One of today’s biggest macro-economic challenges for policy makers and central bankers on a global level is to combat rising inflation. The post-pandemic combination of excessive policy stimulus with direct transfers to households and persistent supply constraints led to a significant spike in global prices for the last year. As a result, major central banks, such as the US Federal Reserve and the European Central Bank, started aggressive monetary policy tightening cycles. This included several interest rate hikes and the reversion of balance sheet expansion programmes. In contrast, the Bank of Japan (BoJ) has been moving at a significantly slower pace.

After decades of stimulus and experimentation, and despite the recent monetary “hawkishness” or urgency to tighten policy of its peers in the US and Europe, the BoJ still relies on unconventional measures. These include negative interest rates, broad-based asset purchases, and yield curve control targets that cap long-term rates at low levels.

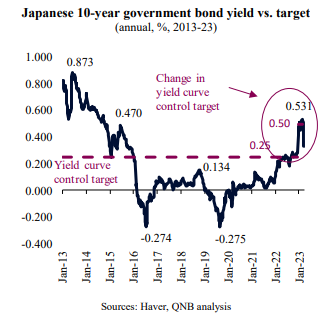

In late December 2022, BoJ officials decided to start a cautious but historical departure from radical, ultra-easy monetary policy. The measure was a soft-touch tweak to the policy target that was set for the 10-year Japanese government bond (JGBs) yield, from a ceiling of 25 basis points (bps) to 50 bps. The change came on the back of above target and accelerating inflation as well as pressures steaming from rapid monetary tightening moves in other parts of the world.

The decision to change the ceiling for 10-year JGBs came as a surprise to market participants and triggered an immediate repricing of local bonds to levels not seen in years. This was followed by investor speculation that this was only the beginning of a more aggressive tightening cycle, as authorities would then soon let go of yield controls altogether.

As a result, in order to sustain the new 50 bps target for 10-year JGBs, which were challenged by speculation that yields are going to increase further, the BoJ had to deploy JPY 19 trillion (USD 4.5 trillion) in asset purchases in January 2023. This was the largest amount of Japanese monthly asset purchases on record, surpassing the heights of the Covid-19 pandemic in July 2020.

While the pressure on the BoJ has since normalized, the winds of change continued to blow. In February 2023, the Japanese government announced Kazuo Ueda as the upcoming governor of the BoJ, after the ten-year tenure of Haruhiko Kuroda, which formally ends next week. The “change of the guard” within the BoJ, while anticipated by most analysts, adds to the speculation about the new directions of the institution.

With this backdrop, what can be expected from the new leadership of the Bank of Japan? In our view, three factors support the idea of a long but steady march to less easing and more monetary policy normalization.

First, the “change of the guard” is set to mark the beginning of a new policy era for the BoJ. The highly respected Haruhiko Kuroda, the outgoing governor, was one of the main architects of the so-called “Abenomics,” the economic policy signature approach of the former Prime Minister Shinzo Abe, which aimed to reflate the Japanese economy with ultra-aggressive measures. Kuroda was therefore often associated with a post-Abe continuation of “Abenomics,” championing “dovish” policies and positions. His exit further stirs the debate about a more significant “hawkish” policy pivot, even if relatively modest, slow and controlled when compared to what happened in the US and Europe.

Second, the upcoming BoJ governor, Kazuo Ueda, a former academic researcher and policy maker, seems to be keen on revising some of the policy tools that are currently used by the BoJ. In an article published in mid-2022, Ueda stated that “the future of our extraordinary monetary easing framework, which has lasted longer than most people expected, will probably need serious consideration at some point.” In the past, he has also taken a more critical stance against ultra-easy, unorthodox monetary policy measures, particularly when it came to negative interest rates, quantitative easing and yield curve control. This makes him well suited to lead a steady process of policy change.

Third, inflation is becoming a real topic of concern in Japan, creating more room for the BoJ to move. The country’s consumer price inflation reached multi-decade highs late last year, surpassing the BoJ target for ten straight months. High and rising prices seem to be already shaking a deeply rooted culture of low spending, low mark ups, low wage growth and overall cost-consciousness. According to the Japanese Ministry of Health, Labour and Welfare, nominal cash earnings of local workers have increased by 5.2% in December 2022, the fastest pace since 1997, and well above the long-term average of 0.6%. This is taking place alongside anecdotal evidence of large Japanese corporates granting significant wage increases to their local workers. In a symbolic move earlier this year, Uniqlo, the leading Japanese fashion retailer, announced a Japan-based staff salary raise of up to 40%. Japanese authorities are calling for similar actions from the rest of the private sector, as consumers suffer from higher imported prices and less disposable incomes.

All in all, after many years at the frontier of monetary policy accommodation, the BoJ is ready to start a significant normalization process, partially catching up with the US and Europe. Financial instability, the exit of the “dovish” or constantly favouring easy monetary conditions “old guard,” a new leadership that is keen on revising the BoJ toolkit and inflationary pressures are all pointing to the same direction. However, the process would still be rather slow and controlled, following decades of the most radical monetary policy experimentation ever tried.

Download the PDF version of this weekly commentary in English or عربي