The US elections were at the forefront of the global agenda. While it is a domestic event, national US policies have a global impact and will determine the pace of the global economy for the next four years.

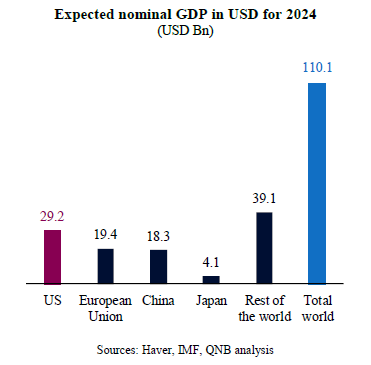

In fact, it is widely recognized that the US economy is not only crucial for long-standing American prosperity but also essential for global stability. Directly or indirectly, the world benefits from America’s extensive market infrastructure, deep financial system, and robust regulatory frameworks. With an expected nominal GDP of USD 29.2 trillion (Tn) in 2024, out of an aggregate of USD 110.1 Tn for the global economy, the US operates at a scale that is unmatched by other economic powers.

Hence, it is important to understand the implications of the US election results for the global economy, particularly as President-elect Donald J. Trump has a comprehensive economic agenda.

After serving as the 45th president of the US in 2017-2021, Trump is not a new comer. Therefore, his economic agenda is well known for investors and analysts. Underpinned by the slogans “Make America Great Again” (MAGA) and “America First,” Trump’s economic agenda is pro-business, pro-capital, mercantilist, pro-domestic manufacturing. In other words, Trump supports de-regulation and less red tape in key industries, lower taxes for corporates and households, more public investments and subsidies for domestic manufacturing and defence, and a strong protectionist stance on foreign trade.

In our view, however, it is important to separate rhetoric from the facts on the ground and actual decision-making. When it comes to “America First” 2.0, this separation is more relevant than ever, particularly for the important topics of fiscal policies, foreign trade, and migration.

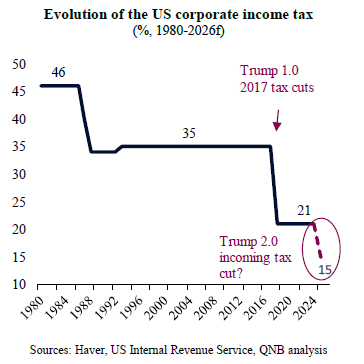

First, on fiscal, Trump indeed seems to be committed to a mix of tax cuts and innovative spending optimization initiatives. During the campaign, Trump proposed a reduction in corporate taxes from 21% to 15%, doubling down on a strategy that paid off in his first term as president. Importantly, the individual tax cuts that he approved in 2017, which are set to expire at the end of 2025, are likely to be extended under his presidency as well. Taken together, those fiscal measures are expected to reduce government income by USD 3 trillion (Tn) to USD 4 Tn. In order to balance this income reduction, Trump is proposing an ambitious government efficiency plan to cut fiscal spending by up to USD 2 Tn. This initiative would be carried on by a new government efficiency commission that is set to be led by Elon Musk, the centibillionaire entrepreneur who is known for his legendary ability of re-arranging supply chains to reduce costs and speed up time to market. Should the Trump/Musk initiative succeed, the new fiscal stance would be favourable to the private sector, incentivizing more consumption and investments without creating additional strains in government finances.

Second, on trade, Trump is expected to re-launch his protectionist agenda. During the campaign, the President-elect proposed imposing higher external tariffs of 10% minimum on the rest of the world and 60% on China. Should this be implemented in full form, it would likely create a significant shock for trade and investment flows. Other countries could retaliate, potentially creating a spiral of “beggar-thy-neighbour” competitive currency devaluations and tariff hikes. This would be negative for consumers globally, increasing costs and inefficiencies. However, we do not expect Trump to fully enact his trade agenda promises. We believe that his aggressive trade policy stance is designed to increase leverage in trade negotiations with major partners and competitors, particularly the European Union and China. Trump wants to extract bilateral concessions by lifting restrictions on US goods and services overseas as well as securing commitments for large foreign direct investments (FDIs) in the US. This would be similar to the playbook of his previous administration, perhaps with a bigger emphasis on FDIs, which are important to create momentum for the on-shoring and new US manufacturing renaissance agenda.

Third, on migration, Trump is expected to moderate his tone an adopt a more pragmatic stance now that the campaign is over. During the campaign, Trump suggested not only the mass deportation of 15 to 20 million undocumented migrants, but also restricting the inflow of visa-holding legal migrants. This would contribute to tighten labour conditions, particularly in the low-wage hourly compensation space. However, given the importance of additional labour supply growth for the service sector and the positive prospects of more favourable demographics to the US economy, we do not expect these measures to be implemented. Instead, Trump is more likely to come with a watered down approach of stricter screening controls for legal migrants and limited, targeted deportations of specific cohorts that are not being well integrated into the US economy. Hence, the potential negative impact on growth from less migration and poorer demographics would be limited.

All in all, Trump “2.0” would bring significant change to the US economic agenda, particularly on the fiscal, trade and migration spaces. Taken together, however, the proposed agenda should be less radical than campaign promises suggest, and US growth prospects should continue to be positive with a projected long-term GDP expansion of 2.5-3% per year.

Download the PDF version of this weekly commentary in English or عربي