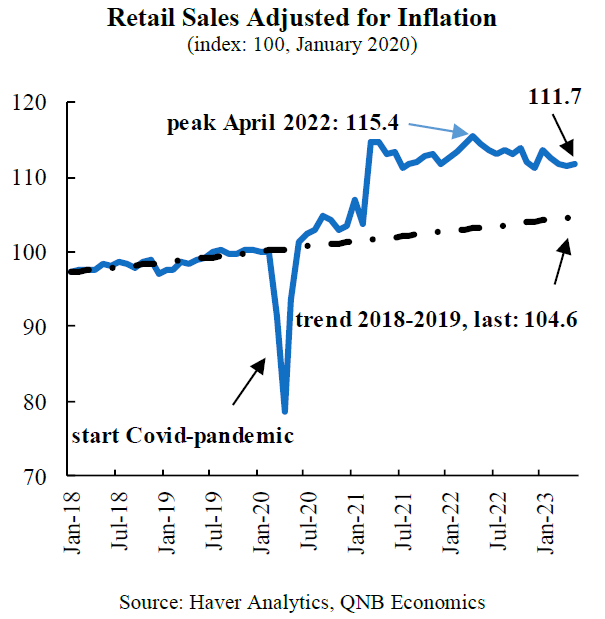

A resilient US economy continues to challenge the imminence of a recession in front of significant headwinds, including high inflation, higher interest rates, and tighter credit standards. Against this backdrop, consumption expenditures, which accounts for approximately 68% of GDP, is holding remarkably well: in the first quarter this year consumption grew at an annualized real rate of 3.8%. This is considerably higher than the 2.5% average in the 5 years previous to the Covid-pandemic. More recently, retail sales (adjusted for inflation) still remain approximately 6.8% above the pre-pandemic trend. But how long can US households keep up with this pace? And how will these dynamics affect the economic downturn?

In a series of articles, we carry-out an analysis of indicators from three categories (production, households, and market-based), to assess the state of the US economy, and how the downturn is taking shape. In this issue, the second one in the series, we take the perspective of the consumers. We argue that two factors continue to support consumption and the view of a US soft-landing.

First, the labor market remains firm, and any signs of softening are still marginal relative to the typical recession dynamics. This year, the unemployment rate has moved in the range from 3.4% to 3.7%, close to historical minimums. In relatively mild recessions, such as the ones in 1990 and 2001, unemployment rates increased by approximately 1.6 percentage points. In contrast, during the Great Financial Crisis of 2007-2008, the unemployment rate increased more than two-fold from 4.6% to 10%.

Unemployment rates can rise either because existing jobs are being destroyed at a higher rate, or because firms are creating new jobs at a slower pace, which results in unemployed workers having to spend more time searching for work. Currently, neither job creation nor job destruction are showing clear signals of deteriorarion in the labor market.

On the side of job creation, nonfarm payrolls have added on average 314 thousand jobs per month so far this year. This figure is well above the pre-Covid pandemic average of 177 thousand during 2018-2019. The Job Openings and Labor Turnover Survey (JOLTS) shows that although there is a softening in the level of job openings relative to the peak in March 2022, these are also still far above the pre-Covid pandemic levels.

The rate of destruction of existing jobs is not showing any sharp signs of deterioration either. The number of claims for unemployment insurance has remained stable in 2023 around a weekly average of 225 thousand, which is not significantly different from the average of 214 thousand of 2022. Additionally, the separations statistics from JOLTS show that the average of the monthly destruction of jobs is lower than last year. Overall, the labor market remains supportive of household consumption.

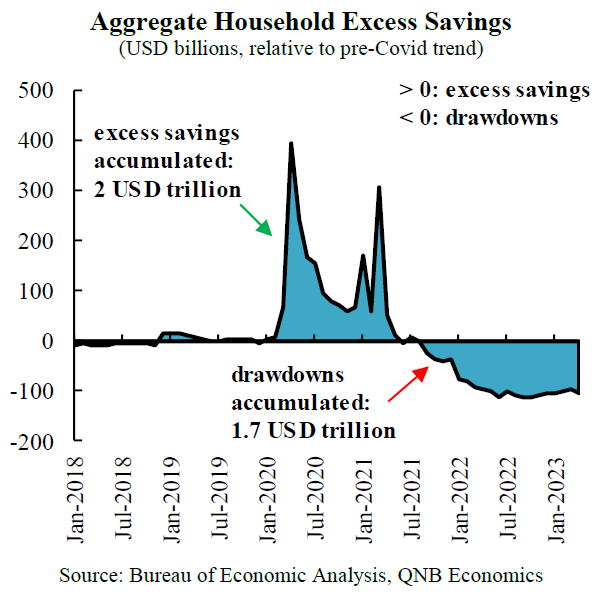

Second, robust household balance sheets support continued strength for consumption. Households hold a large amount of funds that will allow them to support personal spending until at least the last quarter of the year. During the Covid-pandemic, households built up savings at an unprecedented rate. This occurred because of lower spending given the economic closures and social distancing, together with the federal government stimulus packages that injected USD 5 trillion into the economy through a battery of benefits, tax credits, and stimulus checks.

As personal savings increased in an extraordinary manner during the pandemic, the difference with the pre-pandemic trend can be interpreted as “excess savings”. In the period starting in Februrary 2020 and up to August 2021, the accumulated stock of excess savings reached approximately USD 2 trillion. At this point, households started using their excess savings, and have until April of 2023 accumulated drawdowns of approximately USD 1.7 trillion. This implies that around USD 300 billion remain available. Across families with different income levels, and under alternative assumptions, the estimates suggest that households have sufficient funds to support spending into the last quarter of 2023, preventing any sharp downturn in consumption.

All in all, household consumption remains one of the strongest sectors in the US economy, supported by firm labor markets and robust balance sheets, backing our view that the economy is heading to a soft-landing. In a forthcoming issue, we will further analyse and complement our outlook on the US economy from the perspective of markets-based indicators.

Download the PDF version of this weekly commentary in English or عربي