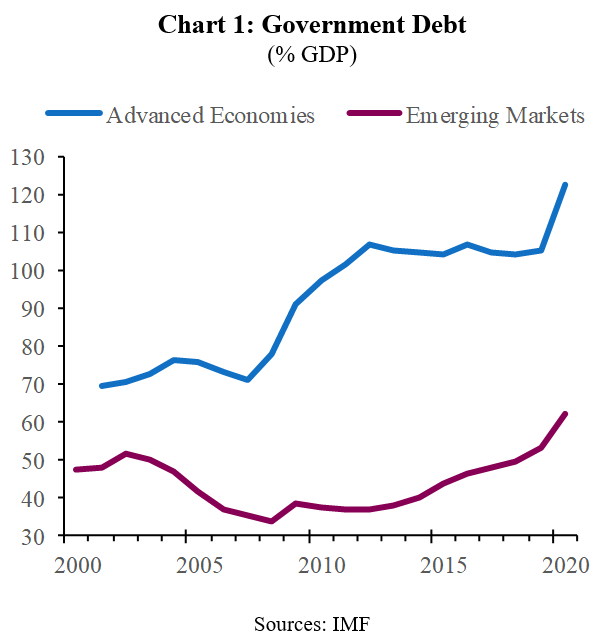

The conventional wisdom used to be that a prudent level of government debt is around 60% of GDP for advanced economies and 40% for EM. However, the 2008 GFC challenged this, causing a jump in the level of government debt in advanced economies to over 100% of GDP. The consistent and persistent fall in global interest rates, is what has kept this higher level of debt sustainable.

Now COVID-19 will push government debt levels to new highs, threatening sustainability. It is our expectation that global GDP growth (both real and nominal) will rebound strongly once COVID-19 has been brought more fully under control. That should lead to a natural improvement in fiscal balances, which will reduce the strain on government debt sustainability. However, it seems likely that global interest rates will need to remain at ultra-low levels for the foreseeable future to avoid causing a systemic global debt crisis. In addition, it is likely that fiscal austerity will be required in many weaker countries to ensure debt sustainability and that will act as a headwind on GDP growth in the medium-term.

Taken together, we can conclude that, despite the sharp rise, government debt remains sustainable in most countries as long as GDP recovers broadly in line with the IMF’s projections and global interest rates remain at ultra-low levels.